Published

- 09:00 am

Payoneer to begin trading today under ticker symbol PAYO

Payoneer Inc., the commerce technology company powering payments and growth for the new global economy, and FTAC Olympus Acquisition Corp., a special purpose acquisition company, announced on Friday that they have completed their business combination. The business combination was approved by FTOC’s shareholders at an extraordinary general meeting held on June 23, 2021..

Payoneer’s global management team, led by Scott Galit, Chief Executive Officer, Michael Levine, Chief Financial Officer, and Keren Levy, Chief Operating Officer, will continue to lead the Company.

The transaction includes a $300 million PIPE investment from investors including existing investor Wellington Management, as well as Dragoneer Investment Group, Fidelity Management & Research Company LLC, Franklin Templeton, certain funds managed by Millennium Management, funds and accounts advised by T. Rowe Price Associates, Inc., and Winslow Capital Management, LLC.

“We are thrilled to be a public company and join forces with Betsy and the entire FTOC team,” said Scott Galit, Chief Executive Officer of Payoneer. “Through our 15 years, we have built a global platform that is trusted by millions of customers worldwide, from aspiring entrepreneurs to the world’s leading digital brands and are now the go-to partner for digital commerce, everywhere. We are just scratching the surface of the enormous opportunity ahead to help businesses grow and scale in the new global economy. This move into the public markets is an important step on our journey to provide any business, in any market, the technology, connections and confidence to realize their potential.”

Betsy Cohen, Chairman of the Board of Directors of FTAC Olympus Acquisition Corp., stated, “The Payoneer team has positioned the company incredibly well to capitalize on the expansion of global commerce, and we are proud to be their partner during this next phase of growth. Payoneer has a strong balance sheet with ample capital to expand its already broad suite of services, both organically, by deepening existing merchant relationships and continuing to build new ones, and through strategic acquisitions.”

Financial Technology Partners served as exclusive financial and capital markets advisor to Payoneer. Davis Polk & Wardwell LLP served as legal counsel to Payoneer and Paul Hastings served as regulatory counsel to Payoneer. PwC served as Payoneer’s auditors. EY served as Payoneer’s tax and public markets advisor.

Citi and Goldman Sachs & Co. LLC served as financial and capital markets advisors to FTOC. Cantor Fitzgerald also served as capital markets advisor to FTOC, and Morgan, Lewis & Bockius LLP served as legal counsel to FTOC.

- 02:00 am

AREX Markets, the data-driven FinTech company that drives financing costs down for SMEs and enables them to get access to cash quicker, today announces its integration into the Xero App Store.

The AREX app helps to unlock money trapped in unpaid invoices and opens up alternative avenues for the UK’s SMEs to traditional invoice financing. The non-recourse finance-based business has been approved following a highly selective process, due to the unique and ethical approach it takes to invoice financing.

AREX facilitates a live, algorithm-based trade that enables businesses to access the cash held in their debtor book. The SME invoice itself becomes a tradable asset and AREX’s platform allows professional investors to invest across a range of these assets and industries.

Its integration provides seamless access to the service for Xero users, who needn’t leave their accounting software in order to unlock value from their invoices, and swiftly receive the money back to their balance sheets - often within 24 hours. AREX can be found in the Xero App Store under the Financial Services category.

Xero’s 720,000 UK subscribers will have access to AREX as it joins the marketplace.

Comments, “Xero’s goals and ours are perfectly aligned. We want to make it easier and fairer for SMEs to do business, and to take back control from traditional structures which have hindered their growth potential. To see the AREX app sit comfortably alongside other business finance options like Market Finance, Satago and iwoca Pay is a major milestone for the company and will accelerate its growth into the UK market where we can make a tangible difference to empower businesses to regain control of their cashflow. We’re really excited to see how this relationship with Xero develops.”

Commenting on the news, Ryan Pearcy, SB Digital director at Scrutton Bland added, “Cloud tech options are fundamentally changing the way business is done. AREX has gone a step further, because their aim is to take power away from the centralised operating model, in this case, the bank. Companies like AREX guarantee the customer competitive market rates and do it in the most ethical way possible. We choose to partner and work with market-defining apps. Through open market dynamics, AREX is one of these, with the ability to change the perception of how financing is used as a first resort rather than a last chance.”

The relationship with Xero accelerates AREX plans and growth within the UK market, following its recent successful EUR 8.8m Series A funding round.

- 06:00 am

Mastercard opens door to startups around the world looking to grow platforms across open banking, predictive financial modeling for small businesses, smart rental payments and beyond

Today the award-winning global startup engagement program Mastercard Start Path welcomes 11 fintech companies to receive dedicated support, access to customers and product teams, and opportunities to co-innovate. Finmod, Flourish Savings, GenEQTY, Karri, KeyChain Pay, Kwara, Layer, Osper, Swap, upSWOT and Wellthi have been selected to participate and are using gamification, behavioral science, social banking platforms and more to modernize payments. Of this group, GenEQTY, Finmod and Wellthi are joining the new Start Path track dedicated to supporting early-stage startups led by founders from backgrounds underrepresented in the fintech space as part of Mastercard’s In Solidarity commitments.

“We’ve seen tremendous growth across the fintech landscape, and more people are benefitting from the digital economy than ever before, whether they’re gaining access to credit for their small business through open banking or securely making payments to their child’s school from the comfort of their smartphone,” said Amy Neale, senior vice president, Fintech & Enablers. “Through Start Path, Mastercard creates a springboard for fintech companies that are driving a more inclusive digital economy and helps them accelerate the way they change the world.”

Mastercard has a track record of collaborating with startups. Since founding Start Path in 2014, the company has uncovered co-innovation opportunities and provided mentorship to more than 260 startups that have gone on to collectively raise more than $5 billion in capital. The following startups are joining this growing network to rapidly scale their business:

- Finmod helps small and medium-sized businesses forecast financials 10 times faster and make financial decisions in real-time.

- Flourish FI is an engagement and financial wellness platform for financial institutions, using gamification and behavioral science to empower individuals to establish positive money habits and achieve financial security.

- GenEQTY offers a smarter digital banking solution to help small businesses and solopreneurs improve financial performance, manage business health and get faster access to funding through one central data-driven business hub.

- Karri is a mobile payment app that facilitates fast and easy payments to schools and community organizations, and provides parents a convenient way to manage their child's money.

- KeyChain Pay is a smart platform for landlords and tenants to collect and pay rent using AI and credit card tokenization.

- Kwara is transforming credit unions into modern, digital banks with a credit union operating system and neobank experience for their members.

- Layer's digital banking platform delivers a blend of traditional and neo-bank capabilities from one platform, dramatically reducing cost, revolutionizing the customer journey and enabling banks and non-financial institutions to become truly digital.

- Osper empowers young people to earn, spend and save; its new B2B platform, Prosper, allows any company to launch their own youth card scheme in weeks at a fraction of the cost of building in-house.

- Swap is a Brazil-based platform that empowers businesses to embed financial services to expand their footprint, deliver unmatched product experiences and boost their economics.

- upSWOT offers a white-labeled business health dashboard that powers online and mobile banking platforms with 150+ API-enabled apps.

- Wellthi builds social banking solutions to help clients leverage the power of AI, data and online communities to attract and retain new customer segments by turning every card into a community.

As the fintech landscape continues to evolve and diversify, Mastercard embraces opportunities to support and collaborate with digital players to unlock potential and build the next generation of commerce.

Ready to scale your business with Mastercard as your global partner? Apply to Start Path here.

To learn about trends in the fintech industry, check out the latest report by Start Path and KoreFusion here.

- 05:00 am

Commenting on UK GDP showing a positive uptick and an encouraging economic outlook, Douglas Grant, Director of Conister, part of AIM listed Manx Financial Group, said: "Today’s UK GDP data shows a positive uptick quarter on quarter and provides a more encouraging outlook for the UK economy going forward. However, the plight of UK small businesses and current default levels caused by the ongoing impact of the pandemic should be of real concern. We must acknowledge that the UK’s business debt burden has ballooned to unprecedented levels and unfortunately this has already created a relentless flow of weak zombie-like companies falling off a loan default cliff. It is imperative that we support sectors and businesses that are strong and nimble enough to adapt to the new economy and therefore continue contributing to its growth.

"We also believe that the introduction of the Recovery Loan Scheme will act as second support system for those businesses currently struggling but with long term growth potential . Indeed, we have been pleased to see the Government look beyond the obviously more resilient business sectors and introduce the RLS which can support those businesses that have been mostly negatively impacted by Covid-19, such as the hospitality and leisure sectors. Conister will continue to do all it can, working alongside the Government and traditional lenders, to support businesses.

"At Conister we have delivered upon all of our initial objectives. We have lent our full CBILS and BBLS allocation and have applications which we hope can be accredited under the RLS. We will focus on lending this to robust businesses in all sectors that we believe will thrive in the future. Conister will continue to do all it can, working alongside the Government and traditional lenders, to support British businesses."

- 01:00 am

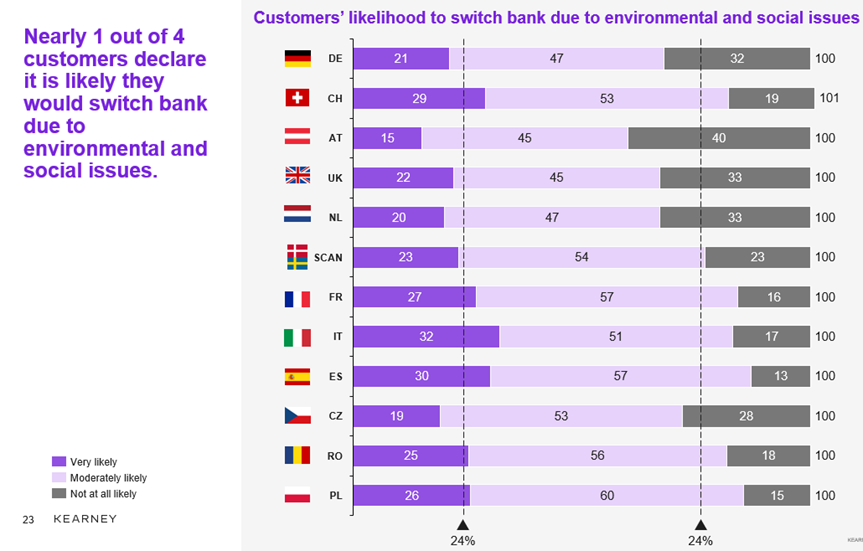

- 44% of European customers rate environmental and social issues as ‘very important’ when choosing a bank

- 18-24-year-olds are almost twice as likely to switch banks compared to those aged 55 and over

Analysis from global consultancy partnership Kearney has found that for almost half of consumers, environmental and social issues are a very important factor when choosing their banking provider. One in four European consumers (24%) are likely to switch if their bank is not engaged in ESG issues.

Responsible investing in particular was the most important ESG topic. 41% of respondents surveyed wanted the reassurance that the funds they invested in would not support companies that produced weapons or polluted the environment, or factories that disrespected safety standards and human rights.

In the UK, over one in five customers (22%) would likely switch to a bank with higher ESG priorities, whilst almost 30% of consumers in Poland, Romania, Spain and Italy reported the same sentiment. Beyond responsible investments, consumers were mostly concerned with climate change (34%), consumer and human rights (34%), and business transparency and accountability (31%), across all countries surveyed.

In terms of age demographic, 18-24-year-olds are almost twice as likely to switch banks compared to those aged 55 and over, with 30% reporting that they would switch for these reasons compared to 18% of the older group. Examining the data from the opposite perspective, only 17% of the younger demographic reported that they were not at all likely to switch over ESG concerns, compared to 31% of those 55 and above.

Simon Kent, Partner and Global Head of Financial Services at Kearney, comments:

“Banking is still a sector with low number of switchers compared to telecoms or utilities, but that doesn’t mean that banks should become complacent. Consumers are actively looking to engage with companies and brands that align to their values, so it’s important that banks take action.

Our research unsurprisingly shows that consumers are likely to be more loyal if they are aware of their bank’s ethical activities, but currently only an average of 40% know what their bank is doing in these areas. There is a considerable opportunity for improvement in customer communications and engagement on this topic to demonstrate a bank’s commitment and aspirations towards supporting and undertaking ESG initiatives more clearly.

ESG concerns are not only here to stay but will increasingly drive customer behaviour in the future, and retail banks must be at the forefront.”

Anand Kumar Bajaj

CEO at PayNearby

Mandar Agashe, Founder, Vice-Chairman and MD, Sarvatra Technologies said: see more

- 02:00 am

August 12 is International Youth Day, a date designated by the United Nations General Assembly in 1999 to recall the role played by young people in development and peacebuilding. Sber timed its research on the investment habits of young people to coincide with this date.

Understanding the stock market is a fundamental aspect of financial literacy. In fact, a great many young people aged 18–35 would like to learn the basics of investing: 50% of all brokerage accounts opened with Sber over the past year (between June 30, 2020, and June 30, 2021) belong to people in this age group. In absolute numbers, that is 1.5 million people. Residents of Moscow opened 34% of those accounts, with St. Petersburg (3% of accounts) following well behind the capital. Heightened interest in the stock market on the part of young people was also recorded in Samara, Yekaterinburg, Novosibirsk, Perm, Voronezh, Ufa, Chelyabinsk, and Volgograd. Forty-eight percent of accounts were opened by women and 52% were opened by men. In terms of general trends, 32% of brokerage accounts with Sber were opened by people aged 30–35, 29% by people aged 21–24, 21% by people aged 25–29, and 18% by people aged 18–20. Young women have a higher average portfolio size than young men: RUB 150,000 compared to RUB 130,000. Young investors tend to invest in shares and bonds. Gazprom, Sberbank, and Nornickel securities are the most popular Russian-issued shares among men, with Tesla, Apple, and Alibaba being the most popular foreign-issued shares. Women prefer to invest in Sberbank, Gazprom, Nornickel, Tesla, Alibaba, and Boeing. Transactions usually take place several times a year (50% of men and 53% of women). Twenty-six percent of young men and 27% of young women trade several times per quarter, 15% and 14% trade several times in six months, and 9% and 6% trade several times per month, respectively. Both young men and women prefer to trade based on investment analytics, which is why 83% selected the Investment plan, which provides them with access to exclusive analytical reviews. There are a lot of young people in the stock market now: 47% of all active brokerage accounts with Sber were opened by clients aged 18–35. That means that 2.3 million accounts belong to young investors. Forty-two percent of them have both a brokerage account and a personal investment account. Although so far Sber counts more men in this age group among its clients (59% of accounts opened), young women are quickly catching up. We strive to make our investment products as convenient as possible for young people and to help them achieve the financial results they desire.

In terms of general trends, 32% of brokerage accounts with Sber were opened by people aged 30–35, 29% by people aged 21–24, 21% by people aged 25–29, and 18% by people aged 18–20. Young women have a higher average portfolio size than young men: RUB 150,000 compared to RUB 130,000.

Young investors tend to invest in shares and bonds. Gazprom, Sberbank, and Nornickel securities are the most popular Russian-issued shares among men, with Tesla, Apple, and Alibaba being the most popular foreign-issued shares. Women prefer to invest in Sberbank, Gazprom, Nornickel, Tesla, Alibaba, and Boeing.

Transactions usually take place several times a year (50% of men and 53% of women). Twenty-six percent of young men and 27% of young women trade several times per quarter, 15% and 14% trade several times in six months, and 9% and 6% trade several times per month, respectively. Both young men and women prefer to trade based on investment analytics, which is why 83% selected the Investment plan, which provides them with access to exclusive analytical reviews.

There are a lot of young people in the stock market now: 47% of all active brokerage accounts with Sber were opened by clients aged 18–35. That means that 2.3 million accounts belong to young investors. Forty-two percent of them have both a brokerage account and a personal investment account. Although so far Sber counts more men in this age group among its clients (59% of accounts opened), young women are quickly catching up. We strive to make our investment products as convenient as possible for young people and to help them achieve the financial results they desire.

- 01:00 am

Fraud, AML, compliance, customer treatment, systems and controls top the list of 2,754 separate allegations logged by 1,046 whistleblowers in the last year

The Financial Conduct Authority (FCA) has received a total of 2,754 separate allegations of misconduct, including fraud, money laundering and compliance complaints, according to official figures. The data, analysed by a Parliament Street think tank and contained in the FCA’s newly published Annual Report and Accounts 2020/21, details the allegations, which were provided by a total of 1,046 whistleblowers in the last 12 months.

The report also revealed that there are 184 individuals and firms under investigation for carrying out unauthorised business, and £189.8 million in financial penalties had been handed out over the same period, alongside a number of prosecutions alleging insider dealing, investment fraud or money laundering.

The FCA revealed it has strengthened its AML supervisions over the last year, becoming more data-led and drawing from a range of information sources. As a result, at the end of March 2021, the body said that it had increased the number of firms required to submit financial crime-related data.

The 1,046 ‘whistleblowing’ reports – staffers reporting against their own organisation – is a small reduction when compared to the 1,100 reports in 2019/20, and, this year, 15 led to ‘significant action’ to mitigate harm, which may have included enforcement action.

In a further 135 cases they took ‘action’ to mitigate harm, which included writing to or visiting a firm, requesting further information, or asking a firm to attest to compliance with the rules. 145 cases were said to have helped inform the FCAs work, and were relevant to the prevention of harm, but did not lead to any specific action; 97 cases were not considered relevant, and 654 cases were still being assessed at the time the report was published.

The retail banking sector was also subject to scrutiny by the FCA in the recorded period and, in February 2021, a ‘Dear CEO’ letter, detailing the risks of harm that retail banks’ activities were causing, was issued. The regulator handled 97 cases involving AML in the retail banking sector, put in place one Voluntary Requirement Notice (VREQ), progressed

5 s166/skilled person assessments and progressed 15 enforcement cases related to

AML failings, one of which was a new case for the period.

FY 20/21 also marked the first full financial year when the FCA was responsible for accessing the Anti-Money Laundering (AML) measures of cryptoasset businesses, which pose ‘increase risk of financial crime’. The report revealed that 138 firms that appeared to be trading without having applied for registration had been placed on a public-facing register.

Wayne Johnson, CEO, Encompass Corporation, comments:

“This year, more individuals are attempting to use the chaos of the pandemic to carry out financial crime. Therefore, it is important that the FCA is taking the necessary to steps to tighten their control and increase visibility over new sectors and payments technologies, such as cryptocurrencies, which are being used to launder money.

“But, the fight against financial crime can’t be won by the regulators alone, and businesses from all sectors must improve the efficiency and effectiveness of their onboarding processes, compliance and due diligence, not just for the sake of ‘ticking boxes’ and averting regulatory fines, but to help prevent even more financial crime and dirty money running through critical businesses and infrastructure.

“In today’s digital climate, organisations are encouraged to invest in automated regulatory technology, which can boost the effectiveness and efficiency of compliance programmes whilst keeping costs low.”

- 03:00 am

Validis, the provider of open accounting data and analytics, announces the appointment of Matt DeVoe as VP of Sales to spearhead its North American financial services growth.

Matt joins Validis from LendingFront and has previously held roles at EDR/LightBox where he helped drive strong expansion of SMB finance technology across the US. Matt’s appointment signals an increased focus by the global fintech to further expand its regional footprint and embed the Validis platform across the North American financial services sector.

Validis currently manages the acquisition and curation of SMB accounting data for several top-tier banks, lenders, and the largest global accounting firms – including the US and Canada, where it has had a long-standing operational presence.

“I’m delighted to join Validis in a key role that will help drive further success for the firm”, says Matt. “Validis are a well-established fintech with a wealth of experience, expertise, and an unrivalled level of sophistication in its technology. It’s a very exciting time in the financial services space where we are seeing a huge focus on digital transformation and a wide-spread appetite to improve connectivity and access data in a way that will better serve the SMB community. The Validis platform allows FI’s to seamlessly automate a very manual and time-consuming part of the underwriting and customer management process. I am looking forward to being part of a team that will help reshape the SMB lending experience and drive value for more banks and lenders across North America”.

Paul Thomas, CEO of Validis said, “We’re delighted to welcome Matt to our growing team as we continue to expand our coverage in an evolving US market. He has an impressive track record and brings a depth of knowledge and experience of the banking and SMB lending sector. With our continued focus on product innovation, increased data coverage, and the addition of high-calibre people like Matt, we have exceptional capability to serve our growing customer base.”

- 05:00 am

Credit card spend 3.5 percent higher compared to June 2019 suggests some households are benefitting from pandemic savings, but not everyone is experiencing post-COVID confidence with accounts missing two payments increasing 15 percent compared to May

Highlights

- Fourth consecutive monthly increase in credit card spend – 6 percent year on year – with spend now higher than June 2019 levels

- Further increase in percentage of payments to balance - 2.5 percent – although growth slowing

- 15 percent increase month-on-month in accounts missing two payments

- Cash usage continues to slowly grow, by 9 percent; but still 62 percent below pre-pandemic levels

Global analytics software provider FICO today released its analysis of UK card trends for June 2021. Maintaining the pattern for the year so far, average spend continued to increase compared to 2020. As the UK was only just coming out of lockdown in June 2020, this rise in spend is unsurprising, but the fact that average spending was 3.5 percent (£23) above 2019 levels suggests that, for those who have been able to save through the pandemic, there is confidence in their future financial stability.

However, the percentage of accounts missing payments reflected the fact that not everyone has been able to accrue savings during the last 18 months. With the end of lockdown across the UK and summer holidays prompting spending in the next months, and government support for furlough payments reducing from 1st July, lenders will need to be vigilant for those already facing financial pressure who could struggle further to stay on top of debts.

Spend on UK cards continued to increase, along with the percentage of payments

The average spend on UK credit cards increased year-on-year for the fourth consecutive month, by £40 to £691, a larger increase than seen in May. It also exceeds the June 2019 spend by £23 with the sunny weather and the Euro 2020 competition likely to have contributed to this uptick.

Average card balances marginally increased month on month. They are 4 percent lower than a year ago and 12 percent below June 2019 levels, suggesting that households are trying to manage their spend in the face of a still-uncertain future.

Mixed picture on payments

Whilst average spend increased year-on-year, the FICO data reveals mixed fortunes when it comes to payments.

The growth in the payments-to-balance ratio started to slow in June 2021, increasing by just 2.5 percent month on month. Year-on-year it is 45 percent higher, although that is unsurprising as some businesses were still arranging furlough and loan support in June 2020. However, it is 18 percent above June 2019 levels, suggesting the use of savings as well as continued government support.

The percentage of accounts paying the full balance stabilised in June and was 16 percent higher than June 2020. Despite the percentage of accounts paying the minimum payment increasing by 3 percent in June, the proportion is still 11 percent below that seen in June 2019.

Missed payment rates remain low

The percentage of accounts missing one payment increased in May. A proportion of these were unable to make a payment in June, which resulted in a 15 percent increase in the percentage of accounts missing two payments and 9 percent increase in their balance compared to total balance.

All average balances on accounts missing payments decreased month-on-month again in June. However, all balances are higher than a year ago, and 2, 3 and 4+ missed-payment accounts are higher than June 2019, prior to the pandemic with 3 and 4+ balances over 18 percent higher.

Cash usage continues to slowly grow but remains below pre-pandemic levels

Cash as a percentage of total spend fell month on month and is 8 percent lower than a year ago and 37 percent lower than June 2019, highlighting the change in attitudes towards cash.

Whilst the percentage of consumers using cash on their credit cards increased for the third consecutive month, it is 16 percent lower than June 2020 and 62 percent lower than June 2019.

Looking ahead

FICO July data will reflect the initial impact of the last stage of the re-opening of high-risk retail and entertainment sectors, as well as the start of the school holidays. It is expected that spend will continue to increase, although levels may not be as high as anticipated because of the ongoing confusion around foreign travel rules. Higher levels of savings may also continue to blur the picture of those negatively impacted by the winding down of the furlough scheme and further business closures.

Lenders will be keeping a watch on the impact all these factors have on their customers and any changes in payment trends as early indications of financial stress. Those that act quickly, offering the most appropriate options, will be viewed most positively by their customers and the regulators.