Help Yourself! Which Digital Banking Topping is for You?

- Leandro Gimeno, Business Development Manager at Strands

- 23.11.2016 10:45 am digital banking

Banks work hard to improve UX and innovate.

The majority of innovation initiatives focus on digital wallets, hiring UX consultancy services, adopting omni-channel technology, or improving mobile banking. On the other hand, perception vastly differs when you ask retail customers how they would rate banks in terms of innovation.

On this digital journey, banks want to streamline digital operations into mobile banking and save customers from having to visit branches. Likewise, customers don’t want to go to branches in person either, but rather, expect to manage their needs and requirements online themselves.

Customers will usually request:

Banks tend to think that personalization comes from big data analysis, financial advice, robo-advisors, and user experience, all blended in a nice, fancy, colourful front end. To sum up, what is the real, tangible difference that banks can offer as innovation?

Actually, aren’t all banks adopting e-payments or intelligent offers in a nice app just like most banks now? If omni-channel means “here’s my functionality, use it for whatever you need,” what will make your bank more successful?

Innovation then brings the conversation back to this question: “What do you want your digital banking to be like? Imagine suggesting to a customer: “Build your online banking the way you like.”

This then brings us to the concept of ‘topping’, much like we choose the add-ons for our favourite ice cream scoop. Banks can offer customization settings so each user can pick and choose whatever they find more effective for managing their daily finances.

Strands is the leading innovation company serving more than 450 banks worldwide, allowing banks to give customers a set of omni-channel financial tools to “customize online banking their way,” adding personalised topping to suit their taste.

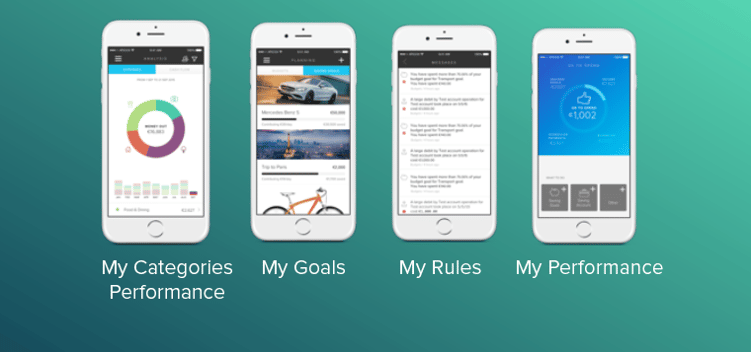

Imagine an online banking solution where customers can get an automated set of Expense and Income Categories, where each user can create their own sub-categories, set their own rules, and create their own budgets and goals, to decide what and how they would like their online banking user experience to be.

PFM (Personal Financial Management) is a proven technology, based on machine learning that allows users to set their own rules, in order to get personalised advice about their financial goals and performance.

PFM allows banks to let users add whatever “topping” they want to bolster their financial management needs. Help yourself! Which topping is for you?

This article originally appeared on blog.strands.com