Side by side comparison of the best loan origination software on the market

- Vit Arnautov, Chief Product Officer at TurnKey Lender

- 01.07.2019 09:30 am Loan Origination Software , Financial IT

Loan origination is a critical part of any lending business. The whole subsequent process depends on origination: collecting the right data about customers, analyzing it carefully and quickly enough, selecting only the eligible borrowers, evaluating risks, etc. For many businesses, origination is what makes the loan issuing process lengthy and stressful both for loan officers and for their clients. Traditional banks who haven’t yet fully embraced FinTech advancements are the best examples here. And borrowers, who have a choice now, find an alternative. That’s why in 2019 the transaction value of alternative lending is already estimated to be US$241,543m.

Unlike traditional banks, smaller operations and all kinds of alternative lenders don’t have the resources to create a wholesome platform to automate all their lending work. Yet they desperately need quality automation to have a smaller staff and winning rates compared to the competition. That’s where they turn to FinTech companies which provide them with ready-made tools that will address their specific needs. But in the whole lending process, one of the hardest sectors to automate is origination. A lot depends on it and it requires really deep analytics of data. And tools work the best with a seamless user interface. User experience is a must to attract customers and also boost productivity within the organization. For a good UI, uibakery.io can help design UI components for your small business so that no one is stuck while carrying out the simple processes at work. It helps optimize the workflow as well.

The major elements of the origination process are:

Pre-qualification

Loan application

Application processing

Underwriting

Credit decisioning

Loan filling

Each of those elements can and should be digitalized and better yet automated. This way a lender doesn’t need the big staff or multiple branches to take care of all these steps. But not any origination automation software will do the trick. All the providers claim to reduce operational costs, improve time-to-funding, and have all the functionality you may need, but a business owner has got to stay cautious. Some platforms are good at automating only a part of the steps listed above, some lack security, and some only fit particular business models. The most important factors to consider when choosing loan origination software are:

Security

Regular updates

Full process automation

Integrations with relevant databases

Price

Option to have a test drive

You’d think origination software providers would be very vocal about the real capabilities of their platforms. But most of them aren’t and it takes time to even understand what exactly their product does. So we’re going to look at each company’s offering to see what each of them has to offer.

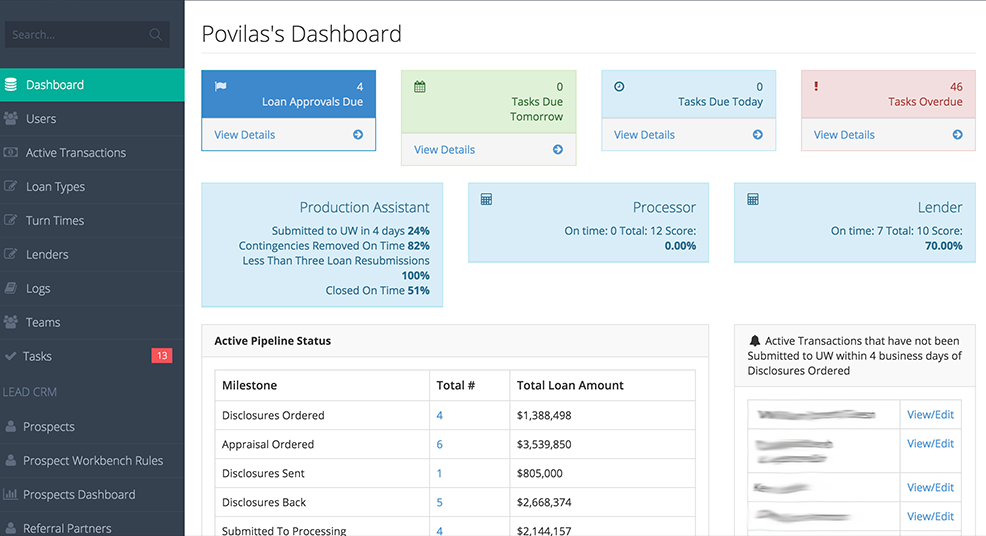

TurnKey Lender

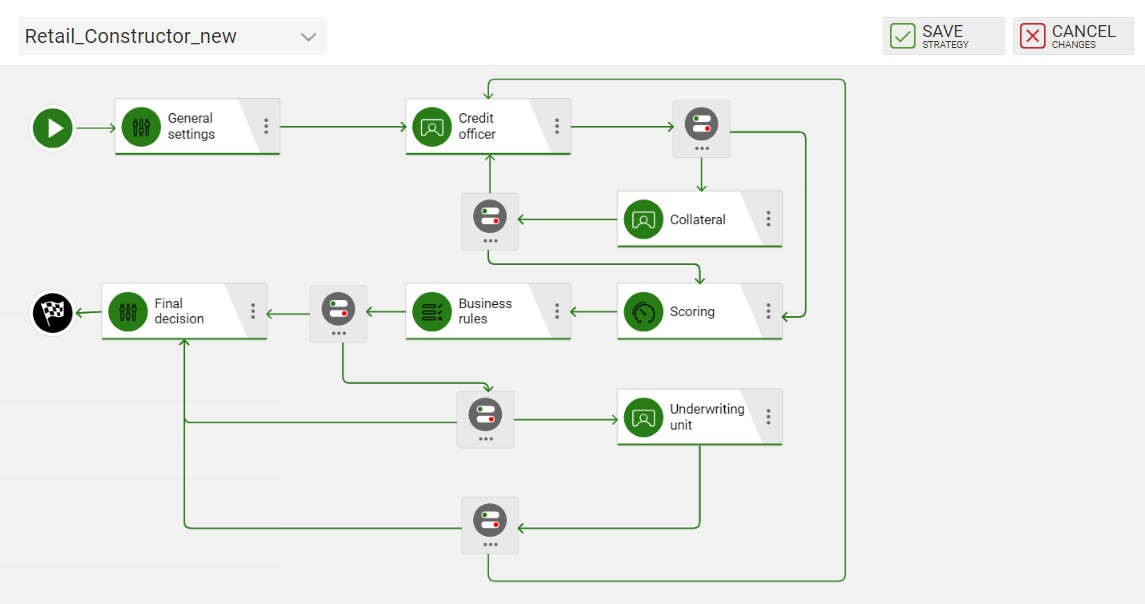

And we’ll start with TurnKey Lender. It’s an intelligent cloud-based software that automates the whole lending process, not just origination. Other functionality includes automation of collateral management, risk management, debt collection, loan servicing, reporting, supervision, and regulatory compliance. But we’re focusing on loan origination today. The loan origination software takes care of all the steps I listed at the beginning of the post. The system includes integrations with all the major credit bureaus and synchronizes with external databases to make informed decisions about the borrowers.

One of the most important and unique selling points of this company’s origination solution is its meaningful use of AI and machine learning. Advanced algorithms learn about each business’ clients and evolve to make more of the right credit decisions with reduced risks. Pre-programmed logic responds differently to different loan applications and evolves intelligently over time. You can customize the base system with alternative scoring models that are easy to install with APIs.

The platform easily deploys from the cloud and can be customized by the client. Lenders can opt for a free trial and start using it for free, paying as they start to make money.

This platform is tailored for the alternative, SME, peer-to-peer and direct lenders, auto financing, mortgage, community banks, and credit unions. If there’s a need for deep customization, the platform can be revamped to meet the client’s needs. Customization is really intuitive and can be done by the representatives of the customer or under TurnKey Lender’s supervision.

Cloud Lending Solutions

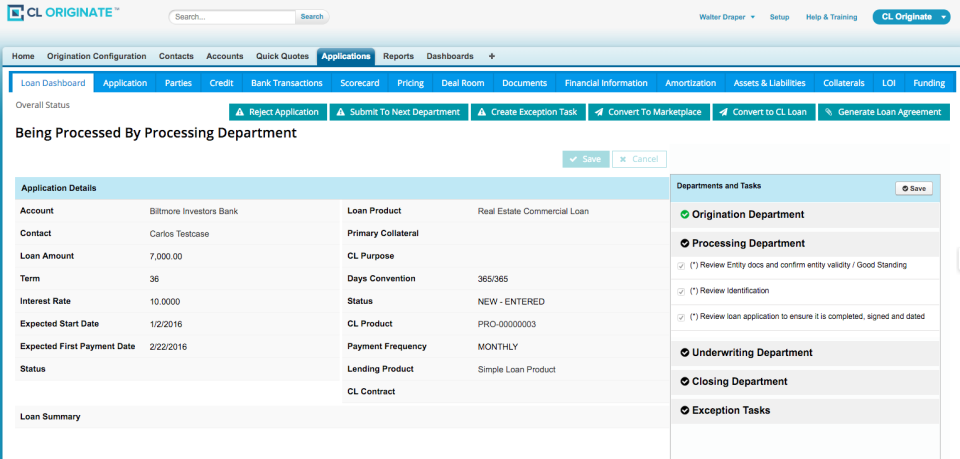

CLS is another platform solution that aims at helping lenders reduce operational inefficiencies through automation and configuration. The products of the company exist in the form of Salesforce apps and include a set of plugins/applications that can be used in a group and separately. The solution for origination is called CL Originate. The solution has functionality that helps lenders manage origination processes including loan file management, underwriting, decisioning, credit analysis, and approvals.

The emphasized pros of the system are the fact that it’s cloud-based and has some configurability. At the same time, it’s worth noting that the system collects data, but you will need to do risk evaluation yourself. On the other hand, some of the loan decisioning is automated and the system can be integrated with third-party data sources.

Even though Cloud Lending Solutions claims to provide an end-to-end solution, their products come as separate packages for portals, loans, leases, origination, marketplaces, and collections. The primary industries served are commercial, consumer and small business lending, and equipment finance.

Some of the big disadvantages of the platform are that there’s no free trial to test it out, the platform isn’t truly all-in-one, and different solutions don’t grant as much flexibility.

CloudBnq

CloudBnq is a web-based solution providing some loan origination features for community banks and credit unions. The solution’s functionality allows for lending campaign creation and management, loan application collection, review, decisioning and application completion. On the other hand, the system leaves complex things like risk evaluation and underwriting to you or to some additional solution you’d need to purchase and sync up with CloudBnq.

LendingPad

LendingPad isn’t positioned as an end-to-end solution. It only works as a point-of-sale and loan origination system. The product is mainly aimed at lending professionals in general, be it banks or credit unions. The functionality covers things like lead and campaign management, service level agreements, document storage, real-time reporting, workflows customization, and loan tracking.

The risk management and automation of the processes leave much to be desired. LendingPad can work as an addition to existing functionality to reduce friction on the point-of-contact level, but one would still need a custom risk evaluation solution. And there is a chance this would leave a lot of room for unnecessary human labor which could be automated. The benefit of this system is that it can work for warehousing activities, post-closing tracking, and tracking of loan characteristics.

Encompass

EllieMae’s Encompass platform for loan origination is one of the big market players. It’s a tool suite that allows lenders to use only the modules they need in their operations. The solution includes functionality for compliance, integrating with external software providers, custom screens tailored to individual personas. The end goal for the company is to provide lenders with a flexible tool that fits different business processes and operations.

Calyx Point

The product in the Calyx’ product lineup responsible for loan origination is called Point. The system is supposed to target a wide specter of lenders, from banks to credit bureaus. When it comes to origination, the key functionality is the loan processing which gives you a score for each client, loan submission control, online application, and an audit trail.

However, the system doesn’t have the proper compliance and fee management in place and isn’t cloud-based. According to the users, the system has got a rather steep learning curve and isn’t always stable when it comes to processing and storing data.

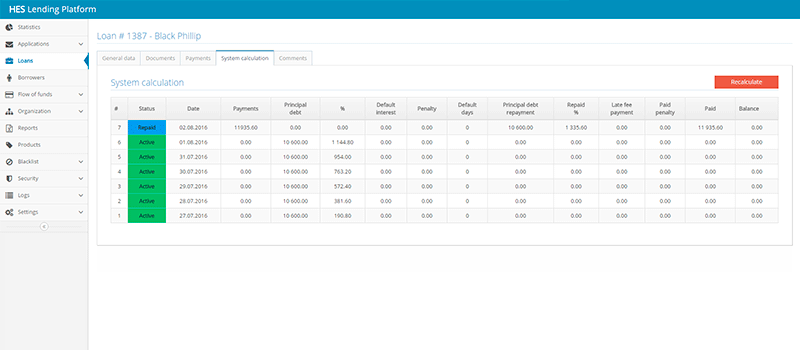

HES Lending Software

The HiEnd Systems’ product is comprised of multiple modules that cover different stages of the lending process for consumer and business lending. The solution isn’t boxed, so the company is open to implementing changes into the system to meet the specific needs of the client and offers a free trial.

Like TurnKey Lender, HiEnd Systems utilizes AI for credit scoring, but in their case, the algorithms need at least initial 1,000 issued loans to get rolling.

LoanDisk

LoanDisk is a system developed specifically to address the needs of the microfinance industry. And even though it has some origination functionality embedded within its core, it’s not adjusted for managing the underwriting process, doesn’t have Credit Bureau integration, manual scorecards, internal scoring, and decision rules. That said, users can add custom fields to Loan Application from the interface, and have a lot of report options by default, not to mention the built-in accounting features. All things considered, LoanDisk is better suited for managing an already issued loan.

Final thoughts

Solutions for loan origination differ and it’s critically important for your business that you choose the right one. Keep in mind that while origination functionality is very important, what comes after also needs to be automated and preferably by the same provider to ensure compatibility. So the software you choose should either cover the next steps as well or be easily integrated.

It’s clear that even though on the paper there are many loan origination solutions when it comes to real functionality, stability, and scalability, very few actually stand out. What’s your favorite origination and lending automation software and why? Let me know in the comment section below.