Published

- 01:00 am

TransUnion, a global information and insights company and one of the UK’s leading credit reference agencies, has released new data on e-commerce fraud trends in the UK during the early 2023 festive season.

Drawing on insights from TransUnion's global device risk consortium, the analysis reviews e-commerce transactions throughout the Cyber Five days, spanning from the Thursday before Black Friday, 23 November to Cyber Monday, 27 November 2023. For consumers located in the UK when transacting, the average number of suspected e-commerce fraud attempts on any given day during the 2023 Cyber Five days was 117% higher than the rest of the year.

“As many purchase gifts online for their friends and loved ones during the run-up to the festive break, there is an increased risk of fraudsters targeting vulnerable consumers for their financial gain,” said Kelli Fielding, chief product officer at TransUnion in the UK. “Online retailers must protect consumers seeking the best deals and financial organizations are using all the tools available to stop fraudsters where they can, by employing holistic fraud solutions that verify customer identity and authenticity at the beginning of transactions.”

The Percentage of Suspected E-Commerce Fraud during the Cyber Five vs. Overall

Country/ Region | Cyber Five 2023 (23 – 27 Nov.) | All 2023 before 23 Nov. | Cyber Five 2022 (24 – 28 Nov.) | All 2022 | Cyber Five 2021 (25 – 29 Nov.) | All 2021 |

UK | 1.52% | 1.09% | 0.66% | 0.88% | 0.63% | 0.70% |

The analysis revealed the average percentage of suspected digital fraud attempts on any given day around Black Friday. TransUnion found UK customers flagged 1.52% of e-commerce transactions as potentially fraudulent, peaking on Black Friday when the suspected digital fraud rate reached 1.76%.

“While the data suggests that there was an uptick in suspected fraudulent transactions – particularly about previous years – this may also be a result of stricter rules and lower risk appetite being applied by retailers during this period,” said Chad Reimers, general manager of fraud and ID at TransUnion in the UK. “Retailers may have reflected on past years’ activity and introduced elements of friction for transactions deemed riskier.”

The Suspected Digital Fraud Rate Varies for Each Day of the 2023 Holiday Shopping Weekend

Day | Transactions in the UK |

Thursday, 23 Nov. | 1.51% |

Friday, 24 Nov. | 1.76% |

Saturday, 25 Nov. | 1.54% |

Sunday, 26 Nov. | 1.27% |

Monday, 27 Nov. | 1.50% |

Consumer concern about being a victim of fraud

In parallel with the rise of suspected digital fraud, consumers are expressing growing concern about potential victimization during the traditional peak period of seasonal shopping. TransUnion’s Q4 2023 Consumer Pulse study found that most UK consumers (59%) are extremely, very, or moderately concerned with falling victim to online fraud this festive season – an increase from 52% in 2022.

“The winter holidays signify the peak shopping season for retailers, but minimizing digital fraud should remain a priority year-round as we see an acceleration to digital channels continue,” Chad Reimers added. “Retailers need to be proactive when it comes to fraud prevention, by arming themselves with the appropriate tools to protect consumers, while offering them a seamless shopping experience in the most friction-right way possible. We are seeing practical examples of this through the multi-layering of risk decisioning strategies during consumer onboarding, leveraging multiple identity, digital, and device signals.”

TransUnion reached its conclusions based on intelligence from its identity and fraud product suite, TruValidate™. The rate of suspected digital fraud attempts reflects interactions that TransUnion customers either denied in real time due to fraud indicators or identified as fraudulent after manual review, compared to all assessed transactions.

- 05:00 am

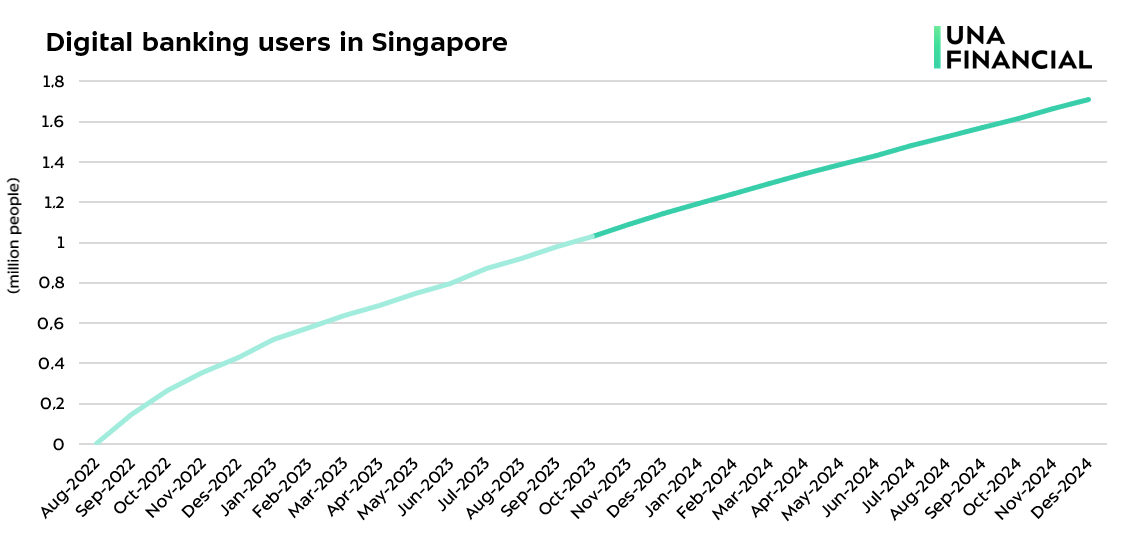

Digital banks in Singapore are experiencing consistent growth, which can be evaluated through a number of indicators including the net interest income and number of users.

Since 2017, the net interest income of digital banks grew by an average of 60% annually. The largest increase of 0.7 billion euros took place in 2022, due to the launch of digital banks in the country. In 2023, the net interest income of digital banks equaled 2.7 billion euros. According to UnaFinancial’s estimates, it is expected to grow by 1.2 times by the end of 2024, reaching 3.3 billion euros.

The app download statistics are available from August 2022. In October 2023, the number of digital banking users reached one million people. The average monthly growth rate was 76%. UnaFinancial’s forecast shows that by 2025, the number of digital banking users will reach 1.7 million.

Analysts of the group comment: “The growth drivers for digital banks in Singapore include two main factors. First, there is an increasing demand for alternatives to traditional banks. Secondly, Singapore is characterized with a high degree of digitalization. The country ranks fourth in the Global Digital Competitiveness Ranking 2022.”

Apart from the historical changes, the study took into account influencing factors. For instance, the number of digital banking users is impacted by such factors as the level of smartphone penetration (direct correlation with the coefficient of 0.98), share of social media users among the population (direct correlation with the coefficient of 0.98) and the inflation rate (inverse correlation with the coefficient of 0.92).

The net interest income of digital banks is influenced by a number of factors, including the GDP per capita (direct correlation with the coefficient 0.73), Internet penetration direct correlation with the coefficient of 0.81) and the inflation rate (direct correlation with the coefficient of 0.84).

- 09:00 am

Thredd, the leading next-gen issuer payments platform, announced that 2023 will deliver the best performance in the company’s history. With strong support from investors including Advent International, Viking Capital, Temasek, and Mission OG, Thredd expanded its leadership role in the payment ecosystem, driving client-centric expansion across global markets with sights set on leveraging this momentum for future growth.

During 2023, Thredd expanded its existing customer base, increasing its transaction growth across several regions. In a difficult year for the fintech industry, Thredd’s organic growth from existing customers in Europe and Asia Pacific increased by 20%, and new client sales tripled. Thredd also expanded its geographic footprint, signing several clients, including Cape, Paytron, BigPay, and others in Malaysia, Thailand, Philippines, Hong Kong, and Australia.

“Thredd’s 2023 performance confirms our belief that this organization could take modern issuing processing well beyond its original remit,” said Gene Lockhart, Thredd's board chairman. “Working hand in hand with Thredd’s investors, the entire Thredd organisation has come together to deliver a clear strategy and plan for sustained expansion. We are all very proud of the team’s achievements.”

Thredd experienced exponential growth across various industries, with a record-breaking 150% increase in new sales. These areas include digital banking, B2B payments, B2C payments, and numerous program types, including cross-border, travel, financial inclusion, multi-currency, and digital wallets. In addition to supporting key payments functionality, Thredd’s client service focus and resulting industry-leading customer satisfaction performance, have also been a key success driver in 2023.

With an emphasis on driving growth and sales across global markets, new payment executives joined Thredd to execute its vision for seamless global payment experiences. Formerly GPS, Thredd was rebranded with a customer-centered positioning that leverages the experience of industry veterans, including Jim McCarthy, the company's new CEO, and Ava Kelly, its newly appointed CPO. Thredd’s recent rebrand also renewed the company’s focus on securing the support of ecosystem partnerships such as Visa, Mastercard, BIN sponsors, consultants, and program managers.

“Joining Thredd in early 2023, I immediately saw the potential of a company on the verge of its next major growth phase,” said Jim McCarthy, Thredd CEO. “Leveraging both new and existing talent within the business, we have put our vision into action with meaningful results for our clients, partners, and team. We have a clear vision and track record of success that we plan to build on in 2024, including entering the US and expanding our network partnerships.”

“As we look toward 2024, there is no question that we will see increased demand for innovation, technological efficiencies, and improved customer experience across the payments industry,” said Ava Kelly, Thredd's Chief Product Officer. “Our goal at Thredd is to transform buzzwords, such as embedded finance, generative AI, and others, into tangible deliverables for our clients. We are a company built on successful partnerships, and our roadmap will be delivered with that touchstone as our guide.”

Thredd has main offices in London, Singapore, and Sydney, with teams in other key markets including, Hong Kong, India, and the US.

- 01:00 am

Virgin Money has announced the launch of a new pension offering, enhancing its digital platform and further extending its partnership with FNZ.

The innovative digital investment solution was initially launched in April 2023, and aimed to make investments more accessible, straightforward and transparent for UK retail investors.

The direct-to-consumer (D2C) platform provides both first-time and experienced investors with direct access to a range of investment funds to choose from, within an ISA or GIA. Everything is managed online and via a dedicated app, ensuring a seamless digital experience, all underpinned by FNZ’s market-leading technology.

The latest pension enhancement now introduces two distinct options – Navigator and Self Drive –helping customers take control of their future and grow their money for a brighter retirement.

The pension has been designed with simplicity in mind to give customers the confidence to make good decisions when it comes to managing their money.

Virgin Money is also helping customers combine existing pensions into one. In just a few simple steps, customers can transfer existing pensions into their Virgin Money pension, meaning they can gain a much clearer view of what their overall retirement income could look like and manage this all-in-one place.

Jonathan Byrne, Chief Executive Officer at Virgin Money Investments, said: “We’re delighted to have launched a new pension proposition - giving customers the confidence to plan for a brighter retirement and feel in control of their money. Planning for the future should feel straightforward. That's why we’ve designed our new pension to simplify the path to financial security.”

After a comprehensive selection process, Virgin Money selected FNZ as its partner. This was due to their state-of-the-art technology. Proven excellence in delivering market-leading direct-to-consumer propositions. A track record of complex platform implementations. And their ability to deliver innovative end-to-end digital experiences across multiple channels.

Alastair Conway, FNZ Chief Executive Officer, UK, Middle East and Africa, added: “We’re thrilled to have partnered with Virgin Money on the launch of the new pension offering. Our partnership reflects our joint commitment to transforming the landscape of wealth management, helping everyone, everywhere invest in their future on their own terms.”

- 04:00 am

Worldline, a global leader in payments services, has launched the Worldline Food Services Payments Suite, an end-to-end solution offering an enhanced, seamless, and secure payment experience for the food and beverage industry, particularly for quick service restaurants and their guests.

With the global foodservice market projected to almost double from US$ 2’65 trillion in 2023 to $ 5.42 trillion by 2030 the industry, particularly within the European restaurant sector, is undergoing a pivotal transformation, driven by innovation and technology. This evolution is not only about enhancing the dining experience but also about streamlining operational efficiency and adapting to the changing preferences of consumers. For example, according to Deloitte, 60% of consumers believe that technology improves their dining experience by streamlining operations and reducing wait times.

Such statistics including the fact that there has been a 65% growth in online food orders and a 31% increase in takeaway service since the pandemic, are transforming restaurants from traditional eating spaces into technologically advanced environments where payment technologies are integrated into the customer experience. This has led to the creation of comprehensive, immersive experiences that bridge physical and digital, including not only augmented-reality menus and AI-driven meal recommendations but also a seamless integration of the dining experience with digital platforms, all the way through to an almost unnoticeable act of payment.

Worldline Food Services Payments Suite has been developed specifically to:

- Answer our customers' food and beverage use cases beyond traditional payment processing. For example, it encapsulates developments and trends within the industry by facilitating the latest digital solutions like wallets, QR codes, and in-app payments.

- Emphasize the customer engagement experience, particularly at the point of checkout. This new and innovative solution creates a more memorable and satisfying experience where the use of data-driven analytics, often powered by AI, plays a pivotal role.

- Enable extended connectivity into the food services ecosystem by using customer data. This offering integrates closely with the hardware and maintenance partners, to offer more targeted and appropriate services and nurture a more loyal customer base.

Florian Cottereau, Global Head of Sales for Retail and Food & Beverage, Merchant Services at Worldline, explains: “Worldline is a major payment service partner of main international brands of Quick Service Restaurants in Europe and the UK, such as Subway SSP, or Areas. With our Food Services Payments Suite, we aim to reinforce our footprint with local restaurant chains and F&B platforms. Food Services Payments is designed to offer a streamlined, secure, and efficient end-to-end payment solution that covers both in-restaurant and online payments. Furthermore, our unique “A la Carte Acquiring” approach enables merchants and partners to find the solution that best fits their needs.”

- 08:00 am

The Consumer Financial Protection Bureau (CFPB) today issued a new report finding that many consumers are still being hit with unexpected overdraft and nonsufficient fund (NSF) fees, despite recent changes implemented by banks and credit unions that have eliminated billions of dollars in fees charged each year. In a recent CFPB Making Ends Meet survey, more than a quarter of consumers responded that someone in their household was charged an overdraft fee or NSF fee within the past year, and that only 22% of households expected their most recent overdraft. Many consumers who were charged overdraft fees had access to a cheaper alternative, such as available credit on a credit card.

“Our research finds that American families are paying fees they do not expect, even when they have access to cheaper forms of credit,” said CFPB Director Rohit Chopra.

The report, Overdraft and Nonsufficient Fund Fees, explores consumers’ experiences with overdraft and NSF fees. Many consumers have access to cheaper credit sources, such as on a credit card, and report being surprised by their most recent overdraft. Other consumers appear to use overdrafts often and intentionally: in households charged more than 10 such fees in a year, more than half of respondents reported that they expected their most recent overdraft. Most account overdrafts are exempt from the regulation implementing the Truth in Lending Act, which is designed to promote the informed use of credit and make it easier for consumers to compare the cost of credit products.

Key findings from surveyed households and consumers in today’s report include:

- Households frequently incurring overdraft and NSF fees are more likely to struggle to meet their financial obligations: Among households that frequently incurred overdraft/NSF fees, 81% reported difficulty paying a bill at least once in the past year. This drops to 25% for households that were not charged a fee.

- Many consumers do not expect overdraft fees: Among consumers in households charged an overdraft fee in the past year, 43% were surprised by their most recent account overdraft, 35% thought it was possible, and only 22% expected it. Consumers who overdraft infrequently are more likely to be surprised by a fee: 15% of consumers from households charged 1 to 3 overdraft fees expected their most recent transaction to overdraft; among households charged more than 10 overdraft fees, 56% expected their most recent overdraft.

- Most households incurring overdraft fees had available credit on a credit card: Among households charged 1-3 overdraft fees in the past year, 68% had credit available on a credit card, while 62% of households charged 3-10 overdraft fees had credit available on a credit card. In households charged more than 10 fees in the past year, 51% still had credit available on a credit card.

- Households face a substantial overlap in being charged overdraft and NSF fees: Among consumers in households charged an NSF fee in the past year, 85% were also charged an overdraft fee. Among consumers in households charged an overdraft fee in the past year, 72% were also charged an NSF fee.

- Low-income households are hit the hardest Overdraft and NSF fees: While just 10% of households with over $175,000 in income were charged an overdraft or an NSF fee in the previous year, the share is three times higher (34%) among households making less than $65,000.

The data for the report comes from the 2023 Making Ends Meet survey and the CFPB’s Consumer Credit Panel. The survey asks consumers about their experiences with overdraft and NSF fees in the past year, as well as their experiences applying for and obtaining credit, use of alternative financial services (e.g., payday or auto title loans), and financial pressures (e.g., difficulty paying bills or carrying an unpaid balance on a credit card). The Consumer Credit Panel, a deidentified sample of credit records maintained by one of the three nationwide consumer reporting agencies, allows the CFPB to observe the credit and debt profiles of these same consumers, including their credit scores, amount of credit available, and delinquent debt.

- 07:00 am

Phoenix Investment House, the capital market, brokerage, and fund management arm of Phoenix Holdings, a leading Israel-based insurance, asset management, and financials group (“Phoenix”) has selected the Order Management System (OMS) of Global Fintech leader Broadridge to drive expansion of international institutional trading on the Tel Aviv Stock Exchange.

"We are proud to offer direct market access to the Tel Aviv Stock Exchange to our clients, fully managed and hosted by Broadridge in the London Data Center environment,” said Elad Burshtein, CEO of Phoenix’s Brokerage and Portfolio Management platform. “Broadridge’s solution significantly improves the toolkit available to international clients wishing to access the TASE. This strategic partnership is a sign of our commitment to innovation, client service and strategic value creation within Israeli capital markets. This initiative will facilitate greater access for international institutions to the Israeli capital market."

“With advanced trading tools and reliable technology, Broadridge’s fully hosted OMS will enable Phoenix to deepen its already distinctive institutional value proposition,” said Ofir Gefen, Managing Director EMEA and APAC, Broadridge Trading and Connectivity Solutions. “Israel is an important market for Broadridge in EMEA, and we are looking forward to a long-lasting relationship with Phoenix.”

Macroeconomic trends and the emphasis on operational resilience are leading firms to look for rich functionality and reduced costs of ownership of solutions. Broadridge’s OMS supports high- and low-touch workflows with powerful tools for compliance and a seamless integration to solutions across the trade lifecycle. The OMS is connected to over 200 exchanges with multi asset class capabilities and utilized by over 150 firms and five thousand active traders globally.

- 03:00 am

Hakbah, the leading Saudi-based fintech savings platform, announces its successful $5.1 million Series A fundraising.

The funding round was led by VentureSouq - the MENA-based venture capital firm with a global portfolio. Also participating were new investors M-Capital and Bunat Ventures; and existing investors Global Ventures and Aditum Investment Management Ltd.

Hakbah is one of MENA’s fastest-growing start-ups and operates in KSA’s $216 billion savings market. The Company has recorded an 18x increase in Total Savings Under Management and a 4x increase in revenue this year, struck several blue-chip partnerships with the likes of flynas, the national low-cost airline in Saudi Arabia and the Middle East has a customer base of over 500,000 users (of which 70% are between 21-35 years old).

Proceeds of the Series A funding round will be used for further product development, with a strong focus on Machine Learning and further developing the Company’s easily integrable savings engine. Capital will be ring-fenced to attract and nurture the region’s best talent and strengthen Hakbah’s position as the region’s leading savings platform. The Company also anticipates entering two regional markets shortly, either via a partnership or a strategic alliance.

Hakbah’s social savings platform - which strengthens financial inclusion and fully integrates with any banking system in less than a week - includes the digitization of traditional group savings (Jameya) with the purpose of spending on financial needs. Popular in over 60 countries worldwide, savings groups are a popular and traditional savings behavior. Hakbah’s users prioritize total needs over time and share the pool of money - which is rotated amongst them. This elevates traditional savings behavior, allows saving for purpose, and increases financial literacy. The Company also anticipates entering two regional markets shortly, either via a partnership or a strategic alliance.

Hakbah’s model tackles the Middle East savings crisis. Savings are a key strategic objective in ‘Saudi Vision 2030’ and critical to the country’s Financial Sector Development Program. 70% of Saudi citizens are without emergency savings, while the country’s household savings rate averages just 1.6%.

Naif AbuSaida, The Founder of Hakbah, said:

“We are grateful and happy to announce our Series A funding round and to enjoy the trust of both our new and existing investors. This demonstrates our success in delivering Hakbah’s strategic goals and will help accelerate our growth plans and financial stability for individuals.

“We’re working to build a savings platform via which individuals can save easily, quickly, collectively, and with impact - on our mission to double the individuals' savings ratio in Saudi Arabia by 2025. With the sizeable Savings Groups and Household Savings markets, and 60% of the population under 30, there is a significant opportunity for efficient, digital solutions to transform Saudi Arabia’s savings habits.

The support from esteemed organizations such as the Saudi Central Bank, Digital Government Authority, Monsha'at, National Technology Development Program, and Saudi Fintech is vital in our pursuit of growth and innovation. By leveraging machine learning and customer behaviors, we aim to develop cutting-edge savings products that cater to the unique needs of our customers."

Musaab Hakami, General Partner - Fintech, of VentureSouq, said:

“We are thrilled to lead this funding round in one of MENA’s most exciting start-ups and to work with Naif and his team in their mission to modernize financial savings and increase financial inclusion. Hakbah has a truly innovative product, a compelling market, and a track record of delivering on its growth promises. We look forward to supporting the Company’s continued scaling.”

- 03:00 am

The UK’s first travel debit card Currensea, has saved travellers over £3 million in foreign exchange (FX) fees since its launch in 2020.

The Currensea card saves at least 85% on every overseas transaction by cutting out the normal fees leveraged by banks.

Currensea cards are now used globally every 10 seconds, with card usage doubling across 2023 compared to the previous year, as the UK’s appetite for travel returns alongside a growing awareness of high foreign exchange rates and a demand for enhanced value when spending abroad.

Alongside cutting costly foreign exchange fees for users, Currensea users are making a positive environmental impact when they spend on their cards – with travellers removing 7 million plastic bottles from the ocean through donations to environmental causes.

James Lynn, Co-Founder of Currensea, said: “With rising costs at home, travellers are increasingly demanding value on their holidays. Currensea’s simple solution to remove FX fees has now saved travellers over £3 million and counting.

"With UK travellers forking out an unnecessary £2.7bn in FX fees every year, it’s vital that savvy holidaymakers understand the real cost of spending abroad. There is a chronic lack of transparency among many payment options with hidden costs and misleading rates that mislead travellers, ultimately costing them more. It’s just as important for travellers to secure value for money on their travel money as it is to get a good deal on flights and accommodation.

“Currensea’s aim isn’t only to offer travellers the lowest FX fees, we also wanted to provide an effective method for supporting the environmental and sustainable causes close to their heart. It’s inspiring that so many customers have donated to reduce plastic pollution in the ocean and support reforestation efforts.”

Currensea has also just announced that its card can now be used with Apple Pay, unlocking access to lower overseas foreign exchange fees for more customers.

James Lynn adds: “Apple Pay functionality is another major step in our journey to give travellers more control over their money. Offering faster, convenient and more secure payments through Apple devices will support our mission to make travel spending fairer - ensuring that Currensea is not only the most cost-effective option for travellers but also the most hassle-free.”

Currensea is a travel debit card that uses open banking technology to link directly to existing bank accounts, allowing people to spend directly from their current account abroad. Its users benefit from access to the best foreign exchange rates at only 0% to 0.5% above the foreign exchange base rate. By cutting out the normal fees, Currensea saves at least 85% on every overseas transaction. For example, a user spending $1500 while visiting the USA would save £40 compared to using a card from a high-street bank.

- 04:00 am

bunq, the second largest neobank in Europe, launches Finn, a GenAI platform available to all its users. Effectively replacing the search function on the app, Finn will enable bunq users to live the life they want, with help of bunq: plan their finances, better budget, navigate the app, easily find transactions and much more.

Finn is bunq’s own technology, using the most powerful LLMs. “Finn will wow you,” says Ali Niknam, founder and CEO of bunq. “Years of AI innovation, coupled with laser focus on our users, allowed us to completely transform banking as you know it. Seeing Generative AI make life so much easier for our users is incredibly exciting.”

Finn will be familiar to anyone who’s ever used OpenAI’s ChatGPT. It has a chat-style text box where users can ask questions or seek advice about their bank account, spending habits, saving and anything else related to money. Finn gives answers to advanced questions like “What is the average amount I spend on groceries per month?” or “How much did I spend on Amazon this year?”. It can even combine data to answer questions that go beyond transactions, such as “What was that Indian place I went to with a friend in London?”, or “How much did I spend at the cafe near Central Park last Saturday?"

bunq also announced it hit 11 million users across the EU and grew its user deposits by 55% since July 2023, now at 7 billion euros. bunq’s successful use of AI has played a significant role in the challenger’s rapid expansion across Europe.

Announced tonight at bunq Update 24 in DeLaMar Theater in Amsterdam, bunq introduces new features that will help digital nomads and international businesses easily manage their finances.

Free credit cards

bunq launches free credit cards for everyone – ready in just 5 minutes and instantly usable through Apple or Google Pay.

Tap to Pay

With Apple’s Tap to Pay, every Business user can now turn their iPhone into a payment terminal and accept payments on the go. All bunq users get free access to this functionality.