Alternative Lending: the Key to Financial Inclusion

- Vit Arnautov, Chief Product Officer at TurnKey Lender

- 27.03.2019 07:45 am alternative finance , Lending , Vit Arnautov is the Chief Product Officer at TurnKey Lender, a company creating intelligent AI-driven solutions for alternative lenders. With more than 10 years of experience in IT, Vit is happy to share his expertise with striving entrepreneurs and anyone else it can be helpful for.

Credit scores and history, checks of bank accounts, bleak and lengthy application processes and waiting for approval - these are the things most people associate lending with. And the reason for it is that most lending is still done through outdated workflows and interfaces of old-school banks. They do their best to optimize, but being as huge, bureaucratic and reliant on legacy solutions as they are, it’s hard to be agile and fast on your feet when it comes to automation and restructuring.

The systems still run on old algorithms, they often rely on humans to analyze the applications and process them and what’s even worse, they still do many of the tasks on real paper. You heard me right. Not digitally, but on real paper, with real pens. That’s crazy considering the state of technology we live in right now and the speed at which it develops.

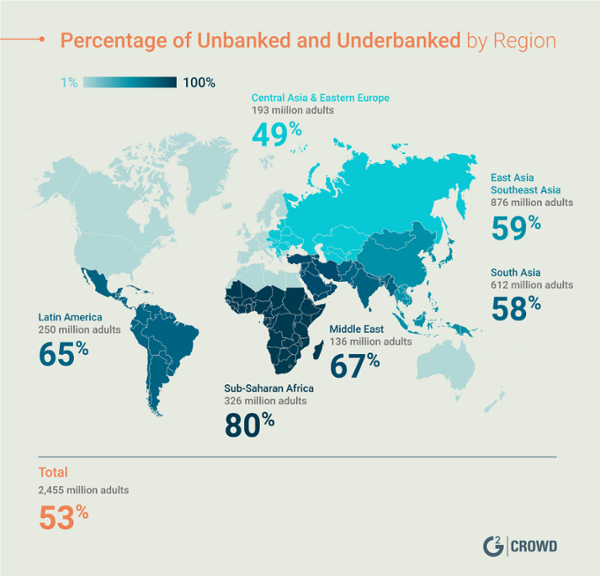

All that leads to more complex processes, higher rejection rates, long waiting periods, and still 2.5 billions of people being in need of proper lending products and services. All that sounds depressing. So let me ease your mind a bit because where there’s demand, there’s supply. And the demand for change in the lending niche is very clear. That’s where alternative lenders come into play.

(G2Crowd)

Their processes are automated to the maximum possible extent, their staffs are small, they don’t need branches around the country, etc. All that adds up to easier and faster processes, access to new, previously underserved, audiences, smarted decisioning, better experience and oftentimes better rates.

Easier access to products and services

Any way you look at it, alternative lending makes credit products more accessible to the public. And with each new lending operation popping up, competition grows. And where competition grows, interest rates drop and software becomes more intuitive and easy to use.

Digitalization of lending isn’t some shade of tomorrow we have to look forward to. It’s already here. And the lenders who embrace it will come out on top. Just as well as the borrowers who choose the right alternative loan providers. Automation makes everyone’s life easier in lending. Lender’s save money and time originating, servicing and collecting and borrowers get better services and products at better prices.

The barrier into entering the lending niche got really low ever since FinTech companies like TurnKey Lender started to provide lenders with ready-to-use platforms to automate lending. And while starting a business got easier, the fight for the users got a little more fierce due to competition. So lenders are forced to reach out into serving previously unbanked and underbanked.

These people weren’t server before because of low credit scores and high risks, but due to the advanced evaluation algorithms and AI powering those algorithms, lenders now can approve more of the safe loans faster. This leads not only to global financial inclusion but also to lenders getting healthier portfolios despite working with people who were considered unreliable before.

Alternative to traditional and shady providers

Before the rise of alternative and digital lending, underbanked and unbanked had to get money from pawnshops and semi-legal shady operations. Now, just with access to a smartphone, they can get a loan from a reputable institution properly regulated by local authorities.

New decisioning rules

Artificial and Big Data aren’t just buzzwords anymore. They are already being implemented in a meaningful way to help businesses grow and prosper. And in lending, the area that benefits from AI most is decisioning.

Loan origination used to take weeks for traditional lenders. It takes a lot of time and analysis for them to come to the conclusion that someone deserves a loan. And with their bureaucratic procedures and criteria, just 26% of small business loans get approved. With AI, like that of TurnKey Lender, loan origination can’t just be reduced to 9 minutes but also lets lenders approve more of the right loans.

The loans that would be declined were for the people who don’t have a proper credit history. But in reality, they very well may be are good people who need money for legit purposes and would pay back the loans in time. The self-learning algorithms adjust to the specific clientele of business and take into account a bunch of unconventional behavioral and informational factors to ensure that both lenders stay safe and borrowers funded.

Price of credit

Alternative digital lenders generally don’t create their own software from scratch. The wave of automation is here for lending and it makes running a lending business drastically easier, not to mention cheaper.

In addition to reducing operational costs, the right lending automation software significantly reduces risks of issuing wrong loans, helps minimize human error and overall, takes lending to a much safer and faster place. This and increased competition, lets credit providers distribute loans at better prices and still work at a profit.

Peer-to-Peer trend

One of the big trends in alternative lending is peer-to-peer financing. With it, lending business needs even less investment to start working. And not just borrowers get what they need but also the people who want to invest their free funds at attractive return rates.

In the years to come, p2p will only continue to grow, letting more businesses and individuals get funded even if they weren’t eligible according to the traditional institutions. Peer-to-peer lending model is going to push the whole financial world to a more inclusive state of being without the monopolies of big banks.

Better user experience

Going to a bank’s branch, collecting a ton of papers, sitting in a line, and waiting for weeks to get rejected doesn’t sound like a great experience to me. Alternative lending changes that, making application, processing, and servicing processes automatically and relocating them online. It may sound a bit introverted, but, given a choice, I’ll take an online experience any day.

Traditional banks often get stuck with legacy solutions that look like they are a parody of a website from the nineties. Another good thing about alternative lenders and the fact that they use ready-made automation platforms is that the interfaces can be crispy-clean and built according to the latest design best practices. That’s true, of course, only if the lender has chosen the right lending automation solution.

Final thoughts

Despite the efforts of lending automation companies and alternative lenders, global financial inclusion is still a bit down the road. But the trend looks up and the wave of upgrading credit products and services looks up for all those underbanked and unbanked around the globe.