Published

- 09:00 am

Hitachi Payment Services, India’s leading payments and commerce solutions provider today launched its financial inclusion business to redefine access to financial services for the underbanked and unbanked sections of society. Through this strategic launch, the company has added a critical extension to its existing bouquet of services and will further drive inclusive growth.

The list of services includes - Aadhaar Enabled Payment Services, Micro ATM Services, Domestic Money Transfers, Mobile & DTH Recharges, and Bill Payments

For the initial launch, Hitachi Payment Services has partnered with YES BANK, demonstrating its commitment to collaborative efforts for financial inclusion. The partnership leverages YES BANK’s strong banking expertise and Hitachi Payment Services' extensive network and technology infrastructure to provide reliable and secure financial services to the underserved.

The financial inclusion business will be operated under the brand ‘Hitachi Money Spot Plus’ through a network of retailers called Hitachi Partners and will have a strong focus in Tier 3 to Tier 6 towns across the country. Driving financial empowerment and innovation, the array of services under the financial inclusion business has been made available through its comprehensive app ‘Hitachi Money Spot Plus’ on Google Playstore. The app provides a convenient one-stop platform for financial services and this digital approach complements the Hitachi Partners network, ensuring accessibility and seamless service delivery across the country.

On the launch of the financial inclusion initiative, Anuj Khosla, Chief Executive Officer - Digital Business, Hitachi Payment Services, said, "The remarkable growth of internet penetration and financial literacy in India, especially in our rural communities, presents an urgent call for a resilient payment infrastructure that can keep pace with this rapid expansion. Retailers and merchants are the last mile touchpoints, enabling easy access to finance for customers. Recognizing this, we are extending our services to include financial inclusion initiatives. In essence, we are not just building a payment infrastructure; we are building bridges to financial empowerment and contributing to the nation’s progress.”

Mr. Naveen Chaluvadi, Chief Digital Officer at YES BANK, said "YES BANK has partnered with Hitachi Payment Services to launch Hitachi Money Spot Plus as part of our commitment to promote financial inclusion. This initiative is aimed at enabling financial transactions at hinterlands, focus on taking digital benefits to last mile in an assisted digital mode”.

Anuj Saraswat, Business Head, Financial Services & Inclusion, Hitachi Payment Services, stated “At Hitachi Payment Services, innovation and financial empowerment are the guiding principles that drive everything we do. We believe that everyone should have access to the financial tools and resources that they require to progress, and we are committed to using technology to make that a reality. Our mission is to bridge the financial divide to empower individuals and communities to thrive. With 'Hitachi Money Spot Plus' we have embarked on a transformative journey to build a more inclusive financial ecosystem in India."

- 07:00 am

Paymob, the leading financial services enabler in the Middle East, North Africa, and Pakistan (MENAP) announces that it has received the Central Bank of Oman’s (CBO) Payment Service Provider (PSP) license, making it the first international fintech company to be fully licensed in the Sultanate.

The PSP license authorizes Paymob to accept and process online and in-store payments in Oman, powered by its local integration with CBO’s secure payment infrastructure, OmanNet. This landmark milestone enables merchants in the Sultanate to accept both local and cross-border payments through Paymob’s gateway, eliminating the need for multiple gateway integrations. Paymob secured the PSP license upon complying with all the regulatory requirements of CBO’s framework.

Islam Shawky, Co-founder and CEO of Paymob stated: “It is a proud moment for Paymob to be the first international fintech company to receive PSP licensing in Oman. We appreciate the vote of confidence that CBO has placed in our technology. We are committed to enabling SME growth in Oman by making cutting-edge payments solutions accessible to all merchants and processing transactions seamlessly and securely through our local gateway.”

Oman is on an accelerated path toward the digital transformation of its banking sector, guided by the country’s Vision 2040 which aims to diversify its economy. In the five years between 2018 and 2022, ATM, POS, and e-commerce transactions processed through OmanNet have increased 300%, from 82.4 million transactions to 252.9 million transactions.

With the PSP license in Oman, Paymob further delivers on its mission of enabling MENAP SMEs to thrive in the digital economy via access to a variety of innovative digital payment solutions. Paymob offers 40 payment methods - the most comprehensive suite in the region - which correlates with higher sales, increased conversions, improved customer retention, and appeal to a broader demographic for SMEs.

Paymob, one of the fastest-growing fintech companies in the region, launched operations in 2015 and serves 250,000 merchants across MENAP. The company is backed by global and regional investors including PayPal Ventures, Kora Capital, Clay Point Capital, Global Ventures, FMO, A15, British International Investment, Helios Digital Ventures, and Nclude.

- 04:00 am

Encompass Corporation, the global provider of real-time digital Know Your Customer (KYC) profiles, has acquired CoorpID and Blacksmith KYC from ING to develop a market-leading platform that solves the critical challenge of identification and verification of corporate and institutional clients.

Transform KYC outreach with CoorpID

In 2018, CoorpID was founded by ING Labs in response to the complex KYC challenges ING and the wider market faced. CoorpID allows global banks to automate outreach and gather private KYC data directly from corporate banking customers, providing a repository that allows the corporation to manage all their banking relationships. For large multinationals, the platform makes it easy to store and structure KYC company documents and enables sharing with banks and business partners. CoorpID today services over 500+ multinationals across Europe, helping them to collate, manage, and share relevant corporate data.

CoorpID enables Encompass to build a complete KYC profile, combining authoritative public information with private information directly from customers. This, for the first time, presents financial institutions with a full Corporate Digital Identity (CDI) - providing a unified source of truth and unrivaled visibility into risk.

It, crucially, enhances Encompass’ efforts to solve the key issue of customer outreach for financial institutions. Through this complete customer profile, the need for unnecessary outreach is eliminated. The result is a faster, slicker experience without compromising on robust compliance.

This is complemented by another acquisition from ING, which sees Blacksmith KYC also join Encompass.

Customise KYC processes with Blacksmith KYC

Blacksmith was established in 2017, as part of ING Labs Singapore, to enhance KYC processes for the financial industry. Blacksmith allows banks like ING to configure their Customer Due Diligence (CDD) requirements within a Digital Policy Manager. This ensures that the relevant data and evidence are gathered and streamlines the collection process. Blacksmith has demonstrated up to 50% efficiency savings and is broadly used across the entire ING Financial Institutions client base, in addition to supporting wider external customers.

Connecting this unique capability will significantly enhance Encompass’ offering, making it much easier for banks to turn their manual KYC policies into efficient automated processes to provide analysts with valuable risk insights from the customer profiles and to better monitor Financial Economic Crime (FEC) risk exposure.

One Corporate Digital Identity platform globally

The deal will see Encompass acquire 100% of CoorpID and Blacksmith, creating a platform that will transform the KYC process across the industry. ING will be a stakeholder and development partner to Encompass.

The acquisitions mark a major milestone for Encompass, accelerating the company’s vision to be the number one CDI platform globally, and achieving a core part of its mission since inception in 2011. CDI, which is emerging as a critical sector in the KYC ecosystem, will complement Client Lifecycle Management (CLM) technology to enhance the overall customer journey.

ING sees Encompass as a strategic partner and has committed to using the platform in the years ahead.

Wayne Johnson, co-founder and CEO, Encompass Corporation, said:

“Today is a momentous occasion for our business, and one I could not be prouder to see.

“ING’s commitment to supporting and fuelling KYC excellence has led to the successful journeys of CoorpID and Blacksmith KYC. The combination of the

technology and market expertise brought by these two businesses is the perfect match for Encompass.

“CDI is the future of our industry, solving critical problems for the banks we serve, and these acquisitions represent a huge step forward in bringing our vision, which will transform KYC, to life. I could not be more excited as we embark on this next phase and fully believe in what we collectively bring, with much more on the horizon.”

Ivar Lammers, Global Head of Financial Crime Wholesale Banking at ING, said: "I am very proud of the sale of our KYC innovations that have reached the time for the next chapter of their journeys.

“Encompass, CoorpID and Blacksmith have been established with the customer at heart, which connects them and has been their recipe for success. Together they will continue to provide a first-class customer experience, with smart, tailored offerings that address the needs and challenges of our clients and industry, now and in the future.

“I have no doubt Encompass is the ideal partner to take our foundations to the next level."

- 02:00 am

Robocash analysts questioned investors to find out how their preferences have changed in the past year. The survey involved 617 respondents from 29 countries.

Overall, 2023 was viewed positively by investors. 83% of participants said that the year met their expectations from the P2P market.

73% managed to achieve their investment plans and 6% even exceeded the goals. "The year proved to be quite successful." - experts commented on the statistics. "The volumes of the continental P2P industry went up. Stock markets also gave investors ample profit opportunities and steered clear of critical collapses."

In the past year, investors have been most affected by economic indicators such as inflation and interest rates (32%). In second place were geopolitical events (26%). "Similar statistics were observed in 2022. Investors are aware of the risks associated with the unpredictability of the economic situation, and political conflicts and endeavor to balance them".

Analyzing the prospects for 2024, the vast majority take a rather conservative approach and maintain portfolio volumes. 28% of respondents intend to expand their investment opportunities.

ETFs (24%), equities (18%), and P2P consumer lending (11%) are the leaders in share gains. At the same time, P2P investments are among the top three for perceived declines. "Perhaps going forward, investors are wary of increased volatility in the sector. This could be due to recent regulatory tightening, for example. It’s also possible that investors are seeing other investment opportunities. Overall, the changes reflect a shift in investor interest towards high returns despite increasing risks." - the experts add.

- 01:00 am

Worldline, a global leader in payment services, and Google announced today a strategic partnership designed to leverage cutting-edge cloud-based technologies from Google Cloud to take Worldline’s digital transformation further. As part of the partnership, Google will also work with Worldline to facilitate seamless online payments for Google’s customers in Europe. In addition, both partners will jointly address go-to-market opportunities, and provide new and enhanced digital customer experiences for merchants and financial institutions.

Accelerating digital transformation with the cloud sustainably

Since 2022, Worldline has initiated a “Move to Cloud” program that includes using the cloud to accelerate its digital transformation into a global premium paytech company. Accelerating its trajectory, Worldline now plans to leverage Google Cloud’s secure, high-performance, and low-latency infrastructure, enhancing its operational efficiency, optimizing costs, and improving its strategic positioning.

Worldline will also tap into Google Cloud’s data analytics and AI capabilities to draw benefits from its own data, and consequently develop new payment products and services. The choice of Google Cloud also results from Worldline’s long-lasting focus on Corporate Social Responsibility (CSR) and the low-carbon options Google Cloud offers, as a leader in sustainability.

Google strengthens its partnership with Worldline to facilitate seamless payments for its customers in Europe

As part of the expanded partnership, Worldline will also serve as one of Google’s key payment providers in Europe and across a selection of countries. Worldline aims to provide Google customers with more advanced payment options, support for more payment networks, improved cross-border conversion, and a more streamlined customer experience.

Combining expertise to benefit merchants and financial institutions worldwide

The strategic partnership between Google and Worldline will ultimately create a powerful ecosystem of improved product offerings, delivering added value to merchants and banks, and setting a faster pace for continued innovation. By combining their expertise and their specialized knowledge and resources, Google and Worldline will be able to deliver improved payment experiences for their respective customers, and accelerate time-to-market.

“Our partnership with Worldline underscores the wide range of opportunities that secure and reliable cloud technology, data analytics, and AI can bring to merchants and financial institutions. By bringing together the strengths of our two companies, we can accelerate innovation in the payment industry,” said Thomas Kurian, Google Cloud CEO.

“Innovation and advanced technology are at the core of Worldline’s DNA. To trailblaze changing payment environments and not only meet but anticipate customer expectations, it is key to couple our Paytech DNA with the technological capabilities of a true market leader. We are very proud to expand and strengthen our partnership as a payment provider for Google in Europe. Our deep market infrastructure understanding, combined with Google Cloud's technology expertise and scale, will accelerate our time-to-market and drive tangible success for our customers and markets,” said Gilles Grapinet, CEO of Worldline.

- 06:00 am

Volopa, the transaction, payments, and expenses company has partnered with Yapily, a leading Open Banking API provider, to deliver a seamless payment experience for finance teams.

Powered by Open Banking, this new collaboration directly connects clients to their bank accounts for transfer authorization – allowing CFOs, FDs, and Treasurers to effortlessly load company wallets and fund international payments without ever having to exit the Volopa platform. This new integration also notifies clients when their balance drops below their preferred level and enables them to top up in a few clicks.

Initially launching in the UK, the Volopa – Yapily partnership will later expand to key markets across Europe, streamlining and expediting payment processes for SMEs on a broad scale.

“Our partnership with Yapily marks a significant milestone in making Volopa the go-to platform for international payments and expense management,” said Ali Al Bajati¸ Head of Product at Volopa.

“Our UK clients can now load their company wallets and fund their international payments seamlessly. We look forward to expanding our integration with Yapily to provide further Open Banking related capabilities soon.

“Client-led innovation remains a core guiding principle for us and this strategic alliance reflects our commitment to stay at the forefront of financial technology innovation.”

Stefano Paoletti, VP of Sales UK, commented on this collaboration,

"We’re delighted to partner with Volopa to support transforming their clients’ payment experience. Yapily’s extensive open banking API connectivity and real-time bank access have significantly streamlined Volopa's funding process, allowing for swift, secure, and direct transactions. It not only simplifies funding and international payments but also demonstrates the practical and powerful impact of open banking in enhancing operational efficiency and customer satisfaction."

- 05:00 am

BlueFlame AI (“BlueFlame"), the leading generative AI platform for alternative investment managers, today launched its new Microsoft Excel Add-in. Designed to address the challenges faced by alternative investment managers as they navigate time-consuming diligence and Due Diligence Questionnaire (DDQ) processes, the new feature will help the industry ignite productivity and redefine critical workflows.

BlueFlame customers can now seamlessly embed prompts within cells, effortlessly connecting to firm data sources across documents, databases, market data, and 3rd party systems. By combining the muscle of BlueFlame’s generative AI solution with the unmatched power of Excel, the new feature automates and streamlines workflows to give firms substantial front-office benefits and time savings without the need for multiple interfaces.

Users can leverage the BlueFlame Excel Add-in to enhance and expedite critical yet time-consuming tasks, such as:

Due Diligence Questionnaire (DDQ) Responses: Reference internal documents, such as LPAs, PPMs, IT and compliance documents, past responses, and template responses, to draft DDQ and RFP responses.

Data Room Reviews: Run template deal diligence questions against the contents of a data room for initial reviews and to create information request lists based on any gaps.

Investment Model Integration: Seamlessly pull semi-homogeneous unstructured data into Excel tables, such as aggregating sell-side report price targets into Excel-based models, aggregating leases or HR and management compensation data off PDFs, and more.

Investor Management: Parse out tables of investor documentation, including investor details off subscription and investment documentation.

“Alternative investment managers need the power to easily plug and play with the data and systems they use daily to accelerate critical activities like diligence and DDQ processes,” said Raj Bakhru, CEO and Co-founder of BlueFlame AI. “This new integration allows users to leverage BlueFlame in Excel or wherever they work to transform their workflows and supercharge productivity. We’re excited to continue collaborating with our clients to define these new AI use cases and help them ensure a frictionless AI journey while upholding the highest security, privacy, and compliance standards.”

BlueFlame will host an exclusive webinar to showcase the new functionality on January 23, 2024, at 11:00 am ET / 4:00 pm GMT. The team will provide an in-depth integration demo, highlight key use cases and provide real-time answers to attendee questions. Registration is now open.

This new functionality comes on the heels of a dynamic period for BlueFlame since its launch in October 2023. The company has made waves by bolstering its executive team with top-tier talent strategically positioned to fuel innovation and ensure client success. Additionally, BlueFlame has assembled a distinguished panel of strategic advisors poised to play a pivotal role in shaping its growth strategy and product development.

- 08:00 am

10x Banking, the transformational cloud-native SaaS core bank operating system founded by former Barclays CEO Antony Jenkins, has today announced a new round of funding and the appointment of a Chief Revenue Officer, as it looks to capitalize on the significant momentum in the core banking market.

The round, led by existing investors BlackRock and JPMorgan Chase, marks the latest significant milestone in the company's journey to revolutionize the banking industry through cutting-edge technology and innovative financial solutions.

At the heart of driving 10x’s continued growth is Chief Revenue Officer, Matt Mills, who joined the company this month from Featurespace as the latest member of 10x’s experienced leadership team.

“There has never been a more exciting time for banking transformation and core modernization, as banks across the world embark on this journey”, commented Mills. “I’m incredibly excited to have joined a company with the strongest offering in this space, offering unparalleled resiliency and scale, combined with flexibility and speed beyond the rest of the market. Our mission is to enable banks to make banking better for their customers and society - 2024 is already set to be the most significant in our history, and I’m excited to be part of this journey.”

Having created the modern technology platform focused on a seamless customer experience that powered Chase’s entry into the UK retail banking market, 10x is committed to helping banks transform the way they operate in response to a rapidly-evolving financial sector, catalyzed in part by the dominance of digital transactions and consumer demand for greater control and flexibility around the way they manage their money.

10x’s success in the UK has been built upon through recent expansion into Australia and New Zealand, with more strategic expansions on the horizon as banks actively look to adopt neo-core banking systems to accelerate their digital transformation and thrive in an increasingly competitive battle to win and retain customers.

- 01:00 am

Over a third of all internet shoppers believe committing fraud against brands online is entirely legitimate.

Research commissioned by fraud prevention provider Ravelin, reveals many consumers have a shockingly brazen attitude to fraud, with 37% saying they see nothing wrong with taking advantage of loopholes or gaps in retailers’ policies for their own gain.

A quarter (25%) believe this type of behaviour is a victimless crime, with 27% of respondents believing that fraud helps level the playing field against companies inflating their prices.

For 16% of those polled, friendly fraud is a legitimate way to help with the cost of living crisis and similar numbers (17%) are unworried about being caught.

Almost a third (32%) say there are celebrities and online influencers encouraging this type of behaviour.

However, many of those surveyed firmly believe friendly fraud is wrong and should be punished. Almost half say perpetrators should face harsher punishments (48%), and more than a quarter (27%) believe publicly naming and shaming people would help bring fraud under control.

Interestingly, 52% of consumer fraudsters believe that dishonest behaviour pushes up the prices for everyone – and yet these behaviours prevail. Almost a quarter (22%) say brands make it too easy for people to rip them off.

Ravelin CEO Martin Sweeney said: “We’ve been taken aback by quite how brazen some people are in their attitudes and behaviours when it comes to friendly fraud.

It’s telling that a significant proportion of fraudsters think retailers themselves enable the practice.

“Retailers must strike a delicate balance between facilitating sales and minimising fraud risks, but it’s clear from our findings that many don’t get it right. One size fits all fraud approaches need to be replaced with data-driven approaches that learn and evolve in response to new patterns of behaviour.”

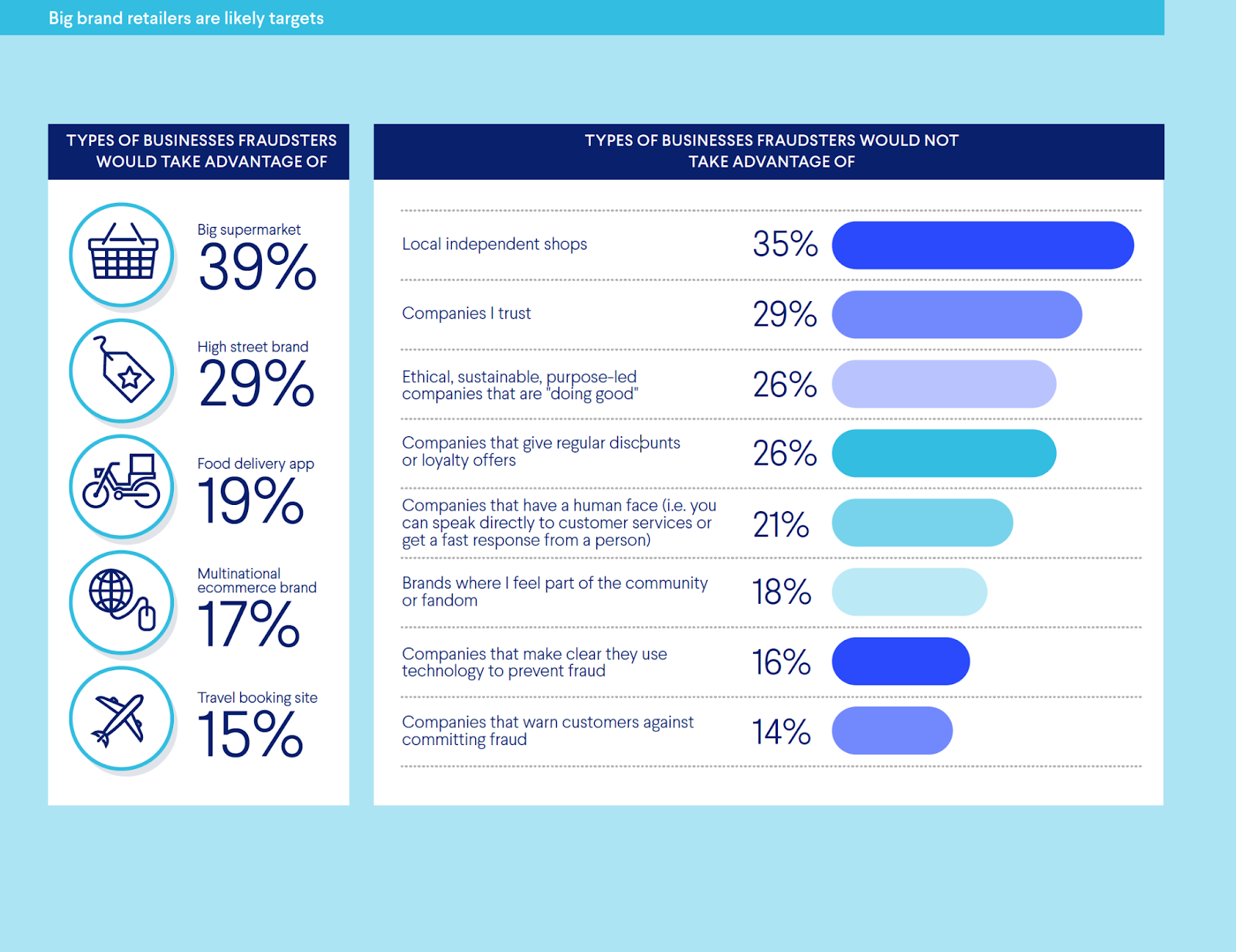

Bigger retailers most at risk

Certain types of merchants are much more at risk from consumer fraud than others with big brand retailers the most likely targets, according to Ravelin’s research.

Large supermarkets are the most at risk, with over a third of consumer fraudsters (39%) saying they are happy to target them.

A quarter (29%) of consumer fraudsters see high-street brands as legitimate targets. Just under one in five (19%) would take advantage of food delivery apps.

On the other hand, purpose-driven brands and social enterprises are least at risk, with only 6% of consumer fraudsters agreeing they are likely targets. Family-led businesses are also less at risk, and are likely to be targeted by only 7% of consumer fraudsters.

Bringing consumer fraud under control

Half of those polled believe more checks and security at checkout are needed.

And a quarter believe better processes around vouchers and returns will help to reduce the lure of fraud.

Nearly half (48%) say harsher punishments are needed, and nearly a quarter (22%) say better communication from brands would help reduce the issue. One in five consumers (21%) believe blacklisting offenders would be a good deterrent.

Martin Sweeney added: “It’s positive to see that many consumers are open to the idea of more checks and security to reduce the impact of friendly fraud. For brands, the challenge is implementing these measures while keeping the customer experience as frictionless as possible.”

Ravelin polled over 6,000 adults across the UK, France, and Germany and found that vast numbers of consumers of all ages regularly commit fraud.

Context: E-commerce growth

The e-commerce industry has seen significant growth over the past decade. International revenue hit over £4,715 trillion at the end of 2023, but the value is expected to reach £5,422 trillion in 2024 and £6,402 trillion at the end of 2026.

The current number of digital buyers is 2.64 billion worldwide.

References: Artios - General e-commerce statistics.

What are consumer fraudsters doing?

|

Survey methodology

Ravelin commissioned a survey of 6278 adult consumers drawn from the UK (2098 respondents), Germany (2092 respondents) and France (2088 respondents) who have shopped online in the last six months. The survey was designed to gauge people’s propensity for and attitudes about e-commerce consumer fraud.

- 01:00 am

Carmoola, the UK-based fintech specializing in direct-to-consumer car finance, has announced a £15.5 million equity investment.

This significant raise follows an £8.5 million Series A round and a £95 million debt facility (both secured in February of 2023), and reflects the confidence inspired by both Carmoola’s performance to date and the strength of its innovative approach to simplifying car finance for UK consumers.

The funding will be used to reach even more car buyers, enabling Carmoola to make further inroads into the UK’s £100 billion used car finance market, which is forecast to grow to £190 billion by 2027. Coupled with a disciplined approach to capital allocation, this investment will accelerate Carmoola’s journey to profitability.

The investment came from US-based fintech specialists QED Investors; VentureFriends; InMotion Ventures, the investment arm of JLR (Jaguar Land Rover); New York-based investors AlleyCorp; and Kyiv-based u.ventures.

Carmoola, which launched its app in March 2022, is transforming the cumbersome and complex car finance market by putting the power back in the hands of buyers and removing the knowledge imbalance that comes with traditional and outdated lending models. The company already boasts an average Trustpilot rating of 4.9 out of 5, from over 1,100 verified customer reviews.

This investment takes Carmoola’s total funding to date to £146 million (including a £95 million debt facility).

Aidan Rushby, co-founder and CEO of Carmoola, said: “We are incredibly excited about this new investment. It's a testament to the hard work of our team and the clear value we bring to car buyers by doing things differently.

“Carmoola came about because we could see that the used car finance market was broken, but the status quo suited traditional lenders just fine, so nobody was doing anything about it. We saw the opportunity to do better and rebalance the situation in favour of the consumer, and our financial backers shared this vision. Now that we have proven our concept we are ready to bring our product to even more people.

“Our goal is to make car financing as user-friendly and hassle-free as possible, and this unrelenting focus has already seen us support the purchase of over £46 million worth of cars. With this new funding, and the support of our investors, we are poised to help even more people buy the car of their dreams.”

Yusuf Özdalga, partner and head of Europe at QED Investors, the backer of finance unicorns Remitly and NuBank said: “Carmoola is shaking up an industry that had grown and remains complacent and is addressing the poor customer outcomes and unnecessary hurdles that the incumbents have allowed to take hold.

“The customer reviews speak for themselves, and show what a real and noticeable impact Carmoola’s customer-first approach is having on people’s lives. It’s clear from this feedback that access to fair, fast and affordable car finance is about more than buying a vehicle; it supports people’s lives and livelihoods. More car buyers deserve to experience the Carmoola treatment, and we are delighted to help make this happen.”

Apostolos Apostolakis, founding partner at VentureFriends, said: “We focus on start-ups that have the potential to address a large market and which can quickly hone in on hard-earned differentiation. Carmoola does just that, and the company’s performance since launch is evidence of the team’s skill in identifying and pursuing opportunities at pace and with intent.

“We are founders ourselves, so understand the highs and lows of start-up life only too well. In our experience, companies whose leaders and people focus unwaveringly on doing what’s right for the ultimate user of their product are the ones that can grow sustainably, and Carmoola is such a business.”

Marshall Porter, general partner at AlleyCorp, said: "Carmoola is delivering a ground-breaking customer experience in an industry where that experience has long been a pain, leaving customers to navigate an unnecessarily slow and bureaucratic process to secure a car.

“As a team of former operators and entrepreneurs ourselves, we are focused on solving the pains that incumbents ignore, and we are proud to back Aidan Rushby and the incredible team at Carmoola as they deliver a much-loved customer experience that also leverages data in a way that just makes them better than the incumbents."

With the UK’s used car market growing year on year and recovering towards pre-pandemic levels, the new funding will be immediately deployed to scale the business to reach and serve even more car buyers. At the same time, user experience and service will remain at the forefront - a commitment that has earned Carmoola independently verified ratings of 4.9 out of 5 from over 1,000 of its satisfied customers.