Published

- 04:00 am

At the extraordinary general meeting of Saxo Bank, Marika Frederiksson was elected to the Board of Directors.

Previously, Frederiksson served as CFO and Group Executive Vice President of Vestas Wind Systems A/S, a global leader in sustainable energy solutions. She has also held various leadership positions including CFO of Gambro AB, CFO of Autoliv Inc., CFO and Senior Vice President Finance and Strategy at Volvo Construction Equipment International AB.

Frederiksson is on the Board of Directors at A.P. Møller - Maersk A/S, Industrivarden AB, Sandvik AB, Ecolean AB and Prodata A/S whilst she is also a member of the Advisory Board at Axel.

Kim Fournais, CEO & founder of Saxo Bank, commented:

“We are proud to welcome Marika to Saxo Bank’s Board of Directors. Her expertise within strategy and leadership will be an important asset as we continue to develop our organisation and grow our business across markets.”

Maria Fredriksson, member of Saxo Bank’s Board of Directors, commented:

“Saxo Bank’s business model is one of a kind with a strong potential to further scale on a global level. Serving both direct clients and institutional partners with powerful and intuitive trading platforms is a core pedigree of Saxo Bank that will only become more relevant as more people look to manage their own investments.”

- 09:00 am

NatWest Group plc (“NatWest Group”) has entered into a strategic partnership with the Vodeno Group (comprising of Vodeno Limited and its subsidiaries) which will see the creation of a Banking-as-a-Service (“BaaS”) business in the UK. This strategic partnership will enable businesses to embed financial services products such as payments, deposits, point-of-sale credit and merchant cash advances directly in their ecosystem by leveraging the Vodeno Group’s BaaS technology, and NatWest Group’s banking technology and UK banking licenses.

Vodeno Group is a European BaaS provider which combines the Poland-based Vodeno Sp. z.o.o (“Vodeno TechCo”), a software company providing its API-based technology platform and the Belgium-based Aion Bank, which has a banking license covering a range of banking products, including loans, deposits and access to EEA payment systems. Vodeno Group is majority owned by Warburg Pincus.

Under the terms of the agreements, a new UK based entity will combine the Vodeno Group’s technological and operational capabilities and its cloud platform with NatWest Group’s banking technology and expertise, building on NatWest Group’s position as a leading supporter of UK business. Through its business banking app Mettle, NatWest Group has built a standalone core banking and payments capability, Vodeno Group’s platform will provide a channel for delivering these capabilities to BaaS clients in the UK.

The new UK entity will be 82% majority owned and consolidated by NatWest Bank Plc, with Vodeno TechCo holding the remaining minority interest. NatWest Group will additionally take a minority interest (initially a 9.9% holding, increasing to 18% subject to certain conditions and approvals being met) in Vodeno Limited, which owns 100% of Vodeno TechCo and Aion Bank.

NatWest Group Chief Executive Alison Rose said:

“As a leading supporter of UK business, we are committed to investing in digital transformation to provide a simpler and better banking experience for our customers. By entering into this strategic partnership with Vodeno Group we will be able to meet the evolving needs of our business customers as they look to embed financial products in their own propositions and journeys.”

“This strategic partnership presents a strong potential source of fee income in a growing market, and an opportunity to deliver sustainable growth by building deeper relationships with our corporate customers. It also complements our existing investment in the development of business banking technology within our Mettle business.”

Wojciech Sobieraj, CEO of Vodeno Sp. z.o.o added:

“Consumers require high quality and accessible banking products that are end-to-end digital, and Banking-as-a-Service is making this possible. Our fully API-based platform offers a comprehensive suite of BaaS products that enable brands to ‘embed’ financial services directly into their ecosystems to create seamless customer journeys. We are excited to combine our technology with NatWest Group to offer the next generation of financial services.”

Completion of the arrangements is subject to satisfying various conditions, including licensing, servicing and other documentation, and obtaining regulatory approvals (including the UK Financial Conduct Authority and National Bank of Belgium / European Central Bank).

NatWest is committed to make in total i) a capped commitment of c.£120m, to enable the establishment of the new UK entity; and ii) a €58m investment in Vodeno Group to acquire an 18% minority stake, investment in each case subject to certain conditions and approvals being met.

- 01:00 am

Fenergo, the leading provider of digital solutions for Know Your Customer (KYC) and Client Lifecycle Management (CLM), has launched a new perpetual KYC solution to enable financial institutions to streamline periodic KYC review processes and reduce costs through automation.

The solution, Fenergo Smart Review, automates the continuous monitoring of client profiles for KYC compliance by identifying all changes to relevant entity data, transactions and anti-money laundering (AML) screening. It uniquely assesses the risk impact of these changes to client circumstances while automatically determining relevancy and materiality. This enables lower-risk cases to be straight through processed while higher-risk cases are prioritised for enhanced due diligence by an analyst. For instance, a change in beneficial ownership to a sanctioned individual, or the appointment of a new exec deemed to be a politically exposed person (PEP), are automatically assessed to determine risk exposure and where human intervention is required.

Financial institutions are mandated to review every customer relationship on a periodic basis in line with global and national KYC regulatory requirements. A recent study by Fenergo describes a people-driven, labour-intensive process. It found that over half of financial institutions are spending between 61 and 150 days on KYC client reviews and the average cost of a single review is $2,200.

“The requirement to complete ongoing KYC reviews manually for a bank with hundreds of thousands of clients presents a huge and costly operational burden, particularly when genuine key risk factor changes are minimal,” said Stella Clarke, Chief Strategy Officer, at Fenergo. “With Fenergo Smart Review financial institutions can streamline the KYC review process by automating the continuous monitoring of clients. This ultimately improves operational efficiencies, while reducing operating costs and regulatory risk.”

“There is growing demand among banks to ease the operational burden caused by the sheer volume of periodic reviews and the amount of time spent completing them,” added Phil Mackenzie, Research Principal at Chartis. Fenergo’s perpetual KYC solution ensures that automation can do the bulk of the heavy lifting – allowing analysts to focus on the material risks.”

Available globally to all financial institutions, Fenergo Smart Review is a modular addition to Fenergo’s Software as a Service (SaaS) CLM offering and comes pre-configured with integrations to leading data and screening providers.

- 03:00 am

ADSS, the Abu Dhabi and London-based financial services firm, has partnered with leading real-time analytics company KX to increase operational efficiency as it rolls out its transformational growth strategy and offers clients greater access to liquidity and a broader range of financial instruments.

ADSS, one of the biggest CFD trading platforms in the Middle East, is making significant investments, and partnering with top-tier technology providers to develop proprietary data processes and multi-asset trading platforms. The adoption of KX technology, incorporating kdb+ the world’s fastest independently benchmarked times series database, has enabled ADSS to better automate and standardize risk management capabilities, reducing margins of error while enhancing execution speeds. KX enables ADSS to combine both real-time streaming and historic data at speed and scale for richer actionable intelligence and critical split-second decision-making. Additionally, the integration of KX’s powerful visualization and dashboard capabilities has enabled ADSS to handle large amounts of data without sacrificing the level of real-time high-quality insights required by financial services firms.

Commenting on the partnership, Chris Dale, ADSS’ Co-Head Quantitative Trading, said: “We price more than 2,700 different instruments, which translates to roughly 1 billion market data ticks per day. To react quickly to unexpected market events, we need real-time analysis of vast amounts of both in-flight and historic data. KX enables us to make better-informed business decisions in real-time, improve customer service with both clients and business partners and be more data-driven across our entire business. We see KX as an important strategic partner for ADSS as we continue our transformation into a data-centric business.”

Nikos Tsoskounoglou, ADSS’ Co-Head Quantitative Trading, added: “Continually enhancing the quality of our data and its delivery speed allows us to leverage large amounts of data in real-time and is vital for accelerating our transformation into a more data-driven organization. The new ecosystem for data that we are building will support our internal processes and continue to enhance our agility in a rapidly changing environment. Through our partnership with KX, we are now harnessing data across the business more efficiently, providing our clients with a more seamless experience, superior pricing, products, and levels of customer service.”

Rich Kiel, Global Head of FX Solutions at KX, commented: “Financial markets operate in microseconds, which is why faster access to richer data and insights is becoming a critical requirement for firms across the sector. We’re delighted to be further strengthening our long-standing relationship with ADSS by supporting its transformational growth strategy, helping it democratize access to data and insights across the business, and ultimately deliver even greater value for customers.”

- 02:00 am

Private markets are now a core component of a holistic wealth management service, with 94% of firms either already offering clients access to these investments or working towards it.

As public markets have remained highly volatile in 2022, 65% of firms have transacted more than five alternative assets deals in the last 12 months, with 38% of managers involved in more than 20 deals.

More than half of managers (53%) say operational challenges are the biggest barrier to scaling their proposition, with two in five (41%) flagging regulatory risk and a lack of resources.

More than four in five (82%) wealth managers say technology plays an increasingly important role in how their clients access private markets.

Wealth managers are increasing their clients' access to private markets as they seek to bypass the volatility of public markets and balance their portfolio's risk, according to Delio's Private Markets in Wealth Management 2022 report.

New Chancellor Jeremy Hunt’s decision this week to scrap most of his predecessor’s mini-Budget measures, which significantly spooked markets last month, has gone some way to improving market stability. But this is a perfect example of the kind of turmoil investors are keen to protect themselves from, with nearly nine in 10 (88%) wealth managers reporting clients are seeking access to illiquid investments, according to the report. Wealth managers are responding accordingly, with 94% of firms saying that they now offer, or are planning to offer, their clients access to alternative assets.

Much of the increased investor interest has been precipitated by the Covid-induced crash of public markets, followed by an extended bull run in 2021, and then another sharp decline over the course of this year. The volatility seen in public markets in recent weeks serves to underline why private markets have risen in popularity so much.

Alternative assets have remained relatively immune to the chaos surrounding public markets. While some alternative asset sectors have been impacted far more than others, the overarching resilience of private markets has made them an essential component of a portfolio seeking investment returns.

Gareth Lewis, chief executive and co-founder of Delio, said: “The importance of private markets to wealth management clients is now clear for all to see. The question for wealth managers is no longer if they offer access to alternative assets, but how they do so in a scalable and efficient way.

“While there is definitely risk inherent in these types of investments, the way that risk manifests is very different from public markets. The relatively illiquid nature of private markets means they are less affected by a shift in sentiment due to external factors, which we see in public markets regularly, and especially in the last few weeks.

“This makes them a great addition to a diversified portfolio. It is no wonder more wealth managers are seeing how important they have now become for their clients.”

Direct investments overtake funds

Delio first undertook this research back in 2019 when most wealth managers who offered access to private markets did so through a diverse range of asset classes, with more than half offering funds, direct investments and real estate deals.

Three years on, and the diversity of investment opportunities available to wealth management clients has increased, yet most firms seem to be consolidating their offering into either direct investments which are offered by 71% of wealth managers, or alternative funds (41%). Impact investments remain popular and are offered by just over one in three firms, while private credit deals are available to the clients of 29% of wealth managers. A smaller proportion of firms are even enabling access to hedge funds and even ‘passion’ investments, such as classic cars, fine wine and antiques.

Gareth Lewis said: "Our research highlights the notable shift in approach that wealth managers have taken in the last three to four years. This is largely due to the significant market turbulence we have seen over this period, firstly due to the pandemic and more recently because of the war in Ukraine and the latest political upheaval. There is no escaping the fact that political decisions have a major impact on the markets, which has been dramatically illustrated in the last fortnight.

“Prior to this, many firms were still in the planning stage when it came to offering private markets to their clients. However, these recent periods of instability have simply confirmed the fact that investors want to allocate more of their wealth to private assets in a bid to mitigate the vagaries of political and economic impacts on their portfolios.

“This has forced slower adopters to accelerate their plans to offer alternative assets to clients as they found themselves playing catch-up, while early adopters were able to shift gears quickly and consolidate their market advantage.”

The wealth management industry is at a crossroads

Wealth managers must decide whether they will commit to scaling private market access by investing in digital tools to do this efficiently, or whether they hope that other aspects of their service are enough to satisfy the majority of their clients while leaving alternative assets available only to their wealthiest clients.

Gareth Lewis added: “One thing is certain - making the correct decision will have significant and long-standing strategic implications.”

- 04:00 am

Get ready to Get Liquid with the next mobile revolution! With iYap Liquid Cash, everything is better. Users can earn cash rewards daily for things they do in-app. Bank, shop, send money, trade crypto, purchase event tickets, get deals, pay bills, find entertainment, and much more... all in one Super App.

Liquid Cash offers the quickest, most safe, and most secure way to pay and get paid from anyone, anytime, anywhere. For travellers who are tired of traditional banking with high foreign transaction fees, low access to international currency, and hacked accounts, Liquid Cash was designed with them in mind. By switching to Liquid Cash users no longer have to pay high and hidden fees to access their money.

"Liquid Cash was initially created because of the opportunity I saw to solve the Caribbean market's local and international payment problems. However, after further review, I quickly realized it was more than just a Caribbean crisis, it was global," says Merrifield, Founder and CEO.

The Liquid Cash app is secured with 256-bit encryption and includes multi-factor authentication to prevent unauthorized access. With Liquid Cash, a user can get a digital bank account with options of savings and checking accounts for both personal and business. Liquid Cash has quickly become the bridge that connects all money into one single universal currency, helping solve the fragmented money issues people face around the world. Merrifield has created an inclusive way for everyone to participate in the opportunity of global commerce without hurdles.

"With the evolution of how people view and value money, giving consumers the ability to use their device to participate in global trade is significant. It's more than just a transaction, it is a gateway for people around the globe to access opportunities. Billions of people around the world are unable to access traditional banking options which potentially excludes them from taking advantage of the advancement's technology has allowed," says Merrifield.

- 03:00 am

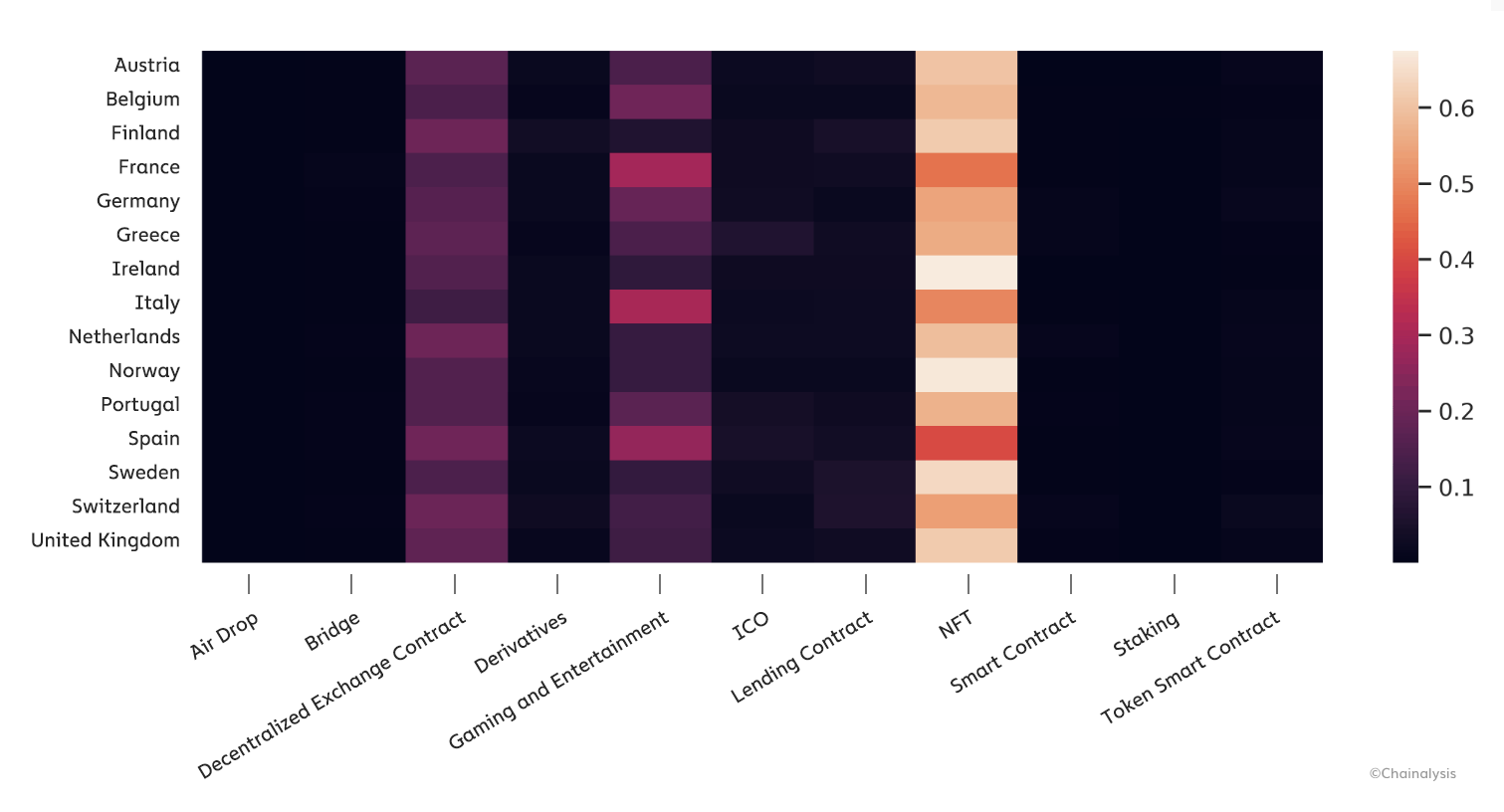

Central, Northern, and Western Europe (CNWE) topped our Global Crypto Adoption Index again this year as the world’s largest crypto economy. Users and institutions throughout the region received $1.3 trillion worth of cryptocurrency from July 2021 to June 2022, and Western Europe alone contained six of the 40 highest grassroots adopters of cryptocurrency: The United Kingdom (17), Germany (21), France (32), Spain (34), Portugal (38), and the Netherlands (39). DeFi protocols and NFTs continued to drive the bulk of this activity, with EU regulations like the crypto travel rule and MiCA licensing regime providing enhanced regulatory clarity.

In most of the ten largest crypto markets in CNWE, on-chain activity grew at a rate of 1-30% over the preceding year. But two outliers stood out: Germany, whose activity grew by 47%, and the Netherlands, whose activity shrank by 3%.

Germany’s outsized growth was likely a byproduct of two recent decisions: (1) to enforce a 0% long-term capital gains tax, and (2) to allow many different types of asset managers to invest in cryptocurrencies. Chainalysis data suggests that these actions had the effect of encouraging both retail and institutional adoption. Dutch regulators, by contrast, took a more cautious tone.

In smaller CNWE countries, changes in on-chain activity varied to a much greater extent. At the poles are Estonia, whose activity leapt by 76%, and Malta, whose activity halved over the time period studied.

Malta faced increased competition from July 2021 to June 2022 as countries like the Bahamas and Bermuda and jurisdictions like Abu Dhabi and Dubai ramped up their efforts to attract crypto start-ups to their region. However, the “blockchain island” still has one of the most comprehensive regulatory frameworks worldwide. Estonia, meanwhile, saw quick success in its ambition to become a central European crypto hub, and in May 2022 turned its attention to reducing money laundering, ransomware, and market contagion risks.

The United Kingdom is Europe’s biggest DeFi district

The United Kingdom ranked 17th in the crypto adoption index this year, up from 21st the year prior. And in terms of raw transaction volume, the United Kingdom is 1st in CNWE and 6th worldwide, with $233 billion in cryptocurrency value received from July 2021 to June 2022.

A lot of this activity was DeFi related. Nearly 20% of the web traffic to both NFT and lending contract-related websites across all of CNWE came from the UK in particular this year.

The UK’s crypto market was also unique in that it was the only top-five Western European country that grew from July 2021 to July 2022 in terms of the raw number of on-chain transactions its citizens engaged in each quarter.

This suggests that crypto adoption rates were more resilient in the United Kingdom than elsewhere in CNWE. “I would like to think it’s because we’ve tried to provide certainty as far as crypto regulation and taxation in the UK,” said Dion Seymour, a Crypto and Digital Assets Technical Director at Andersen LLP and former Policy Advisor at HMRC, the UK’s tax authority. “No one wants crypto to be taxed, but if there’s uncertainty about how it will be taxed, that can cause some level of consternation too.”

Another important barrier to crypto adoption that Seymour felt the UK is continuing to break down is insufficient consumer protections. “Consumer protection absolutely needs to be considered if we want DeFi to become mainstream. We will continue to see a lot of conversation among policymakers, the World Bank, World Economic Forum, OECD, HMT, FCA, and obviously HMRC this year.”

NFTs drive DeFi activity throughout Central, Northern, and Western European citizens

DeFi is popular elsewhere in CNWE as well, and NFT platforms lead the way, driving the most web traffic of any other DeFi protocol type in the region. This is especially true in Ireland and Norway, where traffic to NFT marketplaces accounts for more than 70% of all DeFi-related web traffic.

Blockchain gaming was the second-most highly visited DeFi category in CNWE, with France, Italy and Spain leading the pack. In these three countries, more than 30% of web traffic was metaverse related.

The cutting edge

In addition to being the world’s biggest cryptocurrency market, CNWE has always been on the cutting edge of the cryptocurrency world — the region’s embrace of DeFi being a great example. As new crypto technologies and use cases emerge, it remains to be seen if CNWE retains its status as an early adopter.

- 06:00 am

PPRO, the leading provider of digital payments infrastructure, has completed the rollout of its new, no-code service orchestration layer, uniting hundreds of payment, acquiring, and risk products from dozens of providers - all of which can be deployed and scaled through one connection.

PPRO's orchestration layer enables customers to launch new products and tools faster, and replace legacy platforms more easily while eliminating burdensome RFP processes and single-provider dependence. The milestone concludes PPRO’s technological integration of Alpha Fintech's cloud-based platform, which it acquired earlier this year.

Accessible through the orchestration layer are two new product categories, acquiring platform as a service (APaaS) and risk management, as well as PPRO's existing digital payment methods offering.

PPRO’s APaaS is a cloud-native stack that enables customers to launch best-in-class, end-to-end, acquiring services quickly and cost-effectively. APaaS will appeal to payment service providers looking to break into acquiring, as well as existing acquirers that need to upgrade their legacy systems.

PPRO’s risk management gives customers access to a wide range of easy-to-deploy products and services, from fraud screening applications to chargeback management and prepayment exposure tools. As a result, customers can maximise their risk protection throughout the entire transaction lifecycle by continuously calibrating across a customizable suite of products.

"With our new service orchestration layer, PPRO has greatly expanded its value proposition to deliver everything customers need to optimise and scale their payment services," said Simon Black, CEO of PPRO. "PPRO’s orchestration-powered digital payments infrastructure allows customers and partners to free up valuable time and resources, and offers them products from multiple third-party providers through one connection – from digital payment methods, acquiring and risk management services, to reconciliations, compliance, and more. Ultimately, what this means for our customers is they can laser focus on accelerating their core technology roadmaps and global expansion plans, while we take away a lot of the heavy lifting."

PPRO at Money20/20 USA

PPRO will be attending Money20/20 USA from 23-26 October and participating in a couple of speaking opportunities. Jean Mies, General Manager, Americas, PPRO, will take to the stage to explain how merchants can navigate local payments in Latin America. "The importance of local cards and the rapidly-growing adoption of alternative payment methods in Latin America mean that international and US businesses looking to sell in the region must strategically adapt and tailor their payments and risk management strategies to the market. Money20/20 is the right time and place to take this conversation further," said Jean Mies.

Alicia Rendon, Senior Business Development Manager, PPRO, is also speaking on a panel on bias in the workplace as part of the RiseUp program that the company is sponsoring. "We are excited to join fellow fintech innovators at Money20/20 USA," said Alicia Rendon. "This event brings together the best and brightest in the industry. As a sponsor of the RiseUp program, we are committed to promoting gender equality in the workplace and providing women with the opportunity to excel in leadership roles."

For Money20/20 USA attendees:

- Jean Mies will be speaking on Sunday 23 October at 1:35pm on the Marcello stage, Junior Ballroom, Level 4, The Venetian

- Alicia Rendon will be speaking on the RiseUp stage on Tuesday 25 October at 11:20am

- Please visit PPRO at booth 1235 or book a meeting here

- 09:00 am

Enfuce, the pioneering issuer processing powerhouse, has announced the launch of its dynamic spend management tool Authorisation Control, which empowers companies of any size, in any sector, to set transaction and spending controls for any card in real-time.

Combined with Enfuce’s turnkey Card as a Service (CaaS) platform, Authorisation Control gives card providers unmatched flexibility to create sophisticated rules for approving and declining transactions in real-time, and to have total control over how, where and when cards can be used.

As cards, apps, embedded payments and digital wallets become more widely used across a fast-expanding array B2B and B2C applications and sophisticated use cases, card providers like companies, fintechs and neobanks require more advanced spend controls than just limiting purchases to a certain sum or merchant category.

Authorisation Control goes far beyond current spend management tools in the market, which typically only offer a few generic and basic functions through complicated interfaces that are difficult to navigate. With the ability to set one-time or recurring spend limits, location or merchant restrictions or permissions, and granular transaction data viewable in real-time, Authorisation Control means card programme managers, finance heads, procurement executives and family members can gain total visibility and control over how their cards are used.

With Authorisation Control, card providers, issuers and card managers can:

- get real-time transaction data insights on card usage

- set spending limits, restrictions and permissions for single-use virtual cards, reloadable prepaid cards and credit cards

- ensure the cardholder is verified, whether they’ve entered a PIN, or completed 3D Secure and Strong Customer Authentication checks

- get flexible available balance instead of fixed credit limit or top-up balance

- offer customers cards with detail-level customised controls

- receive authorisation data that is easy to read and relevant to quickly implement custom controls.

Enfuce’s API and Authorisation Control interface has been designed to be seamlessly integrated and as easy to use as possible, especially for entities not familiar with authorisation services. No previous experience or knowledge of card scheme message formats is required. A major difference enabled with this ease of use is that when spending limits need to be adjusted, organisations can do it themselves without needing Enfuce to do it for them. Authorisation Control will be available to Enfuce B2B and B2C clients of all sizes, locations and geographies.

Led by co-founders and co-CEOs Monika Liikamaa and Denise Johansson, Enfuce offers a fast alternative to existing issuer processing platforms, with the agility to quickly add modules and services as and when needed, and a flexible pricing model that’s far more cost-effective and in tune with the scaling needs that companies look for. The first in the world to fully move card issuing to the cloud, and with its turnkey CaaS model, packaged BIN sponsoring, and all regulatory compliance taken care of, Enfuce is a one-stop shop for companies that want to issue cards to their customers.

With Authorisation Control as an add-on to Enfuce’s market-leading CaaS, companies can create their own card programmes, and enrich decision-making by combining transaction data with their own data, from their customer apps or CRM systems for example, to have 360-degree understanding of their card programme usage and trends, and to become even more relevant to their customers.

Denise Johansson, Co-Founder and Co-CEO of Enfuce, comments: “I do believe that Enfuce has the most accessible and flexible spending solution with Authorisation Control. We offer it to all of our customers, regardless of whether they’re consumer or commercial, regardless of whether it’s for a prepaid or credit product. We can provide total card control for every company and every card they offer.

“Many companies have been unable to maximise the potential of their card programmes, as they’ve been unable to understand transaction flows and believe authorisation management is too complex and scary to implement. Enfuce takes away that complexity. With Authorisation Control, something that was hard to do previously is now so much easier. We strive for excellence in every service that we launch, and our Net Promoter Score of 95 shows our focus on customer satisfaction. Combined with our CaaS platform, which has the fastest onboarding time in the market of just eight weeks, Enfuce is empowering our customers to create even more end user propositions, and the best possible customer experience for their end users.”

Monika Liikamaa, Co-Founder and Co-CEO of Enfuce, says: “With Authorisation Control, we have taken something that is usually incredibly complex and translated it into something that is easy for our customers. You don’t need to be a technical expert or have a manual at hand to use Authorisation Control, as it gives card managers everything they need to control how their cards are used – and all in real time. They can adjust authorisation and spending limits whenever they want, to be as fluid or as strict as they need to be and have full control of the end-to-end process.

“Because it accesses transaction data in real time, Authorisation Control’s flexibility allows for a multitude of use cases across B2B and B2C applications. The more transaction variables you have, the more sophisticated things you can do with the card. For instance, Authorisation Control lets organisations see which employee is using the card, which merchant or supplier they’re spending at, what they’re buying, and whether it's a PIN, contactless or digital wallet transaction. Or parents or family members can set spending controls on their child’s card so that they can only buy items that the parent has permitted, or use the card for a specific time period, like during a school trip for example.”

Enfuce’s CaaS ensures banks, fintechs, financial institutions and non-bank brands can become and remain fully PSD2-compliant, with programme management, data reporting and analytics, BIN sponsorship, card issuing, and effortless regulatory KYC/AML and payment scheme compliance all taken care of. With these unmatched levels of speed, flexibility and end-to-end programme management, clients can launch card payment services for customers with quicker time-to-market, give third-party service providers access to digital accounts, and give customers and end users even more choice in payment methods.

The launch of Authorisation Control comes hot off the heels of Enfuce’s recently secured €45 million in Series C funding from Vitruvian Partners, a global investment firm which is intent on supporting the most ambitious, high-growth companies. Enfuce is using the funding to kickstart its expansion across Europe and become the go-to payments partner companies in every sector, as embedded finance opportunities open up to meet urgent consumer and business demand.

Established in 2016 in Finland, and already the trusted number one issuer processor for more than 35 partners, including Pleo, Qred and Rocker, Enfuce is the only issuer processor that can launch CaaS for businesses in just eight weeks, an unrivalled onboarding timeframe compared to other providers that typically take up to six months to get partners up and running with embedded payments. Key applications for Enfuce’s services include expense management, neobanks, fuel cards, loyalty programmes, as well as corporate and consumer lending.

- 07:00 am

Abymap has partnered with freemium open banking provider Nordigen for direct access to customer bank accounts.

Abymap is a French financial software firm that was launched in 2020 by accountant Agnès Bichon and IT specialist Matthieu Paris. The two experts identified common challenges within existing accounting systems and the lack of clarity that was often present in these solutions. They also regularly observed how laborious and time-consuming administrative tasks are for small business owners. This resulted in them creating Ana, an ERP accounting platform that aims to simplify the day-to-day tasks of entrepreneurs and freelancers.

The solution is packed with features that help to stay on top of all financial processes, including generating invoices directly from quotes, calculating tax and pre-filling VAT declarations, product and inventory management, cash flow tracking, and more.

"Ana was created to help streamline enterprise resource planning and save time for busy small business owners. We value innovation and solutions that will help automate processes and add more data to our intuitive platform, which is why we decided to partner with Nordigen and implement their open banking solution," says Agnès Bichon, co-founder of Abymap.

The Nordigen integration enables Ana users to connect their business bank accounts directly to the platform through open banking APIs. Through the APIs financial data can be imported automatically into the ERP and customers can view and manage their finances using Ana’s dashboard.

"Small business owners have a lot on their plates and any solution that is able to help them manage day-to-day processes is incredibly beneficial. We are delighted to be Abymap’s chosen open banking provider, helping to further automate their procedures and enable them to provide their clients with the most straightforward way to manage their finances," explains Rolands Mesters, co-founder and CEO of Nordigen.