Published

- 01:00 am

A leading payment orchestration provider, BR-DGE, has announced today its integration with PayPal to offer merchants greater payment choice and flexibility at online checkout. This collaboration between the two companies offers the latest integrations for BR-DGE merchants with PayPal’s complete payments platform (PPCP) and the PayPal Braintree platform.

PayPal’s complete payments platform (PPCP) is enabling businesses of all sizes across the global economy to drive conversion by giving them the ability to reduce friction at checkout, offering customers an easy and secure way to pay online and in-app. Through this collaboration, BR-DGE’s merchants will have access to the latest PayPal technology enabling them to offer cutting-edge payment innovations to consumers via BR-DGE Connect, its payments ecosystem connectivity tool. Merchants will be able to access PayPal’s full stack of payment methods and features, including PayPal Pay Later and Venmo in the US coming later this year, and offer consumers greater flexibility at checkout.

Recent research from BR-DGE found that 32% of consumers say the availability of payment options is a high priority in their purchasing decisions. Leveraging PayPal’s existing foothold and global strength in payment acceptance, BR-DGE can meet this demand for merchants and deliver a better payment experience for consumers via a scalable checkout solution.

As part of the integration, BR-DGE merchants will also have access to PayPal Braintree, allowing them to reach more buyers and drive higher conversion among customers. PayPal Braintree empowers consumers globally with the ability to pay how they want at leading e-commerce retailers. BR-DGE merchants can now access market-leading solutions from a trusted and experienced brand that empowers hundreds of millions of consumers and merchants across more than 200 markets, and offer these services to consumers via one single integration.

Tapping into BR-DGE’s market-leading position, PayPal will also have access to a global network that empowers merchants across travel, leisure, retail and beyond.

Commenting on the partnership, Tom Voaden, Head of Partnerships at BR-DGE, said: “We are on a mission to empower merchants with the latest payment innovations the industry has to offer. By partnering with PayPal, we are able to meet merchant and consumer needs with an easy-to-use and frictionless payment solution. As we look to process over £1.5 billion of transactions this year, this partnership will help our merchants drive revenues and provide customers with the best possible payment experience. We look forward to working with the PayPal team on this collaboration.”

Led by CEO Thomas Gillan, BR-DGE’s platform is revolutionizing online payments for merchants by offering a universe of payment options via a single point of integration. BR-DGE continues to go from strength to strength following a record year of growth in 2023.

- 05:00 am

Zumo, the B2B digital assets infrastructure that prioritizes sustainability, has announced the appointment of Jason Tucker-Feltham as the company’s new Head of Sales.

Tucker-Feltham is an experienced crypto sales, business development, and capital introduction professional. Before joining Zumo, he worked in business development and European sales at Celsius, covering some of the largest institutional clients in the crypto space, and in advisory compliance at UniCredit, where he lobbied for proportionate MiCA regulation on behalf of the entire banking group.

He is an active member of the international crypto community and a regular speaker at conferences worldwide. Before entering the crypto world, Tucker-Feltham spent over a decade working at global investment banks, including Deutsche Bank. He holds the Financial Risk Manager (FRM®) certification from the Global Association of Risk Professionals (GARP).

Nick Jones, Founder and CEO, Zumo said: “Jason has a rich background in financial services and deep expertise in EMEA institutional sales in the crypto sphere. He is also passionate about digital assets and their potential to transform the financial industry – and wider society – making him a great fit for our team.”

“Jason will lead our sales push at a pivotal time for our growing industry, helping us to work with financial institutions keen to create new digital asset propositions whilst protecting their customers and the environment.”

Jason Tucker-Feltham, Head of Sales, Zumo added: “Last year, the UK’s crypto industry was caught off guard when the FCA introduced new rules for financial promotions. Some industry participants even chose to exit the market due to these changes. However, there are ways to navigate the UK crypto market while staying compliant. By teaming up with Zumo, no one needs to miss out.”

“Zumo offers a range of elegant solutions that open up new crypto business possibilities, including our compliant route to accessing the UK crypto market. I’m thrilled to be joining an award-winning firm that enables our clients to capitalise on the endless opportunities arising from the fast-growing digital assets sector.”

Zumo is a digital-asset-as-a-service platform and the market’s only full-stack infrastructure. It enables financial institutions to launch digital asset propositions engineered with a focus on compliance and sustainability.

Last year, Zumo launched Oxygen, the first of its kind – a full solution for financial institutions to measure, mitigate and report on the carbon footprint of digital currencies in line with evolving regulations and investor expectations.

Zumo was also the first digital asset platform to integrate the tech-based requirements of the FCA’s financial promotions regime for cryptoassets, underscoring its unwavering commitment to setting the highest standards in regulatory alignment and consumer protections.

- 09:00 am

Fiserv, Inc., a leading global provider of payments and financial services technology, is partnering with Genesis Bank, one of only two diverse multiracial Minority Depository Institutions (MDIs) in the country, to drive economic empowerment and create positive impact in local communities.

Beginning this month, small businesses located primarily in low-to-moderate income (LMI) communities served by Southern California-based Genesis Bank will have access to customized technology bundles. Specifically designed to address challenges faced by these businesses, the bundles will provide access to select Clover point-of-sale (POS) technology from Fiserv with no or low entry costs and significantly discounted subscription fees.

“We are incredibly excited to be partnering with Fiserv to offer this low-cost retail solutions bundle to small- and mid-sized businesses,” said Stephen H. Gordon, Chairman and Chief Executive Officer of Genesis Bank. “As the underlying nature and complexity of technology continues to evolve, gaining access to advanced POS systems has become essential for businesses to effectively operate, compete, and grow. Genesis Bank recognizes cost burden as being a significant barrier to gaining access to such essential technology, especially for the diverse small business owners and entrepreneurs that have historically been underserved. Accordingly, we believe this affordable Clover offering will further support our mission to make an impact in the diverse, entrepreneurial LMI communities we serve across Southern California, extending our collective reach into those businesses in need of such essential technology.”

“The best way to help small businesses is to meet them where they are, and many of our MDI clients are already there,” said Neil Wilcox, Head of Corporate Social Responsibility at Fiserv. “By partnering with Genesis Bank, we can support their growth and help maximize their impact by providing critical financial technology resources to the businesses that play a meaningful role in creating the vibrant and entrepreneurial communities that comprise Southern California, the second largest and most diverse demographic in the U.S.”

- 07:00 am

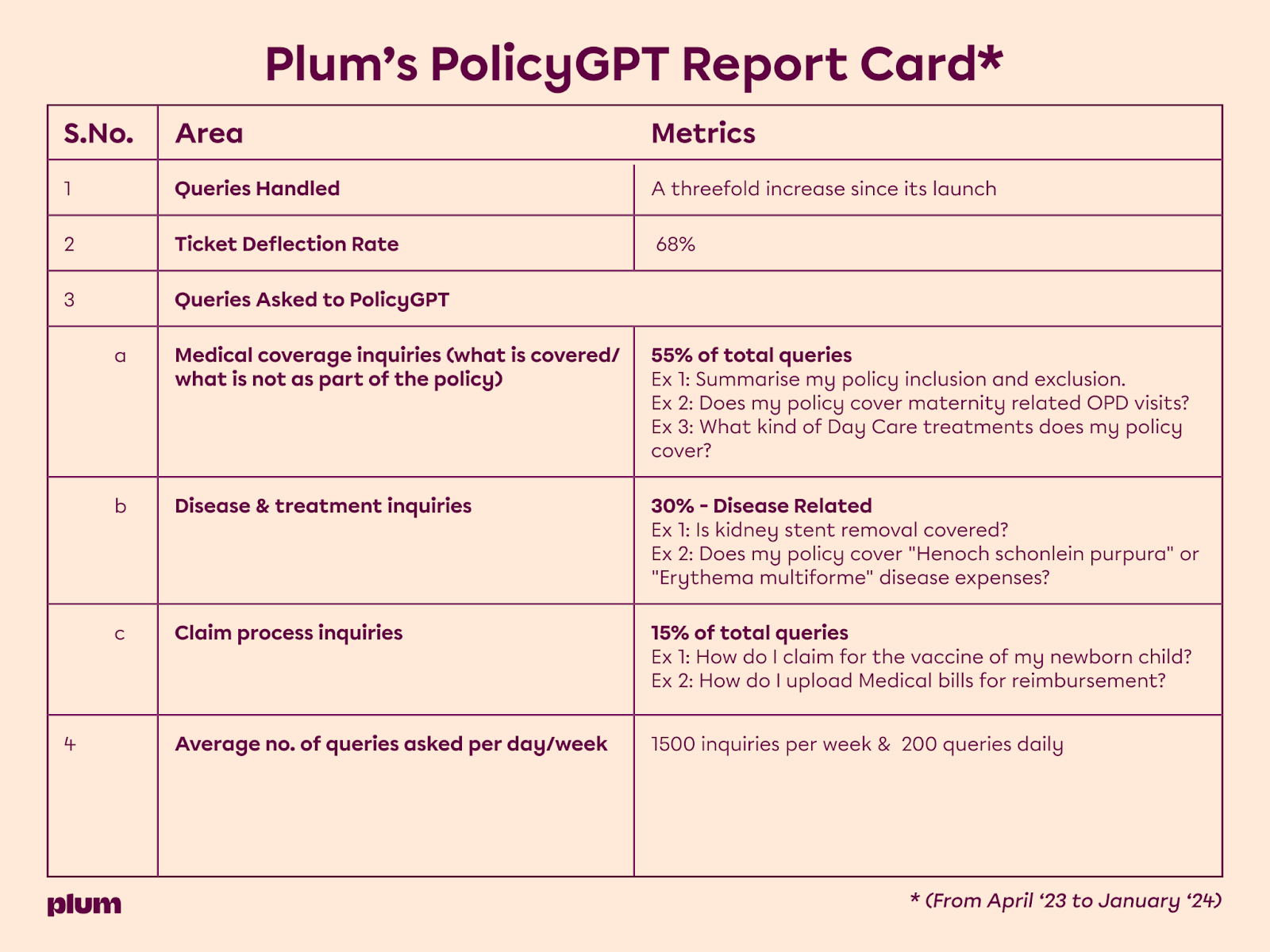

Plum, India’s leading insurtech platform offering group health insurance and business insurance solutions to over 3500+ corporations, has shared a report card of its proprietary PolicyGPT tool which was launched in April 2023. The AI-powered bot has seen a threefold increase in adoption (from launch), successfully resolving 68% of customer inquiries and empowering customer success agents to focus on personalized claims support to deliver a superior customer experience.

PolicyGPT has been built upon a sophisticated architecture called RAG (Retrieval Augmented Generation) powered by OpenAI’s most capable GPT model and is used to provide users with information about their health insurance policy purchased from Plum. It has access to user policy details and general knowledge of health insurance, with the primary goal of educating users about their policies' benefits and instilling transparency in an otherwise hairy industry.

Saurabh Arora, Co-Founder and CTO of Plum said, “The integration of technology and insurance is crucial for simplifying complex issues and driving efficiencies. PolicyGPT represents a significant step in empowering consumers with seamless and swift resolution of their queries. Plum's endeavor to advance its technological capabilities adds value to customers' lives by ensuring they can navigate the complexities of insurance easily and confidently. Industries such as health and insurance often evoke feelings of anxiety among consumers when faced with problems or emergencies. The ability of PolicyGPT to promptly address these concerns without the need for human intervention can significantly alleviate these sentiments."

The future of LLMs lies in increasing bot-led interactions and decreasing response time. Even with PolicyGPT, the goal is to scale by increasing the ticket deflection rate and reducing manual responses - this will help with customer delight for the overall claims process. Some of the areas identified (based on customer queries) include:

Medical coverages - diseases, treatments covered

Policy inclusions, exclusions

Claims processes and how to file claims

Debankur Biswas, Senior Vice President and Head of Operations at Plum expressed, ‘’PolicyGPT highlights Plum's commitment to change customer service and experience in the insurance industry. Insurance is a business of customer-centricity, trust and timeliness, and PolicyGPT has proven to be a powerful tool in addressing these aspects. With a ticket deflection rate of 68%, PolicyGPT helps the customer service team to save up their valuable time, allowing them to focus on resolving more complex and challenging inquiries, ultimately enhancing the overall quality and effectiveness of customer service operations."

Plum has introduced several innovative features in the past to improve customer experiences, such as WhatsApp claims, paperless reimbursements (e-imburse), and its highly-rated mobile app, which currently holds a 4.1 rating on Android and a 4.3 rating on iOS. With PolicyGPT and the adoption of GenAI, Plum continues to lead the way in the insurtech industry, providing exceptional value to its consumers.

- 03:00 am

BABB, a socially focussed P2P mobile banking platform, today announces the ReDeFi project – a new decentralized FMI (Financial Market Infrastructure) platform that redefines our current financial system, by merging the reliability of traditional finance with the immutability of blockchain technology. ReDeFi eliminates many of the traditional barriers to financial inclusion, ushering in a new era of enhanced transparency, efficiency, and affordability in financial transactions.

Central to ReDeFi's vision is the Onchain Money model, a first-of-its-kind tokenized deposit system that preserves the Singleness of Money principle (the idea that all types of money should carry equal worth in a given denomination, be universally recognized for transactions, and be freely exchangeable with any other currency form without diminishing in value). Onchain Money distinguishes itself from the volatility of cryptocurrencies and the limitations of stablecoins by offering a blockchain-based representation of fiat currencies like GBP, directly mirroring funds in traditional bank accounts without necessitating token issuance.

Onchain Money integrates smart contracts into the existing infrastructure that banks and financial institutions use, providing value and convenience, while Onchain Money can be sent to and received from any supported bank (local or overseas) using traditional account details.

With Onchain Money, transactions are reduced in cost, occur seamlessly and near-instantaneously around the world, and fully adhere to regulatory standards. The platform also eliminates the need for middlemen, such as banks and brokerage firms, therefore further reducing transaction costs.

Furthermore, Onchain Money transaction fees are also transparent and verifiable on the blockchain, regardless of geographical location or currency. Unlike today’s financial systems, where fees vary based on currency and merchant bank location, Onchain Money utilises its own blockchain network to solve that problem. This eliminates the complexity and extra costs associated with cross-border transactions, making financial exchanges simpler and more cost-effective for all parties. Currently remittance costs average 6.8%, disproportionately affecting communities in developing economies.

ReDeFi will be launching its layer-1 blockchain with Onchain Money to follow, before the IDO and token sale this year.

ReDeFi and Onchain Money is the brainchild of BABB, a fintech mobile banking platform established in 2018 that promotes financial inclusion and social impact by enabling cost-effective financial solutions.

Rushd Averröes, Founder and CEO, ReDeFi, said:

“At the heart of ReDeFi is Onchain Money, a new model that blends traditional banking with the efficiency of blockchain technology, thereby reforming and augmenting - rather than replacing - existing monetary systems. We are hugely excited about the potential of this new model for everyday people, businesses, banks and governments around the world.”

- 03:00 am

Abu Dhabi Islamic Bank, a leading financial institution, announced the successful launch of a new payment hub that allows customers to conduct their transfers in a quick and efficient manner. ADIB has worked with the real-time payment solutions company, ProgressSoft, to ease the integration of Cross-Border Services and accelerate cross-border remittances.

With the new payment hub, customers can now seamlessly process transfers, providing a solution that transforms payment processing capabilities. This redefines the speed, security, and efficiency of ADIB's payment services across diverse channels and third-party networks.

ADIB, committed to fostering innovation and surpassing customer expectations, has strategically implemented ProgressSoft's Payments Hub, marking a significant upgrade in its technologies, and facilitating a seamless migration from legacy payment systems to a robust platform.

Commenting on the launch, Fernando Plaza Lopez, Chief Digital Officer, ADIB, said: “The successful implementation of ProgressSoft’s Payments Hub Platform comes at a time when ADIB is focused on driving digital-first solutions throughout the bank’s operations. This robust new platform will transform the way ADIB’s payment services function across the board. In line with our commitment to delivering digital excellence for our customers, ADIB will continue to develop its digital capabilities to offer bespoke solutions for all our stakeholders.”

The dynamic platform aligns with ADIB's vision for expanding digital services at the front end as well as global payment corridors at the back end. With advanced and scalable features, ADIB also gains the flexibility to adapt effortlessly to market trends, enabling the introduction of additional payment services with minimal disruption to its back-end systems. This robust and scalable payment infrastructure solidifies ADIB's position as a leader in the digital banking landscape, paving the way for its ambitious growth strategy in the UAE and beyond.

“This successful launch signifies the culmination of a shared vision between ADIB and ProgressSoft,” stated ProgressSoft’s Chief Executive Officer, Michael Wakileh, “Together we have launched a transformative platform that not only addresses the demands of today but also anticipates the needs of tomorrow, reinforcing our joint commitment to delivering excellence in banking services.”

This significant milestone marks the inauguration of ADIB and ProgressSoft’s partnership, ushering in a new era in banking where pioneering strategies and customer-focused solutions stand as the driving forces.

- 04:00 am

CME Group, the world's leading derivatives marketplace, today announced it plans to further expand its cryptocurrency derivatives offering with the addition of Micro Bitcoin Euro and Micro Ether Euro futures on March 18, pending regulatory review.

"Global investors have sought more precise tools to manage their risk as interest for bitcoin and ether grows. As such, we have seen a four-fold increase in volume in our USD-denominated Micro Bitcoin and Micro Ether futures," said Giovanni Vicioso, Global Head of Cryptocurrency Products at CME Group. "The launch of these new Micro Euro-denominated contracts will provide clients with additional products to more efficiently hedge bitcoin and ether exposure in the second-highest traded fiat behind U.S. dollar-based contracts. Year-to-date, 24% of Bitcoin and Ether futures volume at CME Group has been transacted from the EMEA region, and we continue to develop additional tools for clients there to hedge their crypto portfolios and express or take a view on potential market moves."

Designed to match their U.S. dollar-denominated counterparts, Micro Bitcoin Euro and Micro Ether Euro futures contracts will be sized at one-tenth of their respective underlying cryptocurrencies. These new futures contracts will be listed on and subject to the rules of CME.

"TP ICAP will support this market-defining crypto derivative from CME Group by providing block facilitation services to this product. Our global Digital Assets business has been providing price discovery and execution services on CME Group's suite of crypto derivatives since the start of 2020, leveraging TP ICAP's strengths in connecting market participants as the foundation for our Digital Assets proposition," said Sam Newman, Digital Assets Head of Broking at TP ICAP. "Interest in crypto derivatives has seen huge worldwide growth in recent years and these new euro-denominated micro futures contracts will help further expand the accessibility and utility of crypto derivatives, particularly within Europe."

CME Group's Cryptocurrency product suite continues to provide consistent liquidity, volume, and open interest for clients seeking to hedge their risk or gain exposure to the asset class. January was a record month in terms of average daily volume (71K contracts) across all Cryptocurrency products. In addition, average daily open interest for Bitcoin and Ether futures reached all-time highs for the month (23.5K contracts and 6K contracts, respectively). Micro Bitcoin and Micro Ether futures also saw a trading surge, with average daily volumes growing 43% versus December 2023.

- 07:00 am

According to a recently released study by Chargebacks911, a fintech company providing payment dispute solutions, the promise of cryptocurrency's widespread acceptance as a means of payment remains far from being realized.

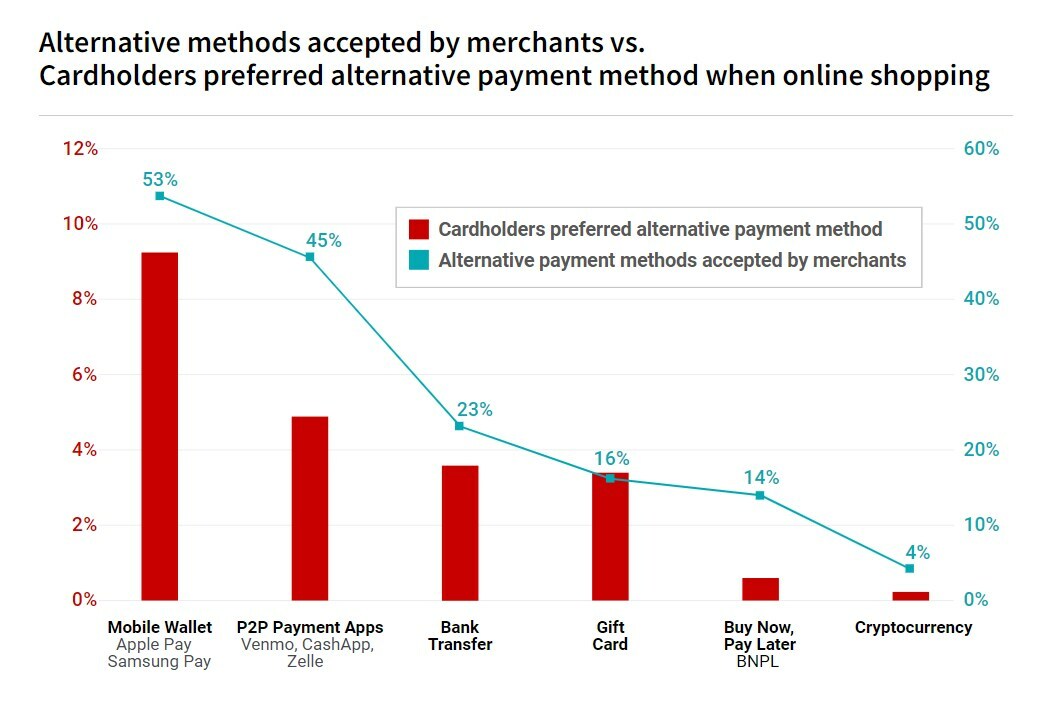

The 2024 Cardholder Dispute Index, created in partnership with analytics and consulting firm TSG (The Strawhecker Group) surveyed 4,000 online shoppers in the United States. Fewer than one percent of respondents identified cryptocurrency as their preferred way to pay online.

Cryptocurrency payments firm Triple-A estimates that 4.2 percent of global consumers own some amount of cryptocurrency. However, given the insights gained from the Cardholder Dispute Index, it seems most crypto holders continue to see digital currencies as a store of value and an investment opportunity rather than a viable currency for day-to-day transactions.

The Cardholder Dispute Index shows that the vast majority of buyers still prefer credit and debit cards over alternative payment methods. 80 percent of those surveyed identified credit or debit cards as their preferred way to buy online. Roughly 10 percent of respondents said they preferred mobile wallets, while a small number of respondents also identified P2P payment apps (Venmo, CashApp, Zelle, etc.), bank transfers, gift cards, and "buy now, pay later" services as other preferred options.

These shopping preferences were mirrored in the Chargeback Field Report, a study conducted by the firm last year that looked at online retailers. That study found that only 4% of sellers offered cryptocurrency as a payment option.

"This is not to say that cryptocurrency is dead," states Jarrod Wright, the head of marketing for Chargebacks911. "However, it's hard to deny that the promise of cryptocurrency as a decentralized, widely accepted means of exchange has failed to materialize so far. If consumers don't want to pay in crypto, merchants won't be incentivized to maintain it as an option."

- 09:00 am

Bloomberg announced today that Commercial Bank International (CBI), a leading national bank in the UAE, has adopted Bloomberg’s Multi-Asset Risk System (MARS) modules for Counterparty Risk, Market Risk, and Valuation.

CBI previously adopted MARS Front Office to aid its LIBOR transition and has now decided to adopt three additional modules of the solution, making MARS the Bank’s primary risk management system. The MARS counterparty risk (XVA) module will notably help address existing regulatory requirements such as SA-CCR for counterparty credit risk capital calculations. The same module provides robust counterparty exposure analytics for derivatives portfolios.

MARS Market Risk module integrates seamlessly to provide a comprehensive solution supporting the risk management and data workflow, providing scalability and allowing further growth of CBI’s treasury business with confidence both in terms of financial product volumes and complexity.

Finally, MARS Valuations provides credible and complete valuations for derivative portfolios, including over-the-counter derivatives and structured products, ensuring data and pricing consistency across the front-to-back trading workflow cycle.

On this occasion, Randa Kreidieh, Chief Risk Officer at CBI, commented: “Using MARS as our primary risk system enables us to streamline our risk management workflows, quickly implement new financial regulations, and improve our operational efficiencies. By adopting additional MARS modules, we benefit from a comprehensive and integrated set of tools, ensuring data consistency and transparency between the front and back office, and enabling us to automate more processes. Such advancements enable more informed decision-making and efficient operations, which contributes positively to both investment management and customer service aspects of banking.”

“We are pleased to continue to support CBI with streamlining and digitizing its risk management processes by expanding the range of MARS modules into an integrated front to back solution,” said Jose Ribas, Global Head of Risk and Pricing Products at Bloomberg. “The ability to bolt on additional risk capabilities as firms progress on their technology journey is a key feature of our MARS offering, in addition to our broad asset class coverage, our pricing library which includes a range of models and automated enterprise workflow that streamlines the entire risk management process.”

Bloomberg MARS is a suite of risk solutions, which are accessed on the Bloomberg Terminal and via APIs, that provides risk analytics for cash and derivatives securities. MARS enables traders, portfolio, and risk managers to manage front office risk, market risk, XVA counterparty risk, credit risk, hedge accounting, as well as collateral and SIMM requirements – all by using a common pricing and data library, providing consistency from front to back. To find out more about Bloomberg’s multi-asset risk solutions, please visit here.

Bloomberg MARS has been recognized across a range of risk management and risk transfer solutions at the 2023 Risk Market Technology Awards, including Market Liquidity Risk Product of the Year, Pricing and Analytics: Structured Products/Cross-Asset, and Best Support for Risk-Free Rates.

- 04:00 am

Amidst demand from consumers for greater flexibility on monthly payments, there is an opportunity for utility providers to unlock greater customer loyalty by investing in payment methods that offer more control and transparency.

That’s according to new research of more than 2,000 UK consumers by Tink, a market-leading payment services and data enrichment platform. Findings reveal that amidst the ongoing cost of living crisis, an estimated two-thirds (66%) of UK consumers believe that utility providers must support customers struggling to pay their bills.

Consumers need greater control and support with monthly payments

With uncertainty around further energy price cap increases, one in five (18%) surveyed UK consumers are currently struggling to keep on top of changes in their regular payments, including increases in monthly utility bills.

Nearly one in five (18%) respondents have defaulted on their regular bills and gone into a debt collection process. While one in five (21%) surveyed have also forgotten about a bill and been charged for going into their overdraft.

The research reveals that consumers want greater control when dealing with their monthly payments, as over half of Brits (51%) say they would welcome more control over how and when they pay their utility bills.

A business opportunity for utility providers

As competition starts to heat up again in the energy market and people search for the best deal, there’s an opportunity for providers to improve the payment experience – to serve their customers in a way that better fits the flow of incomings and outgoings from their accounts.

An estimated one in five (21%) consumers would switch utility providers if offered the flexibility to change the amount they pay each month, while 17% would consider switching providers if offered the opportunity to change the date of their bill payments.

Utility providers who invest in payment methods that offer more control and transparency have the potential to reduce churn and enjoy greater customer acquisition and retention.

Andrew Boyajian, VP of Product for Payments & CX at Tink comments: “During the colder months, when energy and utility bills typically rise, consumers are under increasing financial strain - meaning growing demand for utilities providers to offer more support with managing their bills. With payment flexibility a particular sticking point, investing in data-driven financial services enables utility providers to give customers greater control over their payments – which is especially important during difficult economic times.

“Open banking solutions like VRP (Variable Recurring Payments) can help utilities providers offer support to customers struggling to stay on top of monthly outgoings, with features such as agreed maximum payment amounts and automated retries meaning both parties can have more peace of mind and the ability to adapt to changing circumstances. More flexible payment methods can also be powered by VRP, for example, an agreement with the utility provider to split bills into multiple payments.”