Published

- 05:00 am

FINEXPO, the world's leading event organiser, announced today that it is hosting its first-ever FinTech Festival Asia (FTF Asia) on 27 and 28 September 2023 at the Royal Paragon Hall in Bangkok, Thailand.

The FinTech Festival Asia 2023 held by FINEXPO is an exciting two-day event filled with cutting-edge presentations, interactive exhibits, and networking opportunities with some of the brightest minds in the industry. The event aims to bring together industry experts, startups, investors, regulators and FinTech enthusiasts to explore the latest trends and developments in the rapidly evolving fintech landscape.

FINEXPO has curated a wide range of interactive sessions and networking opportunities to ensure attendees get the most out of the event. After organising conferences, forums, summits, shows, exhibitions, and festivals all over the globe for 2 decades, FINEXPO is finally organising its first event in Thailand. With an estimated 15,000 participants from Thailand and across the globe, FTF Asia is the perfect platform for modern fintech companies to explore business opportunities and collaborations.

A wide range of industry topics will be covered at the FTF Asia conference, including banking, payments, personal finance, InsurTech, AI, digital assets and WEB3, blockchain, exchanges, RegTech, Robo-Advisors, P2P, investments, trading, and cybersecurity. It strives to create phenomenal shows and a substantial events series, making FTF Asia a must-attend event for everyone in the industry. With speakers and attendees exchanging knowledge, FINEXPO is excited to witness the possibilities of the connected world.

As a pioneer in Southeast Asia in adopting the latest technologies to improve and expand the country's capacity for technology, Thailand is the perfect location to host this event. FTF Asia will serve as a hub for modern fintech companies, offering opportunities to expand their businesses and collaborate with like-minded individuals. FTF Asia is a global series of innovative, interactive, and networking events that unite thousands worldwide to explore the latest developments and ideas in the fintech industry under one roof.

The team at FINEXPO is excited to welcome the global fintech community to Bangkok, Thailand, for Fintech Festival Asia 2023 and is confident that the event will be a resounding success. Grab this opportunity to improve your knowledge and meet international speakers and the best presenters from around the world. Join the networking app FINEXPO Asia on your mobile phone to view program details and participate in polls and forums. For further information on Fintech Festival Asia 2023 and ticketing, please visit https://fintechfestival.asia/.

- 08:00 am

Spendesk, a 7-in-1 spend management solution for SMEs, has today shared the findings of a survey carried out with the global finance community CFO Connect, looking at the salaries of business finance leaders of all levels in Europe and the US.

Key findings:

Women in UK finance roles on average earn 23% less than men and overall 12% less in the Europe and US

In the UK, 33% of finance professionals don’t feel they are fairly compensated

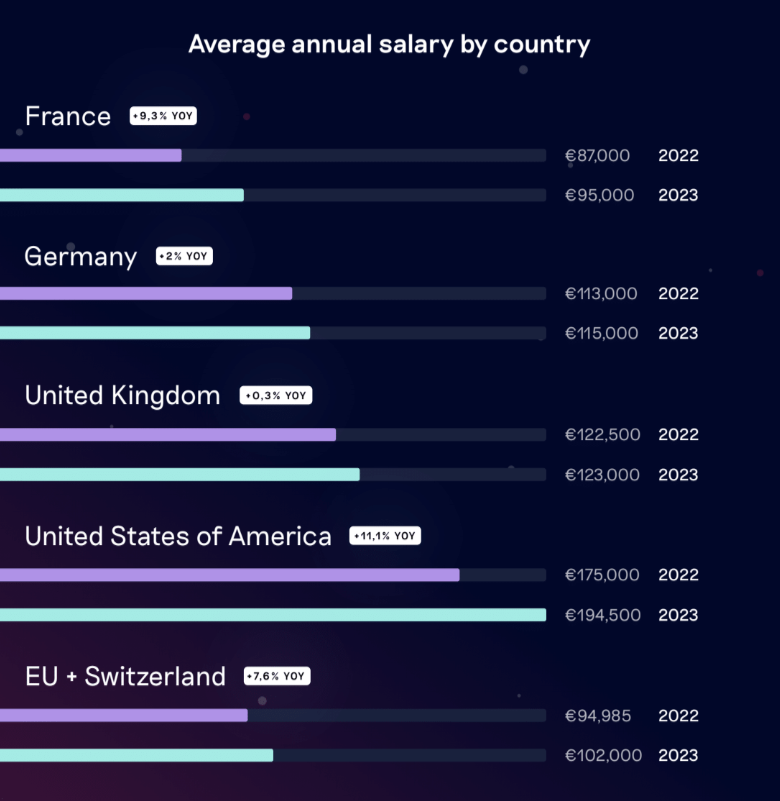

The average finance salary in the US is almost double that in Europe

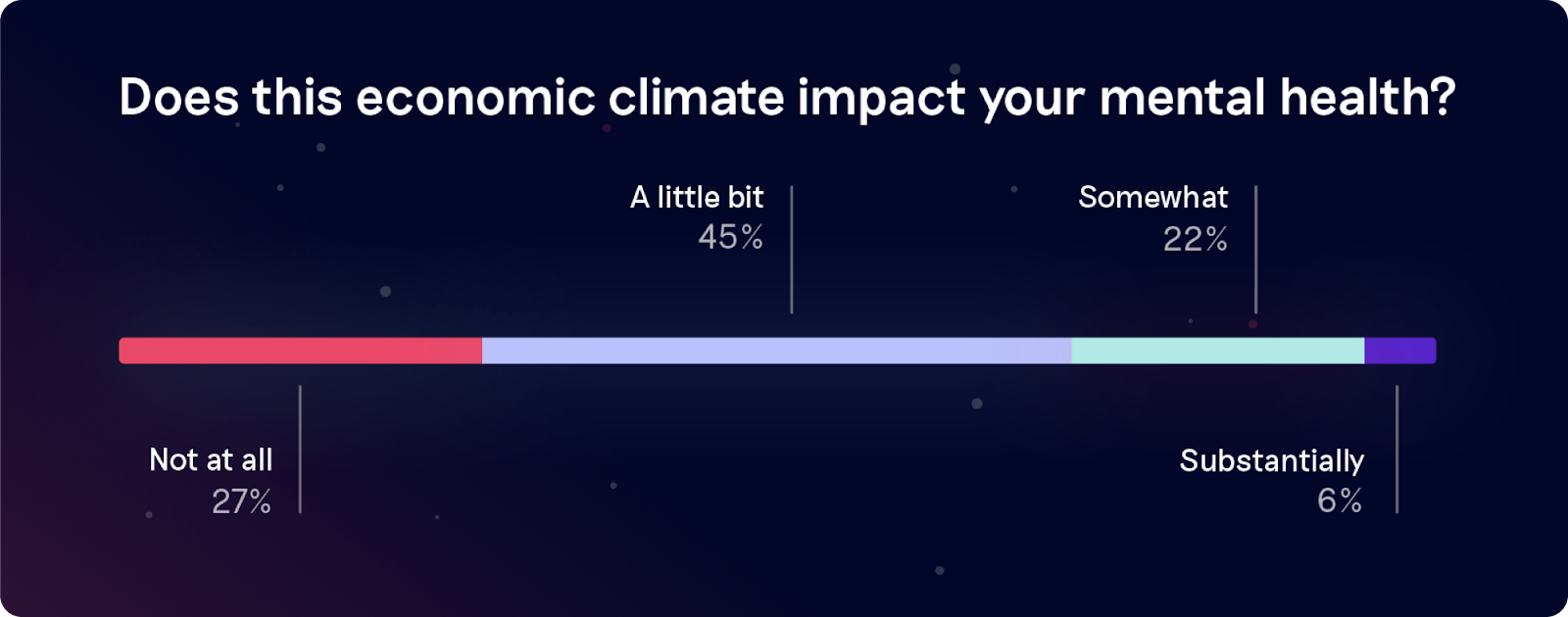

In the UK, 81% of finance professionals felt the current economic climate has had an impact on their mental health

The average overall finance salary in the US is €194,380 / £167,030, which is almost double the €102,192 / £87,813 of Europe. In line with last year’s survey, the UK’s €122,896 / £105,604 average remains Europe’s highest.

In the UK specifically, the findings revealed women are paid on average 23% less than men for the same finance roles. This gap has narrowed by 7% since 2022 (it was 30%); however, it does highlight the fact that the UK’s progression for pay equality is falling behind other countries, which all have less disparity.

When including Europe and the US, women earn on average 12% less than their male counterparts, which has improved by 1% since 2022. Overall, the discrepancy in pay is reflected in job satisfaction, with two-thirds of men feeling that they are fairly compensated, versus 59% of women.

The pay gap is different depending on roles, with senior positions being more closely aligned. For example, the average salary across Europe and the US for a female Chief Finance Officer (CFO) is €140,707 / £121,241, whereas the male equivalent averages at €142,604 / £122,870 – a gap of 1.3%.

In contrast, at mid-level, the pay gap is turned upside down with female Heads of Finance earning 6.1% more than their male counterparts - €98,930 / £84,823 (female) versus €92,908 / £79,660 (male).

The current economic climate and its effect on mental health

Navigating the turbulent headwinds of the economy has not been easy for many businesses, and finance teams have felt their fair share of the difficulties. When surveyed, the majority (73%) of finance leaders felt the current economic climate has had an impact on their mental health. That said, only 6% said the impact was “substantial”.

In the context of the economic climate, women seem to be affected more (80%) than men (70%). Interestingly, German finance professionals are more confident than their peers, with 37% of them stating that their mental health is “not impacted at all” by the current economic context.

The region that is most affected is the UK — 81% of finance professionals have been affected.

Commenting on the results, Rodolphe Ardant, founder and CEO of Spendesk, said: “It’s encouraging to see a slight decrease in the gender pay gap, but of course we would rather not have any gap at all. This should be a cause for concern for all companies. We need to see more determined action to achieve genuine pay parity. Employers who fail to guarantee appropriate equitable remuneration risk losing the very best talent, which then risks the growth and survival of their business.”

He adds: “Now, in the context of years of economic instability, we also see real mental health impacts on finance professionals. We can’t ignore this. We all aspire to create work environments that are open, fulfilling, productive, and enjoyable for our teams. It’s time for companies to recognise the critical importance of pay equity and mental well-being, and take concrete steps to foster a healthy, inclusive work culture.”

The full results of the study can be found here.

- 05:00 am

Dr. Sherif Farouk, Egypt Post Chairman, witnessed the agreement between Egypt Post and Qardy, which enables Qardy to provide its services to Small and Medium-Sized Enterprises (SMEs) in Egypt through Egypt Post's network over 4,300 post offices across the Egypt.

This partnership agreement was signed by Mr. Khaled Emam, Egypt Post Vice Chairman for Financial Inclusion, and Mr. Abdel Aziz Abdel Nabi, Qardy’s founder, in presence of all executive leaders.

According to Dr. Farouk, this partnership aims to give SMEs the power of debt financing through Qardy and Egypt Post branches across Egypt. Qardy allows SMEs to easily fulfill their financial requirements through a hassle-free and streamlined process.

Dr. Farouk stated “this agreement reflects Egypt's efforts to achieve financial inclusion for all groups of society and provide various funding models through postal branches, which help Egypt's economy grow and encourage its culture of freelancing in various parts of Egypt by relying on the great possibilities of postal infrastructure and geographical deployment of post offices throughout Egypt, which reached 4,300”.

According to Mr. Abdel Nabi, we are happy and proud to sign this agreement. Qardy will make sure each customer is matched with the best financial institution. Through our partnership with Egypt Post, which is the largest non-banking financial institution in Egypt with branches that span over 4,300 across Egypt to support SMEs get access to hassle-free wide range of facilities.

Qardy’s vision is to support SMEs to have access to all their financial needs and supporting the adoption of digital transformation and financial inclusion in Egypt; since SMEs represent 80% of Egypt’s GDP and 75% of Egypt’s work force. Qardy is the 1st online lending marketplace in Egypt for financial institutions to fund SMEs.

- 04:00 am

"IDVerse uses generative AI to deliver an end-to-end SaaS solution for identity verification and fraud protection for businesses globally. The primary differentiators of IDVerse’s identity verification solution include zero bias-tested AI, deepfake defender, facial tokenization, and IDOps to optimize the identity verification features,” says Vishal Jagasia, Senior Research Analyst at Quadrant Knowledge Solutions. “The company continues to make improvements in customer onboarding and expand to cover all relevant ID documents in the present markets to enhance detection and improve user experience," adds Jagasia.

- 08:00 am

Research exploring how UK finance decision-makers plan, manage and deliver the finance function reveals that more than a third (39%) take over a week to prepare and submit month-end reports. Worryingly, almost one in five (17%) reported that it can take more than a fortnight – with unreliable data being the most significant cause of delay.

Delayed month-end reporting places additional and unnecessary pressure on finance teams, as well as creating significant business risk by not providing crucial financial information to business leaders in a timely manner.

The sizable survey, commissioned by award-winning accounting software provider iplicit, sought the opinion of 1,000 UK-based finance decision-makers working in organisations that employ between 50 and 500 employees.

The report also highlights additional stumbling blocks in delivering month-end accounts, with the top reasons being:

18% reported having unreliable data that needs checking

17% reported needing to work across multiple incompatible systems/ data points and having a lack of internal resources

A lack of resources is a problem that the accounting profession is facing as a whole, with a recent survey by the Association of Chartered Certified Accountants reporting that two-thirds of accounting firms are finding it difficult to recruit the right talent.

Moreover, UK finance decision-makers say they are restricted by missing data (12%) and having a reliance on many slow manual processes (11%).

Paul Sparkes, Commercial Director at iplicit, reflects on the results, “Spending longer than needed on month-end reporting significantly eats into precious time and resources – both of which have significant bottom-line ramifications for organisations regardless of their size, or sector.”

Over the past three years, organisations have faced an extraordinary array of new challenges. From supply chain disruption to the great resignation, as well as inflation and rising interest rates – the finance teams’ forecasting and traditional measures of business performance have been turned on their head.

On top of this, business risk has escalated and with the ongoing lack of confidence from the CBI, companies urgently require fast access to deep, accurate financial information to support vital decisions.

Sparkes adds, “A lack of rapid insight into business performance is not only hugely frustrating, but it creates a significant risk which is not something any business should tolerate.

I question whether UK finance decision-makers are being held back by their accounting and finance systems and processes.”

Many finance teams still use time-consuming manual processes for adjustments and the allocation of expenses across different business units – core activities that could and should be automated. This will improve accuracy and reduce the burden on the finance team

Sparkes concludes, “Missing and unreliable data will clearly create frustration amongst finance decision-makers. Without careful consideration of how to address these challenges, finance departments could be facing the perfect storm of dealing with unreliable data, lack of resources and inefficient systems to generate their month-end reports.”

You can view the full results of the independent market research in the report titled: ‘A study into how to overcome the barriers of moving to a true cloud accounting system’.

Jason McKee

Director at Nine Moons Ltd

Blockchain technology emerged in 2008, even though it only rose to popularity when cryptocurrency became mainstream. see more

- 05:00 am

TransUnion, a global information and insights company, has released its latest Consumer Pulse study, revealing that a significant portion of the UK population remains financially stable despite rising interest rates and persistent inflation.

The figures illustrate a contradictory picture of the financial landscape among UK consumers. On one hand, almost six in 10 (58%) have proactively taken steps to reduce their discretionary expenditures such as dining out, travel and entertainment, with plans for further cuts in the future. However, three-quarters (75%) of consumers remained steadfast in their belief that they can pay their upcoming bills and loans in full.

James Robinson, managing director of consumer interactive at TransUnion in the UK, commented: "Our recent Consumer Pulse study underlines a significant divergence within the population, indicating the varying effects of the cost of living crisis. Despite the challenges presented by rising interest rates and inflation, it’s encouraging to see that many consumers are displaying resilience, which bodes well for the future. As we navigate the evolving financial landscape, it’s crucial for businesses and financial institutions to understand and adapt to these distinct circumstances."

Access to credit

TransUnion’s study sheds light on the evolving dynamics of consumer access to credit. In fact, despite the fact that the majority of UK consumers (77%) believed access to credit and lending products was important to achieve financial goals, less than half (47%) said they had sufficient access.

Additionally, the figures highlight the widespread recognition of the importance of credit report monitoring among UK consumers, as nearly eight in 10 (76%) acknowledged this.

James Robinson continued: “Our study shows that over half (54%) of UK consumers are monitoring their credit report at least quarterly, reflecting a proactive approach towards maintaining a healthy credit standing and making informed financial decisions. We’re really pleased to see that consumers are starting to better understand their credit information and how it’s used. However, we want to drive further improvement in this area and are working closely with our partners, from high street banks to leading credit score providers, to achieve this.”

For those seeking new credit, the most popular choice was credit cards, according to the latest figures, with 42% planning to apply for a credit card in the next 12 months. Buy now, pay later also proved popular, with more than two in 10 (22%) intending to use these services in the coming year.

Personal loans and mortgage applications

TransUnion’s research showed a significant decline in personal loan demand from UK consumers. Of those who said they’d apply for new credit or refinance existing credit in the next year, less than two in 10 (19%) planned to apply for a personal loan. That’s a considerable decrease from the 36% recorded during the same quarter last year.

Similarly, there was a decrease in stated mortgage demand, as expected, from 21% in Q2 2022 to 16% in Q2 2023, most likely influenced by the current instability in the UK housing market and the substantial rise in mortgage rates. Given that interest rates have climbed, potential homebuyers and existing homeowners appear to be re-evaluating their decisions and adjusting their mortgage plans accordingly.

Generational differences in financial outlook

James ODonnell, director of research and consulting at TransUnion in the UK, added: "We’re seeing distinct differences in how cost of living impacts consumer credit demand among different generations. A significant portion of Gen Z and Millennials, 48% and 41% respectively, expressed their intentions to explore new credit opportunities, compared to 6% for Baby Boomers. These findings provide valuable insights into how varying financial goals, sense of financial security, lifestyles and priorities contribute to the contrasting credit patterns observed across generations.”

Despite the challenges posed by rising interest rates and inflation, more than six in 10 (63%) of UK Gen Z consumers expressed their intention to either increase or maintain their discretionary spending. This positive outlook indicates confidence in their financial stability and their belief that they can weather the storm caused by economic fluctuations, with more than a quarter (26%) of Gen Z respondents planning to increase their in-store or online retail shopping in the coming months.

- 07:00 am

IDEX Biometrics is expanding its presence in Asia with Beautiful Card Corporation (BCC), one of the top 10 smart card manufacturers globally. BCC will ramp production of the IDEX Pay Biometric card solution in response to increasing demand from issuers and banks in the region.

With an annual production of 121 million payment cards1, BCC specializes in the manufacturing, personalizing, and packaging of payment and multiple-application cards. As a leading smart card provider, BCC provides eco-sustainable card solutions and is certified by VISA, Mastercard and JCB. BCC’s expertise, combined with the IDEX Biometrics cutting-edge hardware and software authentication solutions, will support market acceleration in Asia and around the world.

“We are thrilled to collaborate with IDEX Biometrics, leveraging their leading technology to enhance the consumer reach of biometric smart cards. Through our global client portfolio and ecosystem partners, we aim to deliver a seamless experience that meets the growing demand from consumers,” stated Shellen Hsu, Global Vice President, Sales, and Business Development of BCC.

“We are delighted that BCC has selected IDEX Biometrics in support of our expansion in Asia,” said Catharina Eklof, Chief Commercial Officer of IDEX Biometrics. “With BCC’s extensive portfolio and expertise in smart card manufacturing, we are excited to advance the scaled adoption of biometric smart cards globally.”

- 06:00 am

London-based fintech Silverbird has made a senior appointment, hiring Stu Bailey as a Chief Product Officer.

In his new role as a CPO, Bailey, who was previously CPO at Currencycloud, will be responsible for scaling Silverbird’s infrastructure as it grows internationally, helping liberate cross-border trade.

Silverbird is a modern global payment system that offers small and medium-sized enterprises a seamless and fully digital process for joining their platform. It eliminates the need for in-person interviews or visits to a physical branch. All required documents are managed electronically, saving entrepreneurs the unnecessary hassle of travelling outside their home country to open a bank account. This empowers small businesses to efficiently manage their finances from anywhere.

With lightning-fast transactions completed within seconds, Silverbird's banking services cover 200 countries. The company specifically focuses on collaborating with exporters and importers, allowing them to provide exceptional service and effectively fill the void left by traditional banks.

Stu Bailey said he’s joining the company “in a time of walls going up between countries”, so “it's heartening to work for a business that's liberating cross-border trade.”

He continued: “Max Faldin and team are focused maniacally on liberating global trade — a purpose that chimes massively with me and with the international merchants who are our customers.”

Silverbird Founder and CEO Max Faldin said: “The moment I met Stu I knew immediately he is a rockstar. On top of that, he has extremely relevant experience from his previous work with CurrencyCloud, our major banking partner. I couldn’t be more excited to have him on board.”

- 04:00 am

Shinkansen, a burgeoning FinTech start-up hailing from Chile, has recently celebrated the successful closure of a seed investment round.

The young company is known for its revolutionary approach to speedy financial transactions, reflecting the swift movement of Japan’s Shinkansen train network which inspired its name.

A considerable $3m was raised in this funding round, which was spearheaded by Mexico’s eminent venture capital firm, ALLVP, according to a report from Tech Gist Africa. Notably, the round also saw contributions from Salkantay, Chileventures, and Pedro Pineda, the co-founder of Fintual and a Sequoia Scout, who all threw their financial support behind Shinkansen.

The company, named after the famous Japanese high-speed railway system, has carved a niche in the FinTech sector by focusing on expediting money transfers and transactions. Its innovative application programming interface (API) integration system is a game-changer for the Latin American market, which has often grappled with the challenges of country-specific integrations.

The raised funding is set to underpin Shinkansen’s growth ambitions, with a particular focus on expanding its presence across Latin America, including markets such as Mexico and Peru. This move aims to streamline money movement in these fragmented markets, boosting efficiency and bypassing regulatory roadblocks.

An additional standout feature of Shinkansen is its adept use of artificial intelligence to automate operations, allowing for seamless integration of its APIs with banks in Chile, Colombia, Mexico, and soon, Peru. Further underlining its innovativeness, Shinkansen operates a “regulator-friendly” model that ensures security and traceability by not directly handling money flow.

The company’s early clientele list boasts notable names like Xepelin, Buk, and Buda, alongside stockbrokers, insurance companies, and retail chains. Its technical prowess and emphasis on AI have been commended by investors, marking Shinkansen as part of a new generation of companies that give priority to AI from the outset.

ALLVP partner said, “We have had successful investments in Chilean teams before and we see promising similarities with the Shinkansen team. Their focus on user experience and regulatory compliance aligns with our own values, leading us to support their growth in the region.”