Published

- 05:00 am

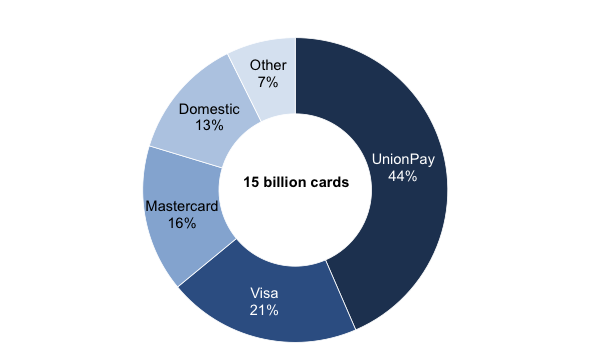

Brand new research from RBR reveals that the number of payment cards in circulation worldwide reached 15 billion at the end of 2017, with UnionPay continuing to hold the largest share

Financial inclusion initiatives drive growth in card issuing

There were 15 billion payment cards in circulation around the world at the end of 2017, up by 6% since the end of 2016, according to RBR’s most recent report, Global Payment Cards Data and Forecasts to 2023. As governments and central banks in developing markets continue to encourage financial inclusion, the number of cards has kept growing, providing further opportunities for card schemes.

Share of Payment Cards Worldwide by Scheme, 2017

Source: Global Payment Cards Data and Forecasts to 2023 (RBR)

UnionPay’s share increases as the Chinese market continues to expand

Growth in the Chinese card market has been strong for several years and the trend continued in 2017 which saw the number of cards in issue rise by 9%. The vast majority of the country’s cards are UnionPay-branded, and in 2017 the scheme accounted for 44% of the world’s payment cards, increasing its share by one percentage point compared to the previous year.

Visa (including Visa Electron, V PAY and Interlink) and Mastercard (including Maestro and Mastercard Electronic) account for 21% and 16% of global cards respectively; if China is excluded, Visa’s share is 36% and Mastercard’s 27%.

The RBR report shows that domestic schemes, usually found in the debit sector, are declining in most markets, as they are either dual-badged with, or replaced by, international schemes. However, they have seen something of a rebirth in a number of large markets in recent years. For example, India’s RuPay’s important role in a financial inclusion campaign has seen its share of the country’s cards rise to 49% since its launch in 2012.

Chinese regulations will only encourage growth in UnionPay cards

For many years, Visa and Mastercard cards in China were dual-badged with UnionPay, but a 2017 regulation prohibiting dual-badging means that this is no longer the case. As all Chinese cards issued for domestic use must be UnionPay-branded, banks are typically issuing UnionPay-only cards to replace existing dual-badged ones, while customers can request an international card for use abroad. RBR’s Daniel Dawson, who headed up the research team, said: “While some Chinese consumers and businesses will request a Visa or Mastercard card, UnionPay will account for the vast majority of Chinese cards for the foreseeable future. UnionPay will also aim to expand internationally, but Visa and Mastercard’s long history in other markets will enable them to withstand pressure from new competitors”.

- 09:00 am

Ingenico Group (Euronext: FR0000125346 - ING), the global leader in seamless payment, today announced that it has signed a partnership agreement with Chinese carrier Xiamen Airlines, to provide the online payments infrastructure for the company. As one of Asia's fastest-growing airlines, Xiamen Airlines' customers come from many different markets, which has led to a complex payments infrastructure. To sustain growth and simplify their payment operations, the company wanted to improve online payments acceptance with complied global Payment Service Providers like Ingenico. This will enable the carrier to increase the number of local payment methods and currencies it accepts, and help optimize the customer experience when purchasing airline tickets online. Ingenico's full-service model with its large portfolio of cards and alternative payment methods, extensive network of local acquirers, and strong regional expertise all contributed to Xiamen Airlines' decision.

Xiamen Airlines was founded in 1984, and today covers a network of around 400 domestic and international destinations, with one of the most modern fleets in the world. The company was recognized as 'The Airline Offering the Best Services' by Chinese passengers for years. As Xiamen Airlines expands operations across Asia and into the far corners of the world, it became increasingly important to offer consumers a localized shopping experience that includes payment options in their preferred currency and with local payment methods. To that end, Ingenico provides Xiamen Airlines with full-service payment processing and value-added services, as well as connections to a series of local acquirers, to drive improved acceptance rates.

"Ingenico has a long track record in the industry, working with many of the world's best airlines. As such, they understand the unique requirements and opportunities that come with operating a growing airline," said Mr. Guo Kaiquan, E-commerce Accounting Manager of Xiamen Airlines. "As consumer expectations change, it is important to us to continue to offer a seamless online purchase experience that reflects our commitment to service and customer satisfaction."

Ingenico works with many of the world's best-known brands from the Travel & Tourism industry. With over 20 years of vertical experience, the company understands the unique payments requirements and has a proven track record of growing revenue and optimizing sales for airlines. Today, Ingenico serves over 100 airlines from all over the world, including a number of the Top 10 best airlines according to the World Airlines Awards 2018.

"Xiamen Airlines continues to pursue innovation and excellence with the aim of building a world-class airline. They understand very well that to continue their growth into new markets, customer experience is key," said Gabriel de Montessus, SVP Global Online (Retail BU) for Ingenico Group. "Ingenico has a long history of processing payments in China and across the world and knows the local customs, preferences and regulations. With our payment solutions and network of local acquirers, Xiamen Airlines is ready to expand operations while providing a familiar and seamless payment experience to travellers anywhere"

- 03:00 am

More than half of UK consumers (54 percent) would be ready to use biometric payment cards if they were available at their bank today, according to new research revealed by digital security leader Gemalto and conducted by GfK*. For 82 percent of them, it would even become their preferred payment card – generating a clear 'top of the wallet' effect. These innovative cards with integrated fingerprint readers let users authorise payments with a simple touch of their finger on the sensor, as an alternative to the PIN code.

If British consumers are to replace their current payment cards, they need them to be more secure than what they currently have (88 percent), to be offered by a trusted bank (79 percent), to be easy to use (69 percent) and to be one that simplifies their life (60 percent).

For a large majority, biometric cards clearly tick all the boxes. Eight out of 10 consumers believe that this new card will be better in terms of convenience and security. Key advantages include: no need to remember different PIN codes, a more secure experience ("no more risk of someone stealing my PIN code when I pay") and more opportunities to pay contactless thanks to higher spending limits. Additionally, the card doesn't rely on a battery and only uses power from the payment terminal to work; this means there is no limit on the number of transactions.

Some consumers also expressed concerns about using biometric technology. 41 percent feel afraid that their fingerprint won't work all the time and more than a third (37%) about it being compromised.

However, these concerns should be alleviated as consumers learn more about the technology. For example, biometric cards will be able to fall back to a PIN code authorisation if for any reason the fingerprint reader malfunctions. The fingerprint data is also securely stored in the card's chip. It never leaves the card. It's not kept on the bank's servers nor sent to a personalization bureau, so to avoid the risk of it being stolen or compromised.

The findings show that Britons are enthusiastic about the potential of biometric cards, but also proves the need to build confidence in order to convince all UK cardholders to take up this new payment method. The majority of them, mainly young active contactless users or multi-banking product owners in the 40-50 age range- are already convinced, but there is also one third of the population that will need more time and proof to feel confident using biometric payments.

Responding to the findings, Howard Berg, SVP Banking and Payment at Gemalto commented, "We are delighted to see that the British public is ready to embrace this new generation of biometric payment cards. Our payment experts have worked hard to design a card that's not only safe and secure but also easy to use and which provides a more convenient payment experience than ever before. Banks are showing great enthusiasm with ongoing trials and we look forward to launching biometric cards in the UK in the near future."

- 09:00 am

ICS BANKS Notification System is created to provide the bank with a notification mechanism where certain messages or advertisements will be displayed for certain customers, once their accounts or customer number are keyed in the system, in order to be addressed in a proper way.

For example, if a customer is entitled for a new credit card, the bank can add a specific notification where the notification will be displayed once his customer/ account number is entered by the teller on the screens of certain functions (Cash, Cheque deposit, inquiries).

The bank can perform specific/bulk notifications or define special notifications that are displayed for the teller once the accounts or customer number are keyed in the system.

With the systems’ flexible parameters, the bank can personalise the notifications to specific customers according to specific conditions, and create automatic notifications according to its customers’ needs.

The system provides the bank with the facility to activate or deactivate specific notifications concerning a customer or an account. The system provides also the bank with the facility to activate or deactivate email and SMS services for each defined notification.

By deploying this system, the bank will build customer centricity and receive higher customer satisfaction.

- 06:00 am

SWIFT today announces the introduction of Payment Controls, an intelligent new in-network solution to combat fraudulent payments, and to help strengthen its customers’ existing security.

The commercial availability of the service marks an important milestone in SWIFT’s Customer Security Programme (CSP) – a community initiative launched in 2016 that has increased security and trust across the global financial community. Payment Controls helps payment operations teams mitigate fraud risk in real-time through its unique alerting and reporting capabilities. The service may be set to flag, hold, release or reject high-risk or uncharacteristic payments in real-time, according to business needs. Initially targeted at smaller financial institutions, the utility service is hosted in the SWIFT cloud to allow users immediate access, with no hardware or software installation or maintenance.

Payment Controls is an important safeguard for firms as the frequency and speed of payments increases. The service bolsters SWIFT’s global payments innovation (gpi) – the new standard in global payments, which has dramatically improved cross-border payments since it was launched last year.

As part of gpi, and to further strengthen customer defences, SWIFT will introduce a new ‘stop and recall’ capability that will enable banks to immediately stop and recall a payment anywhere in the chain. The new feature will provide another barrier against fraud – mitigating business disruption and financial losses in the face of rising threats.

Luc Meurant, Chief Marketing Officer at SWIFT, said: “The growing threat of cyberattacks has never been more pressing, and banks need to be able to verify the integrity of payments in real time. Payment Controls demonstrates our commitment to playing our part in protecting the security of the wider financial services industry. I am confident that the new service will be an important weapon in the fight against fraud.”

Mark McNulty, Global Clearing and FI payments Head, at Citi, said: “Putting the right security tools in place is vital for any bank in mitigating payment fraud risk. The launch of SWIFT’s Payment Controls service is a very welcome step towards reinforcing and safeguarding the security of our ecosystem. For banks, it screens transactions in-flight and flags, holds or rejects transactions based on risk policies – ultimately protecting their operations, fighting cyber-crime and making the community safer for everyone.”

Patricio Melo, Executive Vice President of Technology and Operations at Banco Davivienda, said: For Davivienda it is a privilege to work with SWIFT, especially at this pivotal moment in the financial industry, in which banks should be working towards strengthening their payment processing systems and reducing the threat of fraud. Through the service provided by SWIFT’s Payment Controls, we are confident that our system will not only be better protected from fraud risk, but allow us to then deliver a trusted service to our clients.”

- 07:00 am

Brand new research from RBR reveals that the number of payment cards in circulation worldwide reached 15 billion at the end of 2017, with UnionPay continuing to hold the largest share

Financial inclusion initiatives drive growth in card issuing

There were 15 billion payment cards in circulation around the world at the end of 2017, up by 6% since the end of 2016, according to RBR’s most recent report, Global Payment Cards Data and Forecasts to 2023. As governments and central banks in developing markets continue to encourage financial inclusion, the number of cards has kept growing, providing further opportunities for card schemes.

UnionPay’s share increases as the Chinese market continues to expand

Growth in the Chinese card market has been strong for several years and the trend continued in 2017 which saw the number of cards in issue rise by 9%. The vast majority of the country’s cards are UnionPay-branded, and in 2017 the scheme accounted for 44% of the world’s payment cards, increasing its share by one percentage point compared to the previous year.

Visa (including Visa Electron, V PAY and Interlink) and Mastercard (including Maestro and Mastercard Electronic) account for 21% and 16% of global cards respectively; if China is excluded, Visa’s share is 36% and Mastercard’s 27%.

The RBR report shows that domestic schemes, usually found in the debit sector, are declining in most markets, as they are either dual-badged with, or replaced by, international schemes. However, they have seen something of a rebirth in a number of large markets in recent years. For example, India’s RuPay’s important role in a financial inclusion campaign has seen its share of the country’s cards rise to 49% since its launch in 2012.

Chinese regulations will only encourage growth in UnionPay cards

For many years, Visa and Mastercard cards in China were dual-badged with UnionPay, but a 2017 regulation prohibiting dual-badging means that this is no longer the case. As all Chinese cards issued for domestic use must be UnionPay-branded, banks are typically issuing UnionPay-only cards to replace existing dual-badged ones, while customers can request an international card for use abroad. RBR’s Daniel Dawson, who headed up the research team, said: “While some Chinese consumers and businesses will request a Visa or Mastercard card, UnionPay will account for the vast majority of Chinese cards for the foreseeable future. UnionPay will also aim to expand internationally, but Visa and Mastercard’s long history in other markets will enable them to withstand pressure from new competitors”.

- 03:00 am

Mandatum Life will launch a new online trading service based on the Saxo Bank Group’s (Saxo Bank) state of the art investment and trading technology in the first half of 2019.

The service opens up a uniquely broad global investment universe both for Finnish stock investors as well as advanced tools and services for active traders.

The instrument universe is truly extensive, including more than 35,000 different financial instruments from global capital markets including, stocks, ETFs, currencies, commodities.

“We see great potential in this market, as Finland is lagging behind other Nordic countries when it comes to investing. Mandatum Life wants to offer more alternatives for Finnish investors and the global dimension of Trader service brings new alternatives for global diversification to all Finnish investors”, the CEO of Mandatum Life Petri Niemisvirta says.

“Our mission is to make Finns wealthier, so this is a natural next step within our strategy”, Niemisvirta continues.

“The importance of digital services is growing all the time and we want to offer the very best tools for our clients”, Niklas Odenwall, VP, Trading and Execution Services, Mandatum Life, says.

“Clients can pick from several different investing and trading applications, so this is a very comprehensive offering catering to all investor segments with different levels of investment experience and wealth.”, Odenwall says.

The technology behind Mandatum Trader is the ground breaking Saxo Bank technology. Saxo Bank is a Danish fintech unicorn delivering global capital markets access and Banking-as-a-Service to partners. Saxo Bank’s investment technology forms the technology back bone of investment solutions for more than 120 financial institutions globally.

CEO and founder of Saxo Bank, Kim Fournais, comments: “We are proud to partner with Mandatum Life and support the mission to provide Finnish investors with better global investment opportunities. Saxo Bank has always strived to democratize trading and investment to empower everyone with the best tools and opportunities to navigate their own financial destiny. With Mandatum Life’s new solution, Finnish investors and traders get a much better basis for managing their investments and build diversified portfolios across asset classes and geographies.”

Mandatum Life is responsible for onboarding and client identification, Saxo Bank is responsible for the trading services and the technical side of the platform.

- 08:00 am

Jumio, the creator of Netverify® Trusted Identity as a Service (TIaaS), today announced a partnership with Engage Technology Partners Ltd., to integrate Jumio’s online identity verification technologies into Engage’s cloud-based recruitment solutions, designed to help end-hirers, agencies, payrolls and workers navigate and simplify the recruitment process.

Right to work checks are a compulsory step in the UK recruitment process. Employers are required to see the applicant’s original identity documents, check that the documents are valid with the applicant present, make and retain copies of the documents and record the date the check was made. This manual process can be time-consuming for hiring companies and exposes them to potential data breaches and GDPR scrutiny.

The maximum fine for hiring illegal workers is £20,000 per illegal worker, so even a handful of illegal workers on the books could easily cripple a business. Employers knowingly hiring someone who does not have the right to work in the UK could face up to five years in jail (whereas the illegal worker would face six months).

The integration enables Engage to verify passports, ID cards, biometric residence permits and other forms of identification from over 200 countries automatically to verify workers’ eligibility and actual identity. Workers receive an email or text message invitation to provide their ID and right to work documentation via unique URLs, linking them to the Engage platform, where they can upload or use a camera to take pictures of their documents and of themselves. The automated verification process is then run by Jumio’s Netverify solution, while workers are kept in the loop via notifications. As a PCI-DSS compliant solution, Jumio is also helping Engage meet the stringent data protection and privacy requirements of GDPR.

“Jumio is excited to integrate our online identity verification solutions into Engage’s recruitment workflow to help automate and streamline the right to work verification checks,” said Stephen Stuut, Chief Executive Officer of Jumio. “Our leading identity verification solutions, which leverage biometrics, AI, machine learning, liveness detection and verification experts, are designed to definitively assess whether someone is who they claim to be. Integrating this technology for right to work checks and Engage’s end-to-end recruitment software will help Engage vet new workers quickly, securely and compliantly.”

“Our mission is to connect end-hirers, agencies, payrolls and workers on a self-service platform that seamlessly navigates the entire recruitment process with incredible efficiency, from vacancy to billing,” said Alex Fraser, Marketing Director at Engage. “Working in partnership with Jumio, we're able to provide instant verification to prove that employees are who they say they are and can now offer the necessary compliance with right to work regulation to our clients, especially in the contingency staffing market."

Ensuring that every employee has the right to work in the UK is one of the core duties of an employer. It’s not an extra, or a nice to have: it’s essential for all businesses, regardless of size or industry sector. Integrating a secure and reliable identity verification solution helps Engage deliver a more complete solution to its business customers, comply with the Home Office guidelines, avoid compliance penalties and reduce the likelihood of regular spot checks by the HM Revenue & Customs.

To learn more about Jumio and its award-winning solution, please visit: https://www.jumio.com/trusted-identity/netverify/.

Henry Umney

CEO at ClusterSeven

Latest research forecasts that spending on RegTech (Regulatory Techno see more

- 02:00 am

Viettel's real time billing system (vOCS 3.0) was awarded the Gold Stevie Award for "Best New Product or Service of the Year" entry at the International Business Stevie Awards held in London,England on October 21st, 2018 by the time zone of Vietnam.

Viettel vOCS 3.0 is the only IT product of Vietnam winning this award in the year along with Ooredoo - Qatar with the fastest 5G service in the world, Singtel - Singapore with the interactive sales system, Telkom - Indonesia with the mobile application for navigating locations for naval ships, etc. It is highly appreciated for the creativity and significant influence on the large number of users when being customized to suit each customer's specific needs. Currently, it has been put into use in 11 countries of Viettel with 170 million mobile subscribers with the capacity of each site serving up to 100 million subscribers. The most striking feature of vOCS 3.0 lies in its ability to design each single specific charge package for each user which has not ever been done by any OCS in the world.

As stated by Ms. Clara, Communications Director for Asia region when evaluating Viettel's winning of 2018 IBA Stevie Awards, all members of the judging board had positive and impressive comments on Viettel's vOCS and agreed to award the gold prize. This product demonstrated both the insight of researchers, software developers and the ability to tackle a major problem in the telecommunications sector, which is the fear and hesitation among data service providers in unifying or integrating voice and data into one real-time billing system. The judging board was highly expected to witness the creation of a new business model from this highly-acclaimed real-time billing system.

Viettel Group's real-time billing system (vOCS 3.0) completed its support on the Cloud/NFV virtualization platform for next version vOCS 4.0, which is intended to introduce many features on Mobile Virtual Network Operator (MVNO), Network Slicing as well as readily calculate charge for IoT/5G subscribers.

When the new version 4.0 is completely launched, it will turn Vietnam into one of the OCS-producing countries that support the global trend, namely advanced virtualization technology in order to save overhead cost and facilitate management activities, thereby opening up worldwide business opportunities. This encouraged Viettel to send bidding invitations to more than 30 international telecommunications operators to bring this product to the international market.

Asian markets such as Indonesia, Philippines, Pakistan, etc., will be first selected to expand vOCS 4.0 version with the latest and most distinctive technological strategy as well as the best customer care.

IBA - International Business Stevie Awards is an annual international business award held since 2003 to honor great achievements and positive contributions of businesses and individuals globally to the benefits of the community, including IT and telecommunication fields. IBA 2018 did attract more than 3,900 nominations from all types of organizations / businesses in 74 countries.