Published

- 07:00 am

ClearBank, the enabler of real-time clearing and embedded banking for financial institutions, today announced the appointment of Paul Staples as Group Head of Embedded Banking and Nick Ford as Group Head of Channels and Alliances.

Paul has had a 20-year career in banking, and building technology businesses across multiple industries. He is an active commentator and advocate for safe and well-regulated embedded banking. Paul has also founded several technology companies over the years, from oil and gas marketplaces to building a SaaS platform that solves the complexity of the logistics for ports and construction sites. Paul will be responsible for developing the embedded banking business at ClearBank as it expands into Europe.

Before joining ClearBank, Paul was an Embedded Banking advisor to several private equity and venture capital firms and was formerly one of the Founding Executive team of HSBC’s Global Embedded Banking business. At HSBC, he was charged with building and scaling the business by solving complex banking needs for customers and, in doing so, unlocking value for all parties involved.

“ClearBank’s technology, coupled with the strength of a well-funded, responsibly led, and unquestionably compliant bank, is a great combination when it comes to delivering embedded banking,” said Paul Staples, Group Head of Embedded Banking at ClearBank. “Finding deep value through new propositions that no one has conceived before or considered too hard is an exciting opportunity and the ClearBank team is well positioned to deliver on this.”

Nick Ford joins ClearBank having spent over 15 years within SaaS and Risk Managed Services and was previously Vice President of Global Alliances for 6 years at Encompass Corporation, a leader in dynamic KYC Automation. During this time, he established global partner relationships across the UK, Europe, Australia, and North America, responsible for driving indirect revenue from partners as well as driving revenue to the direct sales team.

“I'm focused on building out a global strategy that will drive indirect channel revenue while expanding on ClearBank’s current partner ecosystem as we move into Europe,” said Nick Ford, Group Head of Channels and Alliances at ClearBank. “I’m thrilled to join ClearBank during this exciting stage and eager to place our new and existing valued partners at the forefront of our growth trajectory.”

“It’s fantastic to have both Paul and Nick on board; they bring a wealth of experience to their newly created roles and join us at a pivotal time for ClearBank. With expansion into Europe planned this year, I’m looking forward to seeing what we’ll achieve from building on our new and existing partnerships and further developing our industry-leading embedded banking offering” said Andrew Barker, Chief Revenue Officer at ClearBank.

- 04:00 am

Mastercard is in the development of a new initiative to support small business owners globally with personalized guidance to help them grow and thrive. Acknowledging the crucial contribution of small businesses to the worldwide economy—and the incredible impact of mentorship on their success—the company is piloting Mastercard Small Business AI, an inclusive Artificial Intelligence tool that delivers customized assistance for all small business owners, anytime, anywhere, as they navigate their unique and varied business hurdles.

Today’s influx of data can be overwhelming and while modern businesses face a compelling need to adapt, enhance their skills, and keep pace with changing consumer demands, time is often not on their side. Given that eight out of ten small businesses operate without employees and 88% acknowledge the immense value of having a mentor, resource-strapped entrepreneurs are seeking solutions that get straight to the heart of their needs.

"Operating a small business is a point of immense passion and pride for entrepreneurs, but it’s certainly not easy. We are working closely with small business owners at all stages of development and seeing the myriad of challenges they face and the critical importance of mentorship to their success," said Mastercard Chief Marketing and Communications Officer Raja Rajamannar. “Mastercard Small Business AI aims to create mentorship at scale, offering always-on advice from an inclusive set of sources. This is a testament to our commitment to the small business community and to innovations that lift people."

Catalyzing AI transformation through partnerships

In partnership with Create Labs, a social venture offering technology access to underserved communities, the tool is being crafted to limit biases and cater to diverse entrepreneurial needs. This innovative tool incorporates cutting-edge Generative AI features to offer a conversational experience, drawing on emerging techniques and inclusive design standards to promote a relevant user journey.

The Generative AI tool being created by Mastercard and Create Labs will be responsibly built on diverse and inclusive content. Not only will the AI tool deliver data from Mastercard’s existing repository of content – from the Small Business Community, Digital Doors, Mastercard Trust Center, Strive USA, and elsewhere – a newly formed global media coalition will contribute to that by licensing their business content—such as articles, podcasts, and interviews. The following are slated to be the inaugural participants:

- Blavity Media Group is a digital media company with a mission to economically and creatively support Black millennials.

- Group Black, a Black-owned media company dedicated to connecting brands with diverse audiences. The group’s collective includes Pod Digital Media, Black Women Talk Tech, ReachTV.

- Newsweek, the modern global digital news organization built around the iconic 90-year-old American magazine.

- TelevisaUnivision, the world’s leading Spanish-language media company, reaching over 53 million U.S. consumers across linear and digital platforms.

The tool is scheduled to be piloted in the U.S. later this year, with the goal for international markets to follow. Mastercard plans to have additional partners join worldwide to drive critical local relevance as the tool expands globally

"Uniting for a common goal of inclusivity holds incredible power. Through collaboration, we are looking to combine diverse resources to enhance a tool designed for all small and medium-sized business owners. We hope that these collective efforts shape a more equitable world for future generations, reducing the exclusion felt by numerous minorities and empowering them with the resources needed to succeed," stated Bonin Bough, Chief Strategy Officer and co-founder of Group Black.

A track record of small business community support

Guided by the conviction that the company can do well as a business by doing good in the world, Mastercard is committed to bringing small businesses everywhere into the financial mainstream. Understanding that time is one of the most valuable assets for any small business owner, Mastercard has a strong history of developing dozens of business solutions and services that center around operational efficiency and ease of use. Mastercard Small Business AI will join the company’s suite of small business solutions designed to empower entrepreneurs to help grow and protect their businesses in today’s digital economy.

- 07:00 am

Global Fintech leader Broadridge Financial Solutions, Inc., today announced the launch of OpsGPT, a new capability for operations users, analysts, and management teams to transform their operations across the post-trade lifecycle. Powered by Generative AI (GenAI) and Large Language Model (LLM) technology, OpsGPT uses transactions, settlements, and positions data to provide clients real-time visibility for faster fails resolution, researching next best actions and prioritizing key risk items in a single, easy-to-use interface. The new application is a direct response to industry and regulatory changes. Reduced settlement cycles, the continuous quest for efficiency, and increasing trading velocity are collectively creating significant stress on firms' legacy technology and operating models.

"OpsGPT is the GenAI-powered-copilot that will simplify and optimize trading operations, generating a step change in productivity for operations teams, creating post-trade trade lifecycle event transparency and empowering users to swiftly remediate, reduce, and prevent risks," said Vijay Mayadas, President of Capital Markets at Broadridge. "Leveraging automation to reduce manual intervention through OpsGPT will allow clients to operate at peak efficiency, despite changing regulations and market complexities."

OpsGPT is trained on curated and harmonized data from Broadridge's global multi-asset post-trade systems which power the clearance and settlement of $10 trillion in trades daily. Moreover, Broadridge's leading post-trade platforms are underpinned by a common data ontology and the highest standards of privacy and confidentiality in handling client data. The result is an AI tool that can be rapidly deployed for clients and has the power to streamline access, connectivity, and understanding of data across multiple asset classes to increase operations productivity.

Broadridge has designed OpsGPT with a strong focus on responsible AI practices, addressing the unique needs and challenges faced by the industry. This GenAI-powered application is integrated with Broadridge's existing global, multi-asset class post-trade solutions, allowing seamless use for clients globally.

Overall, Broadridge's AI platform provides the flexibility to choose a model based on specific use case needs, as well as both functional and non-functional requirements. The platform provides a consistent and scalable API interface that makes it easy to switch between different models based on client needs and risk governance processes.

Broadridge recently published a whitepaper entitled, Efficiency Unleashed: Capital Markets Operations Reimagined with Generative AI, which describes how emerging technology, particularly GenAI and LLM, can be leveraged to revolutionize post-trade operations. For more information on how OpsGPT can transform and optimize your trading, please see here.

- 05:00 am

TodayPay Inc., a technology company pioneering a new category in payments called Refunds as a Service™ announced today at the Consumer Electronics Show (CES 2024) that Visa executive Mike West has joined as a Strategic Advisor. Mike West brings deep industry expertise from leading Visa Direct's international commercialization and network expansion by launching new use cases, innovative payment capabilities, and value-added services.

Mike West joins TodayPay with more than 25 years of experience in payments including senior roles at Visa, PayPal, and American Express. West helped Visa Direct expand globally to support successfully scaling the business to over 8 billion card, account, and digital wallet endpoints, across 200 countries, with double-digit year-over-year growth.

During remarks on stage at CES 2024, Jeremy Balkin, Founder and CEO of TodayPay Inc. and former Head of Fintech for J.P. Morgan, said "Mike is a leading expert in the payments industry, product commercialization and Go-to-Market, and helping companies navigate the transition from market entry to global scale. We're excited to leverage his breadth of experience and expertise to bring our innovative TodayPay suite of alternative refund solutions to merchants and consumers."

"I built TodayPay because I've seen firsthand how the speed of a payment can change somebody's life," said Balkin. "There's over a trillion dollars of value exchanged every year in the form of refunds, yet there's been almost zero innovation improving the refund customer experience. Mike will help us revolutionize the refund experience for merchants."

TodayPay, recently named as a Company that "will revolutionize the world of money" at Money 20/20, the world's biggest, most influential gathering of the global money ecosystem, decouples the refund, which is a payment solution, from the return, which is a logistics problem. "This helps merchants compete end-to-end on customer experience based on the speed of a payment, instead of the speed of broken supply chains," said Balkin. For consumers, it means the ability to get paid instantly with multiple redemption choices, instead of the status quo, which is simply a reversal back to the original payment method on the next month's credit card statement.

"TodayPay is a revolutionary force for transforming the refund process which is a trillion-dollar problem for retailers, e-commerce platforms, and marketplaces. TodayPay's momentum and growth show no signs of slowing," said Mike West. "I look forward to bringing my experience as a leader in the payments industry to a business that is establishing itself as a new market champion."

West has over 10 years of experience at Visa, most recently overseeing Visa Direct, a global real-time money movement platform, and the launch of new products, use cases, and growth of international markets. Before Visa, West spent 4 years leading Product Marketing at PayPal, where he supported the company's successful launch of new digital payments solutions and services and subsequent rapid global expansion.

West holds an MBA from the University of New England and a Corporate Finance Executive Program Diploma from London Business School.

- 08:00 am

")

TrueLayer, Europe's leading open banking payments network, has officially joined the SEPA Payment Account Access Scheme (SPAA). This initiative is set to redefine the landscape of account-to-account payments in Europe and TrueLayer is the first company to join the scheme.

The SPAA initiative, extending beyond compliance with the European Union’s payments services directive (PSD2), introduces new features designed to support growth in the European open banking ecosystem. Within SPAA, European banks have an opportunity to develop and offer premium open banking APIs and be remunerated for access to these APIs.

Reflecting on the news, Joe Morley, EU CEO at TrueLayer, said: “Our inclusion in the first SPAA register underscores our commitment to innovation and our role in advancing the next era of payments across Europe.

“SPAA is the long awaited commercial API framework which will allow banks to directly monetise their investment in open banking. It will complement PSD2 and help the EU become a global leader in payments. It represents the start of a new phase, where banks and fintechs collaborate to develop the next generation of account to account payments, to the benefit of European businesses and consumers.

We look forward to continuing to support the development and rollout of SPAA.”

SPAA’s origins go back to 2021 when the European Payments Council was tasked by the European Retail Payments Board to create premium open banking services going beyond PSD2 compliance. The project aims to stimulate the adoption of account-to-account payments, create a meaningful alternative to card companies, and help position the EU as a global digital leader.

- 08:00 am

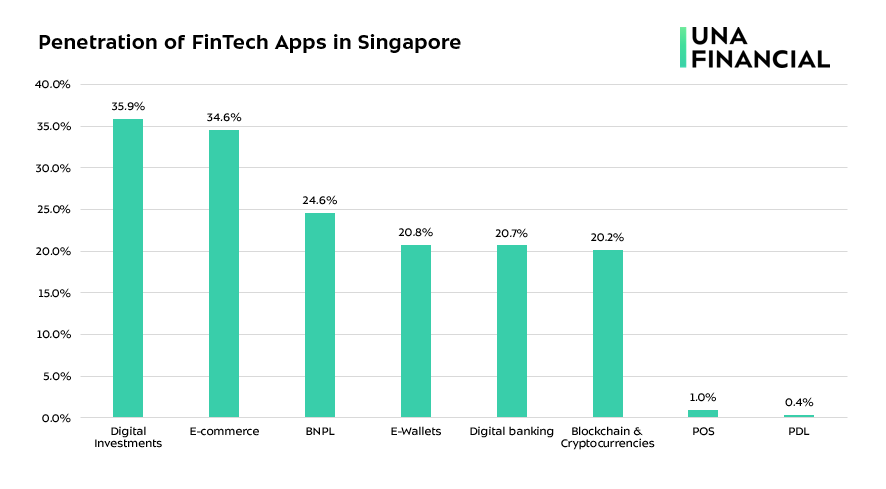

According to analysts of UnaFinancial, digital investment apps are used by 35.9% of Singaporeans aged 15+. The next most popular apps in the country are those designed for e-commerce and BNPL, used by 34.6% and 24.6% respectively

Analysts have revealed that the digital investment sector is developing at a rapid pace. From August 2018 to November 2023, the penetration rate of such applications increased by 14.7 times, reaching 35.9%. The experts explain: “The main driver of the sector’s growth is the desire of the local population to increase private wealth, which is due to the high living standards in the country. It is also influenced by a recent spread of robo-advisors, which has allowed decreasing the minimum investing capital amount.”

The second most popular fintech apps are e-commerce applications (34.6%). From August 2018 to November 2023, their penetration level increased 2.2 times. The analysts comment: “Interestingly, the trend of using e-commerce apps became horizontal after the growth phase. First, there was a general increase in digitalization after the pandemic, which accelerated the introduction of online shopping. The growing demand led to an increase in supply, which was supported by the government. The third driving force was the improving technological base - in 2023, 98% of the population owned smartphones. Today, however, all three factors have almost reached their maximum potential, and to develop further, the market needs a new impetus.”

The third sector actively used by Singaporeans is Buy Now, Pay Later. BNPL app usage has increased by 3.3 times since 2018. Factors contributing to this growth include an increasing spread of e-commerce platforms and the rising popularity of this lending method throughout the region.

Other popular fintech applications in Singapore include e-wallets (20.8%), digital banking (20.7%), and blockchain and cryptocurrency (20.2%). The least used are POS- and PDL apps (with a penetration rate of 1.0% and 0.4% respectively), despite the steady growth of these segments.

The study considered the data on 66 apps in Singapore from data.ai. The analysts counted the number of active users among the population aged 15+ using 3 methodologies. The data on active users were available only for the e-commerce sector. To calculate the number of users for other sectors, the analysts based on the number of app downloads.

- 01:00 am

Riskified, a leader in e-commerce fraud and risk intelligence, today announced further expansion of its Dispute Resolve platform that streamlines chargeback operations for merchant teams, particularly as they face the typical surge in chargebacks after the holidays. The solution leverages expanded gateway and artificial intelligence integrations to auto-compile and format compelling evidence for every chargeback, saving teams time and enabling them to dispute more chargebacks.

A credit card chargeback is a process by which a card owner contests a purchase directly with their issuer, which can force a merchant to reverse the transaction. This process can be abused by a consumer who makes a legitimate purchase, but then falsely claims harm or fraud to obtain a refund. To recover the revenue, chargeback managers must evaluate the legitimacy of a chargeback, and dispute the false claim by gathering and submitting “compelling evidence”. However, the process for compiling compelling evidence and disputing chargebacks is often a manual, time-consuming process, fragmented over several platforms. The result is that the majority of merchants recover less than half of chargebacks, according to a forthcoming study by Riskified. Built to streamline and speed up revenue recovery, Dispute Resolve empowers merchants to centralize and manage all chargebacks, harness automation to minimize manual effort and customize workflows to enhance existing operations.

“The broader e-commerce environment continues to brighten and grow, but with that comes the opportunity for increased chargebacks. Chargeback management is another financial center that’s primed for digital transformation, since today much of the process is manual, and time-consuming, and hinders teams from disputing as many chargebacks as they can. With Dispute Resolve, merchants have full control over their chargeback dispute operations. They can choose to automate specific segments or outsource the entire dispute process,” said Eido Gal, CEO and Co-founder of Riskified.

“Hotelogical’s in-house analyst produces outstanding win rates, and Riskified’s Dispute Resolve enabled her to maintain and scale that performance as we grew. Consolidating data and automating menial tasks allowed her to focus her time, insights, and expertise 100% on revenue recovery,” said David Hobbs, CEO of Hotelogical.

Using Riskfied’s Dispute Resolve platform, merchants can efficiently manage many of the manual processes that are typically associated with the chargeback dispute process. For example, merchants can automatically gather intelligence about the individual's purchase history and order details before deciding which chargebacks to dispute. After building their case, merchants can submit their disputes to issuing banks automatically and monitor the status of those disputed transactions in real time. Additionally, merchants can leverage customized and optimized compelling evidence letters for their disputes. Early results show that merchants may be able to boost chargeback win rates by as much as 35% by switching to Riskified. Along with the ability to view all of their data and results in one consolidated dashboard, merchants using Dispute Resolve can achieve superior performance and savings.

- 03:00 am

Today, the Consumer Financial Protection Bureau (CFPB) issued guidance to consumer reporting companies to address inaccurate background check reports, as well as sloppy credit file sharing practices. The two advisory opinions seek to ensure that the consumer reporting system produces accurate and reliable information and does not keep people from accessing their personal data. First, an advisory opinion on background check reports highlights that those reports must be complete, accurate, and free of information that is duplicative, outdated, expunged, sealed, or otherwise legally restricted from public access. Second, an advisory opinion on file disclosure highlights that people are entitled to receive all information contained in their consumer file at the time they request it, along with the source or sources of the information contained within, including both the original and any intermediary or vendor source.

“Background check and other consumer reporting companies do not get to create flawed reputational dossiers that are then hidden from consumer view,” said CFPB Director Rohit Chopra. “Background check reports, and all other consumer reports, must be accurate, up to date, and available to the people that the reports are about.”

Background Check Reports

Background checks are often critical factors when landlords and employers make rental and employment determinations. The information in the reports can cover a person’s credit history, rental history, employment, salary, professional licenses, criminal arrests and convictions, and driving records. However, as documented in earlier CFPB research on tenant screening, background check reports often contain false or misleading information about individuals.

The CFPB and Federal Trade Commission (FTC) launched a public inquiry in early 2023, and asked for people’s experiences with background checks used to screen potential tenants for rental housing. The CFPB and FTC received more than 600 comments. Most of the comments came from renters. They told the agencies about many problems they encounter, including not receiving adverse action notices and finding inaccuracies and errors that are difficult to correct and that have a decades long impact on housing opportunities. Many described biases in criminal and credit systems transferring into housing decisions.

The CFPB issued today’s advisory opinion on background screening to highlight that consumer reporting companies, covered by the Fair Credit Reporting Act, must maintain reasonable procedures to avoid producing reports with false or misleading information. Specifically, the procedures should:

- Prevent the reporting of public record information that has been expunged, sealed, or otherwise legally restricted from public access.

- Ensure disposition information is reported for any arrests, criminal charges, eviction proceedings, or other court filings that are included in background check reports.

- Prevent the reporting of duplicative information.

In addition, today’s advisory opinion on background screening reminds consumer reporting companies that they may not report outdated negative information—and that each negative item of information is subject to its own reporting period, the timing of which depends on the date of the negative item itself. For example, a criminal charge that does not result in a conviction generally cannot be reported by a consumer reporting company beyond the seven-year period that starts at the time of the charge.

Credit File Disclosure

People have the right to know what information consumer reporting companies keep about them as well as where the information originates. Disclosure of a person’s complete file, upon their request, is a critical component of a person’s right to dispute false or misleading information. Consumers must be provided with all sources for the information contained in their file, including both the originating sources and any intermediary or vendor sources, so they can correct any misinformation.

As explained in the advisory opinion on file disclosure, individuals requesting their files:

- Only need to make a request for their report and provide proper identification – they do not need to use specific language or industry jargon to be provided their complete file.

- Must be provided their complete file with clear and accurate information that is presented in a way an average person could understand.

- Must be provided the information in a format that will assist them in identifying inaccuracies, exercising their rights to dispute any incomplete or inaccurate information, and understanding when they are being impacted by adverse information.

- Must be provided with the sources of the information in their file, including both the original and any intermediary or vendor source or sources.

In a January 2023 report, the CFPB noted improvements and continued challenges for the nationwide consumer reporting companies. The CFPB has highlighted other consumer reporting problems and has reminded consumer reporting companies of their obligations to consumers under the Fair Credit Reporting Act. For example, the CFPB issued guidance on permissible purposes for accessing consumer reports, identifying and eliminating obviously false and junk data, and resolving consumer disputes. Additionally, the CFPB has taken action against consumer reporting companies when they have broken the law, as well as affirmed the ability of states to police credit reporting markets.

Read the advisory opinion, Fair Credit Reporting; Background Screening.

Read the advisory opinion, Fair Credit Reporting; File Disclosure.

Consumers can submit credit reporting complaints or complaints about other financial products and services by visiting the CFPB’s website or by calling (855) 411-CFPB (2372).

Employees who believe their companies have violated federal consumer financial protection laws, including the Fair Credit Reporting Act, are encouraged to send information about what they know to whistleblower@cfpb.gov. To learn more about reporting potential industry misconduct, visit the CFPB’s website.

- 04:00 am

Deriv, a leading global online brokerage specializing in trading and derivatives, is excited to announce the expansion of its partnership with BVNK, the globally regulated payments platform bridging traditional payment systems with blockchain technology.

Through the partnership, Deriv has enabled Solana payments for 2.5 million customers globally, giving them the option to make deposits with digital assets.

With an estimated 4 million owners of cryptocurrency around the world, the demand for digital currency payments is growing. In the last 12 months, the market cap of cryptocurrency Solana (SOL) has grown 700% to over $40bn.

The collaboration with BVNK marks a significant step forward in Deriv's payment strategy, enabling them to quickly meet demand for digital currencies from their diverse global customer base.

Deriv’s decision to explore digital currencies was driven by requests from their customers and the opportunity to expand to new markets. Tiago Garbim, Senior Payment Solutions Operations Executive at Deriv, said: “We've noticed a growing interest in cryptocurrencies like Solana and Polygon among our clients – by partnering with BVNK we can effectively respond to their needs”.

Bernhard Niebsh, Director of Product for Payments at BVNK, said: "Deriv shares our vision for fast frictionless global money movement. This collaboration is more than just integrating new technologies; it's about creating an easy and efficient payments experience for Deriv users around the globe. Cryptocurrency payments are increasingly important to brokers and we’re thrilled to partner with Deriv to support their global growth.”

Integrating with BVNK's API was easy, said Garbim: "We started with Solana due to high client demand and we plan to expand our crypto payment options in future. BVNK's excellent support has made this a very smooth transition."

The partnership between Deriv and BVNK extends beyond digital currency payments. Deriv also uses BVNK’s platform to settle funds from South East Asia, and the partnership has led to significant time savings.

"Our relationship with BVNK has been very smooth in all aspects," Garbim remarked. "Their competitive fees and comprehensive product suite make them an ideal partner for us. We're excited about the future of this partnership."

- 09:00 am

hyperexponential, the global leader in pricing decision intelligence (PDI) software, today announced the completion of its $73m Series B funding round led by global technology-focused investment firm Battery Ventures, with participation from leading Silicon Valley investor a16z, and existing Series A investor Highland Europe, which increased its holding.

hyper exponential serves insurance and reinsurance companies in the multi-trillion-dollar global property-casualty insurance industry, which protects individuals and businesses from a wide array of risks. As factors such as climate change, geopolitical unrest, and cyberterrorism have increased the frequency and severity of risks, the industry has pursued next-generation risk pricing methods to augment or supplant traditional pricing models for a changing world.

The platform of choice for the world’s most significant insurers

hyper exponential’s PDI platform, hx Renew, enables insurers to leverage large and alternative datasets, develop and refine rating tools rapidly, employ sophisticated machine learning approaches to price risk, and make data-driven pricing decisions at the portfolio and individual levels. Since the company’s Series A in 2021, hyperexponential has grown sales 10x while staying profitable, serving some of the world’s largest insurers, including Aviva, HDI, and Conduit Re.

This latest round of financing will support Hyperexponential’s expansion into the United States, as it targets opening its New York office this year. It will also enable increased investment in new product capabilities to serve growing client demand in adjacent insurance markets, including the SME insurance sector. The company plans to double its global team to over 200 in the next year.

Sponsoring its Series B investment and joining hyperexponential’s board as a director is Battery Ventures Partner Marcus Ryu, Co-founder, Chairman, and former CEO of Guidewire Software, which has grown into one of the world’s largest Insurtech companies since its 2001 founding. Also joining the company’s board is experienced Andreessen Horowitz General Partner Angela Strange.

Pricing for today’s frontier of risk

The hx Renew platform, named Insurance Insiders’ 2023 ‘Insurtech Product of the Year,’ enables customers like Convex and Conduit Re to sharpen their competitive edge with enhanced agility, efficient risk transfer, and aggregate loss avoidance. In 2023, Aviva’s Global Commercial and Specialty team was able to build 20 models in 9 months, unlock machine learning capabilities, and improve the speed and accuracy of their pricing and underwriting decisions, even as the frequency and severity of risks continue to evolve continuously.

“The insurance industry is at the forefront of a rapidly changing world and must find ways to understand and respond to that change in risk profile,” said Amrit Santhirasenan, hyperexponential CEO and Co-founder. “We’ve focused on building a capital-efficient, independent business that was both high-growth and sustainable from the outset. Although we have more cash on hand than we’ve raised, we wanted to bring on new expertise in our target markets as we continue our growth into new verticals and geographies. We are delighted to have attracted a world-class set of investors who bring an unparalleled combination of experience, expertise, and support to hyperexponential in the next phase of our expansion.”

"I believe hyperexponential is among the most compelling new entrants in insurtech I have seen in over twenty years of serving the P&C insurance industry," said Marcus Ryu. "As former software engineers and actuaries with top-tier commercial insurers, Amrit and Michael each bring a deep practitioner's grasp of the new requirements for risk pricing. hyper exponential is rapidly becoming an indispensable tool for the insurance industry to thrive in a future that is not reliably the same as the past."

Angela Strange, General Partner at a16z says, "Pricing risk is the most critical function of an insurance carrier. Yet, most actuaries still work with cumbersome Excel models and are constrained by legacy software that limits their ability to dynamically incorporate new data and more sophisticated analytical techniques. Amrit and Michael’s actuarial experience helped them design the system the insurance market needed, and Hyperexponential has achieved incredible traction with technical users and executives alike as they’ve completed multiple industry-leading deliveries around the world. hx Renew is rapidly becoming the operating system for pricing risk in the global insurance market. We are thrilled to join forces with the hyperexponential team as they launch in the US and expand beyond specialty lines".