Published

- 06:00 am

FBS, a leading online trading platform, has been recognized as the “Most Reliable Forex Broker 2023” by the International Finance Expo. This prestigious title serves as a testament to FBS’s dedication to providing secure and trustworthy financial services to more than 27 million of its clients in over 150 countries.

Since its foundation in 2009, FBS has recognized the paramount role of people’s trust and gradually fortified the security of its products to protect user legitimacy. These actions have earned FBS the title of the “Most Reliable Forex Broker 2023” and included several major aspects, such as

Global Regulation: FBS is licensed by such reputable financial regulators as Finance Service Commission, Belize, Cyprus Securities and Exchange Commission, and Australian Securities & Investments Commission.

Enhanced Product Security: The global broker takes strategic security measures, including server colocation with top providers, the use of the latest DDoS protection systems, and its own trading proxy Anti-DDoS servers.

Fraud Monitoring and Control: FBS approaches advanced data encryption methods and requires every user to undergo stringent ID and payment means verification.

Customer-Centricity: With its 24/7 multilingual client support and free educational resources, including customized FBS VIP Analytics, the global broker aims to cater to clients’ needs and support them on their trading journey.

“Acknowledgement of FBS as the Most Reliable Forex Broker of 2023 is a great honor and a powerful impulse for our brand to continue reimagining our products, making them even more convenient for our clients,” said Diego Lima, FBS’s Business Development Manager for the African Region. “Moreover, we are constantly enhancing our platform and clients’ data security to make their experience with FBS more comfortable and trustworthy.”

- 08:00 am

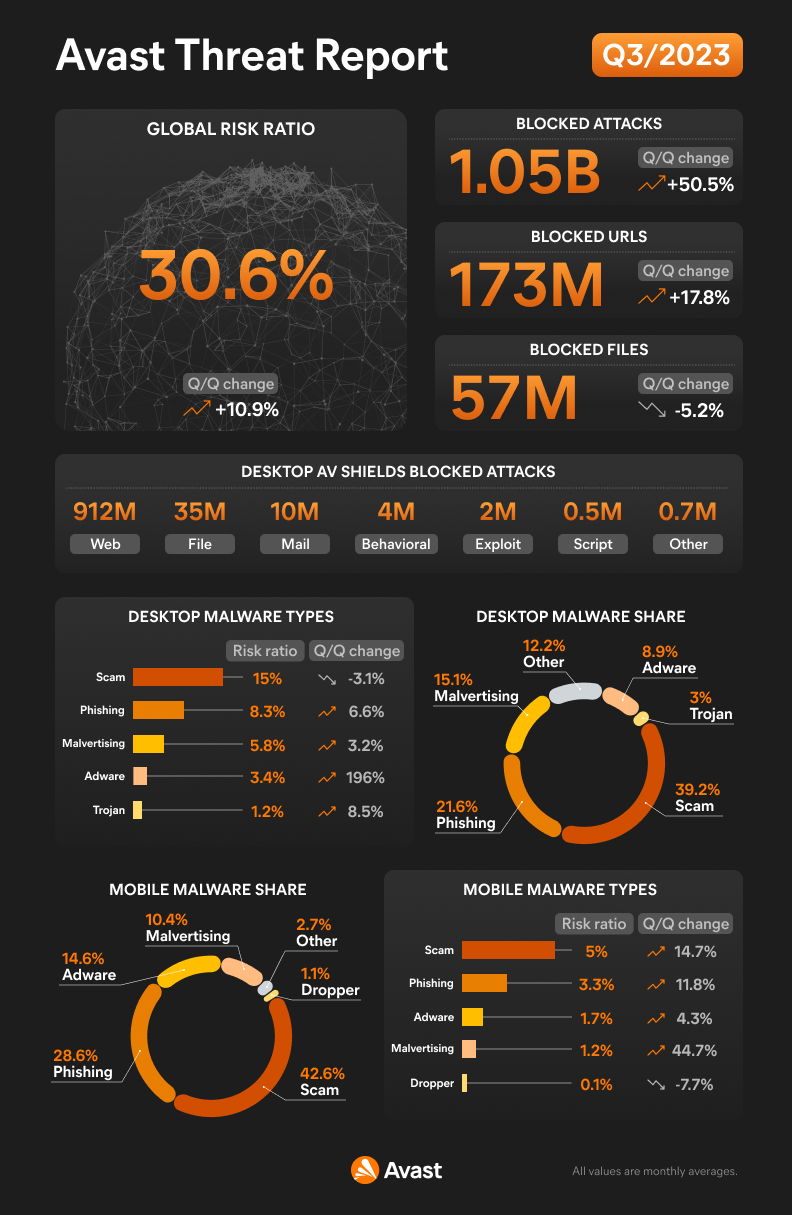

Although less people spent time online in July, August and September, Avast, a leader in digital security and privacy, and a brand of Gen™, has blocked over 1 billion attacks per month – a record high. The latest Avast Threat Report, released today, breaks down some of the greatest risks in our connected digital world, from cybercriminals using social engineering and AI while running scams to the rise in adware and malvertising.

“Typically, during vacation times people spend less time online, and in turn, we see less cyber threats. This year, we were blown away to see the opposite,” said Jakub Kroustek, Avast Malware Research Director. “Apparently the days of cyberthreat seasonality are long gone with the increased use of AI and advanced tools at the fingertips of cybercriminals. Whether people are using social media, dating online, streaming shows or even just answering emails, it’s important they’re aware of potential threats when they go about their day-to-day activities.”

Threats Hidden in Ads and Spyware

Adware: Adware doubled globally from July through September 2023 over the previous quarter. A new strain of mobile adware dubbed “Invisible Adware” has already gathered over two million downloads in the Google Play Store. These applications display advertisements while the device screen is off, gaining revenue through fake clicks and views. This is not only contributing to ad fraud but can also impact battery life and potentially install dangerous software without a person’s knowledge.

Malvertising: Malvertising activity spiked significantly, especially during September as people returned to school and work after vacation. Using pop-up messages and push notifications, cybercriminals exploit recognizable logos of well-known companies, usually informing people that their device has been infected with a virus. These pop-ups lead to a phishing website where they are asked to enter credit card information under the guise of providing antivirus services. Push notifications are especially effective on mobile, where they can be easily disguised as system notifications such as an unanswered call or a new text message.

Spyware: People should also be wary of spyware apps on their mobile devices, which are now more difficult to spot. One of the most recent is the fake Red Alert missile waring app that is used by many in Israel to monitor missile warnings. This app was distributed through a phishing website and contained identical features as the original with added abilities that allow it to spy on its victims. This included extracting the call log, SMS lists, location, and emails.

Finance and Dating Scams

Finance Scams: While people were enjoying time away from their devices, scammers were hard at work. The risk of encountering scams has grown significantly, with the most affected countries being Japan (+19%), Greece (+17%), United States (+14%), Austria (+13%), and Germany (+12%). Social media sites have become global platforms for spreading highly targeted and precisely tailored cryptocurrency scams. These scams are often initiated with a deepfake video of a famous personality, such as Elon Musk, Mr. Beast, Donald Trump and others, promising a significant amount of bitcoin if people sign up for a promoted platform and pay a small fee to verify their account. Victims find that not only is the promised bitcoin unattainable, but any transferred funds to the platform are irretrievably lost to the scammers.

Dating Scams: Avast researchers recently discovered a threat called Love-GPT. This AI-driven tool helps scammers create realistic personas on popular dating apps, allowing them to reach out to even more victims. The level of dating scams increased by 34% globally, with Belgium, Germany, Canada, and the United States being the most frequently targeted countries.

- 01:00 am

iPipeline, a leading global provider of comprehensive and integrated digital solutions for the life insurance and financial services industry, announced today that Pat O’Donnell, a technology industry veteran with more than three decades of experience, has been appointed Chief Executive Officer.

Pat will replace Deane S. Price, who has served as the company’s interim CEO since February 2022. Price joined iPipeline after more than 10 years with fellow Roper Technologies business, Aderant, where she held the role of CEO. O’Donnell’s appointment is effective immediately and Price will remain with the organization as an advisor, assisting with the transition. O’Donnell will be responsible for the global iPipeline organization and will report to Satish Maripuri, Group Executive, at Roper Technologies.

“Pat is a proven leader with a growth mindset in the technology sector, with robust experience and proven success in the industry. We are excited to welcome him to iPipeline and Roper Technologies,” said Satish Maripuri. “Pat’s focus on customer intimacy, innovation, driving M&A, and building high performance cultures is key to iPipeline’s ongoing commitment to innovate and strategically transform the global industry -- life insurance, protection, financial services, and pensions -- through the company’s innovative technology solutions. We look for Pat to build upon the strong and solid foundation iPipeline has built and I want to thank Deane for her leadership at iPipeline during this interim period.”

O’Donnell brings extensive industry knowledge and experience to this role, having most recently served as CEO of Ministry Brands, the leading provider of software and services for faith-based, non-profit, and other purpose-driven organizations. During more than three years in his role with the organization, O’Donnell played a key role in the company’s success and oversaw a period of transformation and growth.

His experience includes serving as Senior Vice President, and later as President, of FLEETCOR, an Atlanta-based leading global business payments company. O’Donnell also held roles of increasing responsibility, including serving as Senior Division Vice President and Division Vice President of Major Accounts during his nearly 24 years with ADP, a member of the Fortune 500 and a global technology company providing human capital management solutions. O’Donnell is a graduate of West Chester University with a bachelor’s degree in economics. Additionally, he earned the Six Sigma designation and the Project Management Profession (PMP®) certification.

“I am honored to be appointed to lead iPipeline, a company that not only is a pioneer in the industry but one that continues to be a leader, with a global footprint, a strong portfolio of innovative technology solutions, and a talented and driven team of Pipers,” said Pat O’Donnell, Chief Executive Officer at iPipeline. “I look forward to working with the team to collaboratively build upon the foundational success of iPipeline as we advance our strategy to the next level.”

- 06:00 am

Time is running out for British AI, data management and tech specialists to take advantage of a new, streamlined pathway offering career advancement in Western Australia (WA).

WA is a major player globally in the emerging critical mineral industry, renewable energy and medical technology.

WA also boasts higher wages and a cheaper cost of living compared to Britain, along with the lifestyle benefits of a State which enjoys over 200 days of sunshine every year.

Under the terms of the UK-Australia Free Trade Agreement signed two years ago, the two countries agreed to open up a special visa scheme to allow British citizens the chance of working in Australia.

The Innovation and Early Careers Skills Exchange Pilot (IECSEP) was established to offer a smoother pathway for early career professionals and innovators from the UK to work Down Under.

This program will mean opportunities for innovators in various industries - Research and Development, Renewable Energy, Artificial Intelligence, Medical Technology, FinTech, AgriTech, Audio-visual and Cultural.

One of the industries where workers can benefit is data management, AI and tech - but there isn’t long left before the door shuts on the opportunity.

The IECSEP closes its window for new applications on November 20 this year, blocking off a potentially smoother process to make the move.

There are two streams under IECSEP:

the Early Careers Skills stream, which will allow participants to undertake a short-term placement, secondment, or intra-corporate transfer for up to one year in Australia.

the Innovation stream, which will allow highly skilled and experienced participants, with a demonstrated contribution to innovation, to undertake opportunities for up to three years in Australia.

Total visas available under the IECSEP will be 1,000 in the first year, and 2,000 in the second year of operation, during which the program will be reviewed.

While the scheme runs across the whole country, Western Australia is pushing the opportunities the State offers - both for employment and lifestyle.

Those interested in pursuing their careers in Western Australia at a time of huge growth can visit https://likenoother.wa.gov.au/

For information on the Innovation and Early Careers Skills Exchange Pilot, and an application form, visit the Department of Foreign Affairs and Trade’s information page https://www.dfat.gov.au/publications/trade-and-investment/benefits-tech-entrepreneurs-and-innovators/iecsep

The Skilled Migrant Employment Register helps skilled migrants to connect with Western Australian jobs. For more information visit https://migration.wa.gov.au/

- 02:00 am

NALA, an East African financial technology company, has grown rapidly in recent years via geographic expansion, product innovation, and improvement in financial infrastructure. One of the critical elements of NALA’s growth has been its methodical approach to pursuing payment licenses. Holding licenses permits the company to own more steps in the payment flow, including direct integration with banks and mobile money operators.

The company received approval from the National Bank of Rwanda for a Payment Service Provider license, which will enable direct integration with banks and mobile money operators locally. This is a major milestone towards NALA’s mission to build strong payment networks in Africa, and a signal of their intention to continue investing in Rwanda, given the country’s position as a global hub for business and investment.

NALA has been operating in Rwanda since 2021, partnering with other companies to disburse remittance payments to bank accounts and mobile money wallets. Since then, the company has processed 10,000+ transactions and helped thousands of Rwandan diasporans send money home. This has resulted in over one billion

Rwandan Francs being sent home from abroad. The new PSP license enables NALA to process disbursements and collections in-house, reducing cost and increasing reliability for those sending money to and collecting money from Rwanda.

With this new license in hand, NALA can now offer:

● Payment gateway services, allowing merchants to collect payments from local channels such as mobile money or cards

● Direct integration with telcos and banks, opening up greater reliability and control as well as reduced overhead costs

● Payment processing on behalf of third parties, such as other remittance services

NALA group COO Nicolai Eddy said, “Enabling direct integration to banks and telcos allows us to address some of the most pressing and sticky challenges that individuals and businesses face when moving money across Rwanda’s borders. Our

new PSP license enables us to build these capabilities under our roof, which means we can improve the quality of service and reduce cost.

We have worked closely with the Bank of Rwanda to complete the appropriate steps to become licensed as a Payment Service Provider. With this new license, NALA commits to supporting and collaborating with the Rwandan regulator and the

relevant government agencies to accomplish our shared ambitions.”

The approval comes after the rollout of the Rwanda Fintech Policy 2022-2027, which aims to firmly establish Rwanda as a regional financial center and advance the nation’s financial inclusion. The report states:

“The development of the Rwandan fintech landscape and the establishment of Rwanda as a fintech hub will attract investment and provide the technology and financial services needed to make Rwanda a global financial center... Fintech also

enhances the reach and efficiency of financial services more broadly to boost financial inclusion beyond payments.”

Rwanda’s vision for economic advancement, not just of their nation, but of the region and the continent aligns closely with NALA’s mission to increase economic opportunity for Africans worldwide.

Jean-Marie Kananura, Chief Investment Officer at Rwanda Finance Limited commented:

“The establishment of NALA aligns perfectly with our aspirations of positioning Rwanda as a Fintech hub. NALA’s presence will undoubtedly contribute to our efforts to drive digital and financial inclusion in Rwanda. We are excited about this

development as it underscores our immediate role in facilitating different forms of investments to structure through KIFC. Working closely with different stakeholders, we have put in place the right framework and policies to create a conducive

environment that will attract more Fintech companies like NALA in our ecosystem to drive innovation and growth of our financial sector.”

NALA continues its operational activities in Rwanda and hopes to support the nation’s ambitions to innovate and advance technologically, especially as a lever to support opportunities for its growing youth population.

The NALA App is available for download via the App Store or Play Store from the US, UK, and Europe.

Despite the many options for sending money to Africa from abroad, the continent continues to be the most expensive destination to send money to. The World Bank estimates average transfer fees to Africa at ~9%. Further, many existing options

include hidden fees that make it hard to discern the true cost of sending money. NALA is working towards changing the paradigm of financial tools for Africans by providing fair and transparent services to empower people with control over their

finances.

- 08:00 am

Delio, the provider of configurable technology and deal structuring solutions has released a report exploring how investment vehicles are driving innovation and democratization in private markets.

Delio’s research has found that changing market dynamics and increased demand from clients wishing to access private market opportunities have meant that financial institutions have had little choice but to adapt their propositions. Offering access to alternative assets is now essential for financial institutions wanting to stay ahead of the curve.

Gareth Lewis, Delio’s Chief Executive comments “While multiple approaches may be taken to do this, the ultimate focus lies in creating opportunities in unlisted assets that do not require investors to deploy hundreds of thousands to benefit from the types of returns that make them so attractive. It is about opening private markets to a new wave of modern investors who understand the unique intricacies of alternative assets, the risks associated with them, and the potential for long-term returns if utilised correctly as part of a diversified portfolio.”

While historically, the ability to structure deals to meet this criteria would only have existed with experts in the largest banks and financial institutions, many are now looking to outsource this, making the launch of investment vehicles more accessible to a broader range of firms.

Given the range of vehicles available including both off-the-shelf and bespoke structures, the previously untapped pool of capital held by non-institutional investors, estimated by McKinsey to be worth $45tn, is now being unlocked. Some vehicles are facilitating individual investments as small as £5,000, meaning firms can target certain types of investors who would have previously had no realistic access to these types of assets, without compromising on regulatory commitments.

As explored in the report, the use of investment vehicles alongside digitising and automating operational processes through third-party fintech suppliers gives firms the ability to offer their clients access to private markets deal flow in an organised and professional way. This, in turn, widens the pool of investors that can deploy their capital to alternative assets, all without the need to build their own expensive in-house systems.

As an expert in the field, Delio designs, builds and develops enterprise-grade investment vehicles that can be fully integrated with their market-leading technology to deliver an intuitive investor experience that supports a wide range of use cases.

Each vehicle possesses unique characteristics to serve a variety of purposes and Delio’s structuring experts work with clients to advise which is most suitable depending on the firm’s objectives, the profile of their investor base and their geographical location, amongst other factors. Among the most popular are a Luxembourg Special Purpose Vehicle (SPV) and a Reserved Alternative Investment Fund (RAIF).

Businesses such as Investa Solutions are paving the way in demonstrating the success that can be achieved by having a one-stop solution that seamlessly integrates investor onboarding, investment distribution and administration support. Tullio Musso, CEO and Founder of Investa Solutions, commented “The efficiency I’ve gained through using the Delio platform is fantastic. The scalability factor is making a real difference and as a result, I’ve managed to grow quickly while still providing a high-touch service to all. I’m a strong believer in allowing more and more investors to access private markets and this solution is a huge step forward towards that.”

With the value of private equity assets outpacing public market capitalisation nearly threefold over the last 20 years, it’s clear why financial institutions and individual investors alike have sought to deploy their capital to alternative assets. The potential for long-term returns if utilised correctly are great, making it almost a matter of when, and not if, financial institutions engage with external investment structuring specialists.

- 09:00 am

Pan-European flexible payment provider Hokodo and US-based fintech company Balance have released a joint research report which explores trends and attitudes among B2B sellers about cross-border payment terms.

The report features data collected from a survey of 200 merchants and marketplaces across the UK, US, France and Germany, in order to discern what businesses are looking for in a global payment terms solution.

Growth is on the agenda in 2024 - the report’s findings show that 44% of B2B sellers surveyed are preparing to extend their e-commerce operations into Europe next year, while 34% of B2B sellers plan to expand into the Americas. Payment terms have a significant part to play in this, as 65% of B2B sellers consider that offering payment terms is vital for influencing business growth in their respective markets. This suggests that growth could be stunted without access to flexible B2B payment terms.

“The report shows that many businesses are making payment terms part of their long-term strategy,” says Louis Carbonnier, Co-founder and President of Hokodo. “Of particular note is the urgent requirement of smaller businesses, with 79% of UK and US respondents within the $80 million-$400 million revenue range noting global payment terms as a critical lever for business growth.”

The report demonstrates that cross-border payment terms are essential in order for businesses to secure meaningful, long-term growth. Balance and Hokodo’s partnership encompasses all the key elements of international payment terms management, from credit scoring, fraud mitigation and payment processing, through to insurance, financing and collections, to empower global merchants to achieve their growth goals.

- 02:00 am

Islamic Finance, guided by Shariah principles, is a values-driven approach to investment that promotes justice and prohibits unethical, speculative, and usurious practices. It plays a pivotal role in supporting the real economy and boosting the global financial system's resilience. Since the war of the Soviet Union and the emergence of new nation-states in 1991, the Muslim-majority republics of Central Asia have witnessed the introduction of Islamic banking and finance to the region. The Islamic Development Bank (IDB) has played a significant role in facilitating the expansion of financial projects in the area that adhere to Islamic principles, including the prohibition of usury or riba.

This report delves into the landscape of Islamic Finance in Central Asian countries, including Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan, and Uzbekistan. These nations are home to approximately 80 million people, with roughly 85 percent of the population identifying as Muslims. Kazakhstan has a Muslim population representing 71 percent, while the other four Central Asian countries have approximately 90 percent Muslim populations. This region holds immense potential for Islamic Finance.

Kazakhstan and Kyrgyzstan are pioneers in this field, having formally introduced Islamic financial institutions over two decades ago. Despite more than two decades of continuous efforts and initiatives by local Muslims, Central Asian states have made relatively modest contributions to the global Islamic Finance and Banking industry. However, Islamic Finance has significant growth prospects in these regions due to the sizable Muslim population and the presence of international Islamic financial institutions (IFIs), such as the Islamic Development Bank (IsDB) Group, as noted by UNDP in 2021. Refinitiv's 2022 report indicates that in terms of Islamic Finance development, Kazakhstan is the fastest growing central Asian Islamic banking market in 2021 and ranked 24th globally, surpassing the global average, and leads the Central Asian markets. The Kyrgyz Republic, Tajikistan, and Uzbekistan ranked 38th, 46th, and 49th, respectively, while Turkmenistan lagged significantly behind, securing the 85th position.

Islamic Finance in Central Asia

The Islamic Development Bank (IsDB) has been a major partner in the development of Central Asia since the early 1990s. Its mission is to alleviate poverty, promote human development, science, technology, Islamic banking, finance, and enhance cooperation among member countries. The IsDB focuses on six strategic pillars, including economic and social infrastructure support, inclusive social development, cooperation between member countries, private sector development, Islamic finance sector development, and capacity building. It mobilizes funds and invests using Shari’ah-compliant financing methods while providing technical assistance to member countries. Kyrgyzstan was the first country in the region to join the IsDB in 1993, followed by Turkmenistan in 1994, Kazakhstan in 1995, Tajikistan in 1996, and Uzbekistan in 2003.

Geographical representation of Central Asian Countries

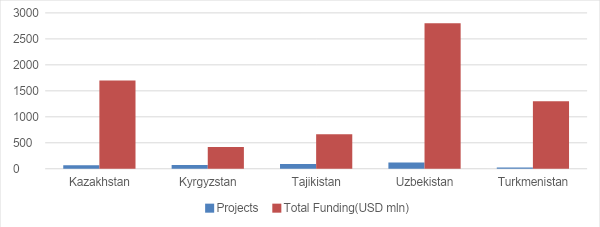

As of 2022, the IsDB has funded 378 projects in Central Asia worth US$6.88 billion. In 2018, Kazakhstan hosted the IsDB's Regional Hub responsible for operations in Central Asia. This hub plays a key role in coordinating the IsDB's work in the region. The IsDB's private sector arm, the Islamic Corporation for the Development (ICD), also plays an important role in Central Asia. The ICD provides Islamic financing and advisory services to support the development of the private sector in the region. The figure 1 represents the total funding for each country in Central Asia. In Kazakhstan, the IsDB has supported 69 projects with a total funding of 1,700 million USD, while in Kyrgyzstan, 71 projects have received 421 million USD in funding. Tajikistan has benefited from 92 projects with 663 million USD, and Uzbekistan has received funding for 123 projects, totaling 2,800 million USD. Turkmenistan has also received IsDB support for 23 projects, amounting to 1,300 million USD.

Fig 1: IsDB Funded Central Asian Projects

Republic of Kazakhstan

Kazakhstan has been making significant efforts to embrace Islamic Finance, becoming a regional hub for it in the Commonwealth of Independent States (CIS). The country started taking steps in this direction as far back as the early 1990s. These efforts were driven by the stability of Islamic financial institutions during the global financial crisis, the need to diversify funding sources, and attract long-term external investments for industrial development plans.

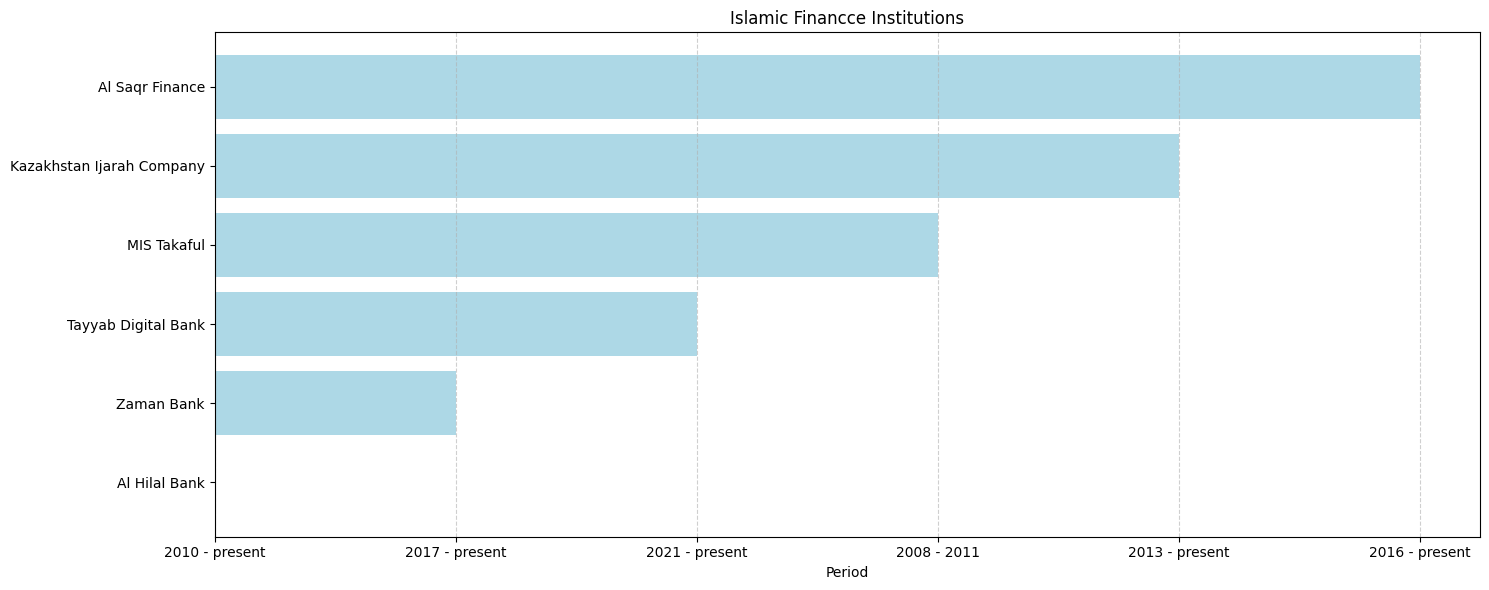

Since 2009, Kazakhstan has introduced various initiatives to support Islamic Finance, such as changes in legislation to promote Islamic banking and insurance (Takaful), the establishment of Islamic financial institutions (IFIs), and the issuance of Sukuk (Islamic bonds). Islamic banking in Kazakhstan accounts for a substantial portion of Central Asia's Islamic banking assets, and the country is expected to further boost its Islamic banking sector thanks to digitalization and government support. Currently, three Islamic banks and two Islamic leasing companies operate in the market. The details of Islamic financial institution are shown in figure 2. According to Islamic Financial Services Stability Report 2022 (IFSB, 2022), the Islamic banking sector in Kazakhstan accounts for 70 percent of Central Asia’s aggregate Islamic banking assets. Despite this, Islamic banking assets in the country represented less than one-quarter of one percent of all banking industry as of the end of 2021. Other Islamic financial institutions (OIFIs), such as fintech companies, investment firms, financing companies, leasing and microfinance firms, and brokers and traders, assets growth rate 44% was recorded.

Fig 2: Islamic finance Institutions in Kazakhstan

Key milestones in the development of Islamic Finance in Kazakhstan include the enactment of a special banking law in 2009 and the establishment of the first Islamic bank in 2010 through an intergovernmental agreement between the UAE and Kazakhstan. Several other IFIs and Islamic leasing companies now operate in the market. Kazakhstan aims to continue expanding its Islamic Finance sector with a new master plan for 2020-2025, which includes goals to increase the domestic market share of Islamic Finance. Various educational and research centers have also emerged to promote Islamic Finance education in the country.

In terms of regulations, Kazakhstan has made amendments to its legislation to facilitate Islamic banking and insurance, enabling Islamic banks to operate effectively. Additionally, the Astana International Financial Centre (AIFC) was established as a platform for financial services and has been actively promoting Islamic Finance. Kazakhstan's commitment to Islamic Finance reflects its aspiration to diversify its financial system and attract international investments, making it a notable player in the Islamic Finance landscape.

Kyrgyz Republic

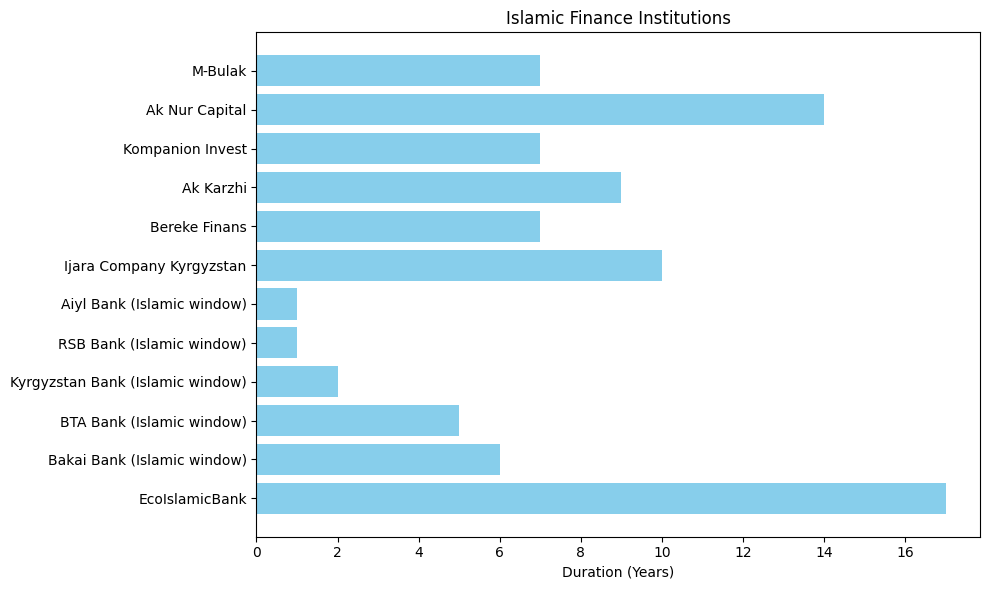

Kyrgyzstan has been a frontrunner in the adoption and development of Islamic finance in Central Asia since gaining independence. It has shown a higher level of commitment and consistency in this regard compared to its Central Asian and Transcaucasian counterparts. According to the Islamic Financial Services Stability Report 2022, the Kyrgyz Republic has made significant steps in creating a favorable environment for the smooth functioning of the Islamic financial system. Notable improvements have been made in the legal and regulatory frameworks, particularly in the areas of risk management and corporate governance, which have contributed to the growth of the Islamic banking industry.

As of now, Kyrgyzstan boasts one full-fledged Islamic bank, EcoIslamic Bank, along with four Islamic banking windows. Furthermore, five Islamic microfinance institutions offer Islamic financing, underpinning the country's commitment to expanding the reach of Islamic finance, the details are presents in figure 3. Takaful products are expected to enter the market in the near future, further diversifying the range of Islamic financial services available. By the end of 2021, the value of Islamic banking assets in Kyrgyzstan had increased by 28.78 percent year-on-year to approximately US$58.15 million. This represented a 1.5 percent share of the overall banking sector.

Fig 3: Islamic Finance Institutions in Kyrgyz Republic

A crucial aspect of the Islamic finance landscape in Kyrgyzstan is the legal and regulatory environment, which has been significantly improved to facilitate the functioning of the Islamic finance sector. Key milestones include introducing Islamic banking in 2006, creating Islamic banking windows within conventional banks, and amending various laws to accommodate Islamic finance. The National Bank of the Kyrgyz Republic (NBKR) has played a vital role in issuing resolutions and regulations to regulate and supervise Islamic financial transactions, risk management, and corporate governance.

However, despite the progress, Kyrgyzstan's Islamic finance sector faces challenges. These include a shortage of qualified Islamic finance specialists, low public awareness, a tightly regulated industry, and a lack of empirical research on the Islamic finance sector in the country. To further foster the growth of the Islamic finance industry in Kyrgyzstan, it is recommended to develop a long-term strategic plan with clear actions and milestones, establish capacity-building programs, liberalize the industry to encourage innovation, promote research and development, and increase public awareness and financial literacy. With these steps, Kyrgyzstan is well-positioned to continue its journey towards a more robust and diversified Islamic finance sector.

Republic of Tajikistan

Tajikistan's journey into Islamic finance and banking began in 1996 when the country became a member of the Islamic Development Bank (IsDB). Since then, Tajikistan has received around $500 million for the implementation of 60 projects, and the National Bank of Tajikistan (NBT) became an observer member of the Islamic Financial Services Board (IFSB) in 2010.

The government of Tajikistan initiated the introduction of Islamic banking in 2009, with the aim of promoting financial system resilience and stability through Islamic finance. They sought inspiration from countries like Kazakhstan, Kyrgyzstan, Malaysia, and Indonesia. The Islamic Banking Law was enacted in 2014, and over the subsequent years, the NBT developed more than 25 regulatory and legal frameworks to oversee and regulate Islamic financial institutions.

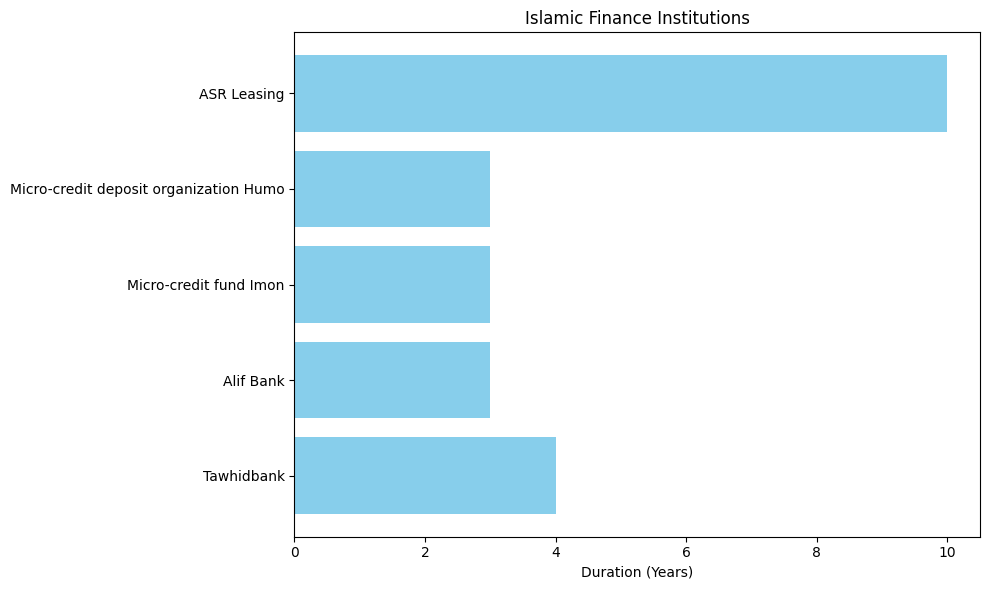

To facilitate the growth of Islamic banking in Tajikistan, the NBT established the Consultative Council for Islamic Banking Services in 2017. Key milestones in the development of the Islamic financial sector in Tajikistan include the establishment of the first Islamic leasing company, Asr Leasing, in 2013, the founding of the first regulated Islamic microfinance institution, Alif Capital, in 2014, and the establishment of a full-fledged Islamic bank, Tawhid bank, in 2019, as shown in figure 4. In Tajikistan, Islamic assets accounted for 1.1% of its all banking assets as of the end of 2021.

Fig 4: Islamic Finance Institutions in Tajikistan

As of mid-2022, Tajikistan's banking sector consists of 15 banks, including two state banks and two Islamic banks, with two Islamic banking windows also operating. Tawhid bank is the first full-fledged Islamic bank in Tajikistan, and Alif Bank offers digital Islamic banking services. Furthermore, microfinance institutions Imon and Humo have received licenses to open Islamic windows. In Central Asia where Tajikistan was one of the fastest growing Islamic banking markets, the introduction of takaful will shore up the region’s Shariah-compliant financial industry. Tawhid Bank, one of Tajikistan’s full-fledged Islamic banks, announced in February 2022 an agreement with AlHuda CIBE to set up a takaful operator.

The preconditions for the development of Islamic banking in Tajikistan include a significant Muslim population, challenges in the conventional banking system, a lack of alternative non-banking financing, the development of Islamic finance infrastructure, and the economic viability of Islamic banking. To further promote Islamic finance, recommendations include raising awareness, introducing Islamic finance education in schools, sharing knowledge with other countries, attracting international Islamic institutions, and standardizing products and operations. Educating the local population about Islamic finance is considered crucial for its success in Tajikistan.

Republic of Uzbekistan

Uzbekistan is developing its Islamic finance sector, which has the potential to serve its large and conservative Muslim population. The government has introduced various initiatives and laws, including the establishment of Islamic banking and finance infrastructure, the issuance of Sukuk, and the provision of Islamic financial services by microcredit institutions. Several banks are preparing to operate under Shariah principles and have signed cooperation agreements with the Islamic Corporation for the Development of the Private Sector (ICD) to open Islamic windows. Apex Insurance is the first and only Takaful operator in the country. Uzbekistan had 41 insurance companies operating as of September 2022, including 33 general and 8 life insurers. Taiba Leasing, established by the ICD in 2011, is the first standalone company in Uzbekistan offering Islamic financing products, focusing on leasing various types of equipment and machinery.

In April 2022, the President of Uzbekistan signed a law allowing microcredit institutions to provide Islamic financial services. The ICD and SQB Securities signed a Memorandum of Understanding in January 2021 to develop Islamic finance and capital markets in Uzbekistan, with a focus on introducing Sukuk and other Islamic finance instruments. The Uzbek government plans to launch the Tashkent International Financial Center, which will facilitate the development of the Islamic banking industry and introduce new instruments, such as Sukuk and Shari'ah-compliant swaps and repos. Islamic finance education is also on the rise in Uzbekistan, with academic institutions offering courses in the field.

A 2020 study by the UNDP found that 56% of individuals and 38% of businesses in Uzbekistan do not take loans due to religious beliefs. However, more than 60% of individuals and businesses do not have a full understanding of how Islamic finance products work. The Uzbekistan 2030 strategy is a positive step for Islamic banking, as it calls for the introduction of Islamic finance criteria and procedures in at least three commercial banks. This will make it easier for people in Uzbekistan to access Islamic finance products and services.

However, the development of Islamic finance faces challenges, including the need for an enabling legal and regulatory framework and the scarcity of skilled human capital. The government aims to address these issues and promote the growth of the Islamic finance industry by developing a strategic roadmap, adopting international prudential standards, and launching awareness campaigns. Furthermore, the introduction of Islamic FinTech and collaboration with international institutions are expected to facilitate Islamic financing in Uzbekistan.

Republic of Turkmenistan

Islamic finance is still in its early stages of development in Turkmenistan, with no Islamic banks or other financial institutions (IFIs) currently offering Shari’ah-compliant financing to the local population, despite demand. Government support is essential for encouraging the development of Islamic finance initiatives in the economy. Recently, the International Islamic Trade Finance Corporation (ITFC), a member of the Islamic Development Bank (IsDB) Group, partnered with the State Bank for Foreign Economic Affairs of Turkmenistan (SBFEAT) to organize a three-day Islamic trade finance workshop for local financial institutions and relevant public enterprises. The workshop covered a variety of Islamic financial products and services, with the aim of developing a thriving Islamic finance sector in Turkmenistan and increasing international trade. One positive sign for the development of Islamic finance in Turkmenistan is the interest shown by some local financial institutions and relevant public agencies at the ITFC's Islamic trade finance workshop.

- 05:00 am

iDenfy, a Lithuania-based RegTech company providing identity verification and fraud prevention tools, announced a new partnership with Opal Auctions, a global stone and jewelry marketplace platform for verified users. iDenfy’s KYC solution will help verify and onboard sellers and buyers through a simple, four-step identity verification process.

Without implementing a risk-based approach within the precious stone and jewelry industry, companies can face significant challenges in meeting Know Your Customer (KYC) and Anti-Money Laundering (AML) requirements. According to iDenfy, implementing proper fraud prevention processes and choosing the right tools is extremely important, especially since items like precious metals, stones, and jewelry are not only inherently high in value but also easily transportable. This makes the market that Opal Auctions operates in prone to money laundering and other financial crimes.

According to iDenfy, opals and jewelry have long been favored in international illicit financial activities. These criminal activities not only have financial consequences but can also tarnish a company's reputation and credibility. Opal Auctions operates in a global market, making it a prime target for cross-border schemes. In line with this perspective, Opal Auctions is committed to eliminating fraud risks and implementing a real-time anti-fraud strategy. To achieve this, the leading luxury opal auction platform decided to partner with iDenfy. With this partnership, the opal marketplace will enhance its risk reduction and mitigation strategy by implementing a crucial measure — identity verification.

Opal Auctions is a venue for members to offer, sell, or buy items. The company ensures trust through its established Verified Sellers program. All sellers on the platform must comply with this well-established program, which helps guarantee a high level of industry expertise, fair refund policies, and transparent pricing. Currently, Opal Auctions has a network of over 140 accredited opal sellers from more than two dozen countries. All verified sellers on the platform have special access to the industry's latest Opal Encyclopedia for up-to-date information. Furthermore, Opal Auctions stays updated with the latest gemological data for its stones. Its in-house professionals provide independent assessments to ensure item accuracy from pictures and descriptions.

The Opal Auctions team decided to switch from manual KYC processes and adapt to the changing technological scenery by implementing iDenfy’s full-stack ID verification software. After evaluating various KYC solutions, the business selected iDenfy as the top choice for identity verification. They were delighted by iDenfy's commitment to robust fraud prevention, safety, and user-friendly experience, matching the company's ID verification provider criteria.

Additionally, iDenfy asserts that this partnership will enhance Opal Auction’s efficiency. By centralizing data and introducing automated case assignment policies, the auction site will achieve a simple distribution of all KYC verifications while ensuring a transparent audit trail. This will enable Opal Auctions to easily monitor all user actions across their lifecycle, which is a crucial component in meeting compliance requirements. Through this partnership, the company will also have an option to customize the user interface to align with its brand.

Consequently, Opal Auctions will verify its sellers using advanced image recognition and face comparison algorithms. This updated verification process for Opal Auctions will provide real-time results, minimize fraud rates, and streamline the KYC process. It’s worth mentioning that iDenfy’s ID verification solution automatically recognizes, verifies, and extracts data from over 3,000 identity documents spanning 190+ countries. It covers a wide range of documents, including passports, ID cards, driver's licenses, and residence permits, enabling efficient and precise global identity document analysis for Opal Auctions.

“We’re happy to partner with Opal Auctions and help them onboard more users, at the same time, ensure trust for both buyers and sellers,” commented Domantas Ciulde, the CEO of iDenfy. “Our identity verification software is designed to foster trusted relationships in marketplaces while minimizing unnecessary friction in the process.”

- 04:00 am

After recently launching Tap to Pay on iPhone in the UK and Netherlands, myPOS has enabled Tap to Pay on iPhone for businesses in France.

“Nowadays, consumers expect the convenience of using contactless cards and digital wallets to make secure purchases wherever they shop. Tap to Pay on iPhone with the myPOS Glass app will help SMEs meet these consumer demands. Overall, contactless payment acceptance technology means better customer service, flexibility and mobility for the business owner,” said Florian Malvicino, myPOS France Country Manager.

Tap to Pay is available within the myPOS Glass iOS app and allows merchants to accept contactless payments directly on their iPhone, with no additional hardware. myPOS clients with compatible phones – iPhone XS or later running the latest version of iOS – can accept contactless payments by downloading and opening the myPOS Glass app, ringing up the sale and presenting their iPhone to the customer. In return, the shopper needs only to tap a contactless payment method like a contactless debit or credit card, Apple Pay, or another digital wallet.

French entrepreneurs seem to be looking forward to the new payment option. Andrea Tribolo is an osteopath based in Aix-en-Provence. She chose Tap to Pay on iPhone with myPOS to make it easier for her patients to pay. "Tap to Pay on iPhone allows my patients to pay for their consultation in a single gesture, by tapping their contactless card on my iPhone. This allows me to always have a way to accept credit card payments for home consultations. I highly recommend this feature to all healthcare professionals who want to simplify their payment acceptance."

Frederic Delaunay is a VTC driver in the Nantes region. Tap to Pay on iPhone with myPOS was an obvious choice for him when it came to equipping himself with a payment solution to accept customer contactless cards. "Tap to Pay saves me and my customers time when I drop them off at their appointments. They're often in a hurry and this innovation enables them to pay for their errand in a single gesture. All they have to do is hold their bank card or digital wallet up to my iPhone, and the payment is made! I recommend this feature to all my VTC and cab colleagues who want to save time, because in our profession, every minute counts!

Merchants new to the myPOS platform can start using Tap to Pay on iPhone with myPOS Glass after opening a myPOS account and going through online verification. What’s more, by becoming a myPOS client, they will benefit from a free merchant account, a free business card and immediate deposits of all accepted payments at no extra cost.

Apple’s Tap to Pay on iPhone technology uses the built-in features of iPhone to keep the businesses’ and customers’ data private and secure. When a payment is processed, Apple and the myPOS app do not store card numbers on the device or on Apple servers.