US Fed – “Here We Come, Ready to Taper”, Bond Yields Soar

- Michael Moran , Senior Currency Strategist at ACY Securities

- 17.06.2021 12:00 pm trading

Hawkish Surprise Boosts USD; Majors, EMS, Asians Slump

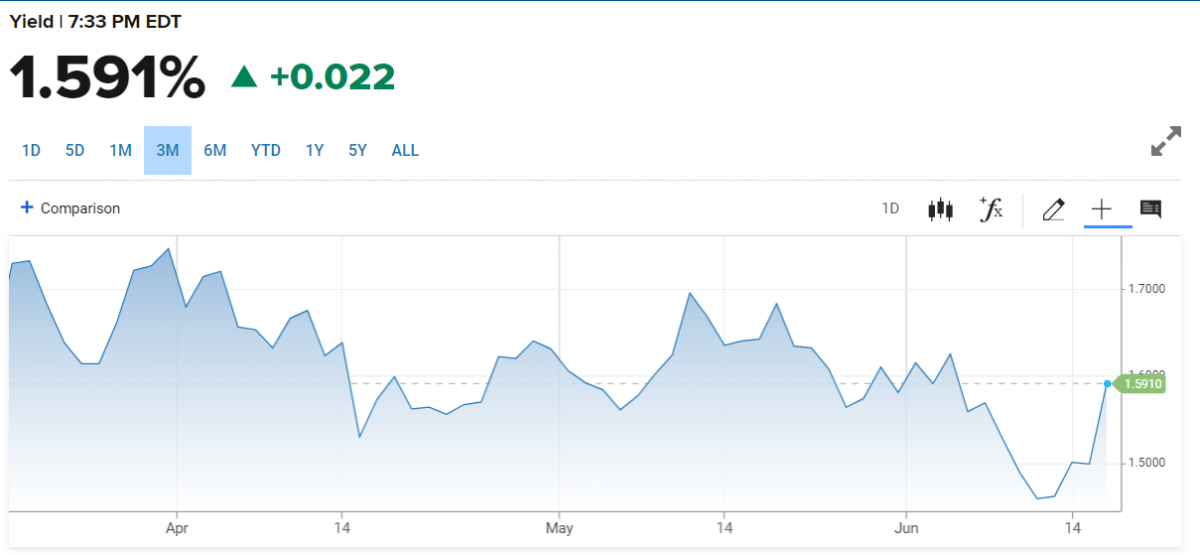

Summary: While the Federal Reserve kept its Fed Funds rate unchanged (0-0.25%) and maintained its monthly QE taper, projections pointed to a clear hawkish shift. The dot plot (a quarterly chart summarizing the outlook for the Fed Funds rate over the next 3 years) saw officials increasing rates at least twice in 2023. In his speech following the FOMC decision, Fed Chair Jerome Powell remarked “inflation has increased notably in recent months.” The Fed’s Q4 year-on-year GDP forecast for 2021 was revised higher to 7% from 6.5%. The benchmark US 10-year bond yield soaring to 1.579% at the close of trading, up 9 basis points (1.49%). Two-year US Treasuries climbed to 0.20% from 0.16%. Short speculative US Dollar bets (long Currencies) raced for the exits which resulted in a 0.8% lift in the Dollar Index (USD/DXY) to 91.25 from 90.50 yesterday. The Euro slumped from its 1.2125 open yesterday to close at 1.2006, just above the critical 1.20 level, and a loss of 0.96%. Sterling was last at 1.3997 (1.4080) with Brexit jitters adding weight to the British currency. The Australian Dollar fell further from its 0.7685 open to close at a 2-month low at 0.7615. USD/JPY extended it rally to finish at 110.65 (110.05). Against the Canadian Loonie, the Greenback climbed 0.62% to 1.2265 (1.2188). The Greenback gained most versus the Asian and Emerging Market currencies. USD/CNH (Dollar-Offshore Chinese Yuan) rocketed to 6.4385 at the New York close (6.4065 yesterday) and 6.3870 last Friday. The USD/SGD pair gained 0.65% to 1.3358 (1.3275). Wall Street stocks fell after the Fed boosted its outlook. The DOW lost 0.75% to 34,037 (34,300) while the S&P 500 slipped to 4,224 (4,247). Other global bond yields were steady. German’s 10-year Bund yield eased 2 basis points to -0.25% while the UK’s 10-year Gilt rate was last at 0.74% from 0.76%.

Data released yesterday saw Japan’s April Machinery Orders slump to 0.6% from 3.7% in March, underwhelming estimates at 2.7%. UK Headline CPI (y/y) rose to 2.1% in May from 1.5% in April and beating forecasts at 1.8%. China’s Industrial Production (y/y) fell to 8.8% in May from 9.8% in April, missing estimates at 9.2%. Chinese May Retail Sales (y/y) was also lower to 12.4% (17.7% April) and lower than expectations of 14.0%. The Unemployment rate in China improved in May to 5% from 5.1% previously. Canada’s May Headline CPI (m/m) rose to 0.5%, beating forecasts at 0.4%. US May Building Permits eased to 1.68 million from a downwardly revised 1.73 million in April. Housing Starts in the US were also lower than estimates at 1.57 million against 1.64 million.

- EUR/USD – Euro long bets were shaken out following the hawkish bent from the US Federal Reserve. The EUR/USD pair slumped from its 1.2126 opening (which was mid-range earlier in the week) to an overnight low at 1.20036 before stabilising to settle at 1.2006 at the New York close. In early Sydney, the shared currency eased further to 1.1995.

- AUD/USD – The Aussie Battler slid to 0.76085 post FOMC before climbing to 0.7615 at the New York close. In early Sydney, AUD/USD trades at 0.7620 with the 0.7600 support level holding so far. Today sees Australia’s May Employment report as well as a speech from RBA Governor Philip Lowe.

- USD/JPY – Higher US bond yields following the FOMC Statement saw the Greenback extend its rally against the Yen to 110.723 in early Sydney. USD/JPY closed at 110.65 in New York, up 0.51% from 110.05 yesterday. Japanese economic data released saw a slump in Japan’s April Machinery Orders.

- USD/CNH – The Fed’s hawkish shift coupled with weaker-than-expected Chinese Industrial Production and Retail Sales (May) saw the USD/CNH soar to an overnight high at 6.4427 (6.4065 open yesterday). The Dollar eased back to settle at 6.4385 in late New York. Two weeks ago, the Greenback was languishing against the Offshore Chinese Yuan at 6.3517.

On the Lookout: A few minutes ago, New Zealand’s Q1 GDP (q/q) soared 1.6% overwhelming median forecasts for a 0.5% rise and the previous quarter’s fall of -1.0%. NZD/USD rose 10 pips to 0.7067 from the New York close of 0.7057, and yesterday’s 0.7122 open. The muted reaction to the upbeat GDP report was mainly due to the overall stronger Greenback. Expect this newfound USD strength to pervade FX trading today.

The economic calendar sees China’s May House Price Index kick off (April’s was 4.8%). Australia releases its May Employment Report which will be keenly watched (11.30 am Sydney). The Australian economy is forecast to have added 30,500 jobs in May following April’s fall of -30,600 jobs. Australia’s Unemployment Rate is forecast to remain unchanged at 5.5%. Earlier in the day (10.10 am Sydney) RBA Governor Philip Lowe is due to deliver a speech to the Australian Farm Institute Conference in Queensland titled “From Recovery to Expansion”. Interesting timing, considering this will come just ahead of the Aussie Jobs report. Europe enters the market with Switzerland’s May Trade Balance (f/c +CHF 4.23 billion from 3.84 billion). The Swiss National Bank has its Monetary Policy Assessment and Policy Rate (f/c unchanged at -0.75%) followed by a Press Conference. The Eurozone releases its Final Headline (y/y f/c 2.0% from 2.0%) and Core CPI (y/y f/c 0.9% from 0.9%). Canada reports on its ADP Non-Farm Employment Changed (May, no forecasts, April’s was 351.3k). Finally, the US releases its Weekly Unemployment Claims (f/c 359k from 376k – Finlogix). US Philly Fed Manufacturing Index for June follows (f/c 31.0 from 31.5) and US CB Leading Index for May (m/m f/c 1.3% from 1.6%).

Trading Perspective: The Dollar has gained the upper edge against its Rivals following the Fed’s changes in its forecasts. But as we all know in any market, FX specifically, nothing goes in a straight line forever. Expect consolidation within the recent ranges and an overall bid US Dollar. Watch the US bond yields in the days ahead. The benchmark 10-year bond yield peaked at 1.7540 at the end of March, closing at 1.579% yesterday. Keep an eye out ahead for the other major central banks and their respective outlooks to their easy money policies. The next major central bank to meet (next week) is the Bank of England.

- EUR/USD – The Euro broke through the 1.2000 support level in early Asia this morning and currently trades at 1.1990. Immediate support lies at the 1.1970/80 level, which is strong and should hold for now. Immediate resistance can be found at 1.2030 and 1.2060. Expect consolidation between 1.1970 and 1.2030 first up. The risk is still lower for the Euro but be patient to sell rallies.

- AUD/USD – The Battler extended its losses this morning, breaking through the overnight low at 0.7609 to 0.7604 before settling at its current 0.7612 level. Immediate support at 0.7600 is strong and should hold into Australia’s Employment report. Any weakness in the job market could see a break down through the next support level at 0.7575. Immediate resistance can be found at 0.7650 followed by 0.7680 and 0.7700. While the Aussie looks heavy, prefer to sell rallies. For now, am prepared to trade the range between 0.7585-0.7655.

- USD/JPY – the Dollar has edged up against the Japanese Yen to its current 110.79 level from the New York close at 110.65. It is surprising that this currency pair did not trade higher given the move up in the US 10-year bond yield. Japan’s 10-year JGB yield was unchanged at 0.04%. We can expect a drift up to the next resistance level at 111.00, which is strong. The next resistance level comes in at 111.40. Immediate support can be found at 110.30 and 109.90. Look for a likely trade between 110.35-85 first up.

- GBP/USD – Sterling looks suspect and the close below 1.4000 doesn’t auger well for the Pound. GBP/USD currently trades at 1.3985 (1.3997 NY close) with the next support level found at 1.3960 and 1.3930. Immediate resistance can be found at 1.4040 and 1.4090. Look for consolidation between 1.3970 and 1.4070 first up. Be patient and wait to sell into strength for the next leg lower.

Happy Thursday and trading all.